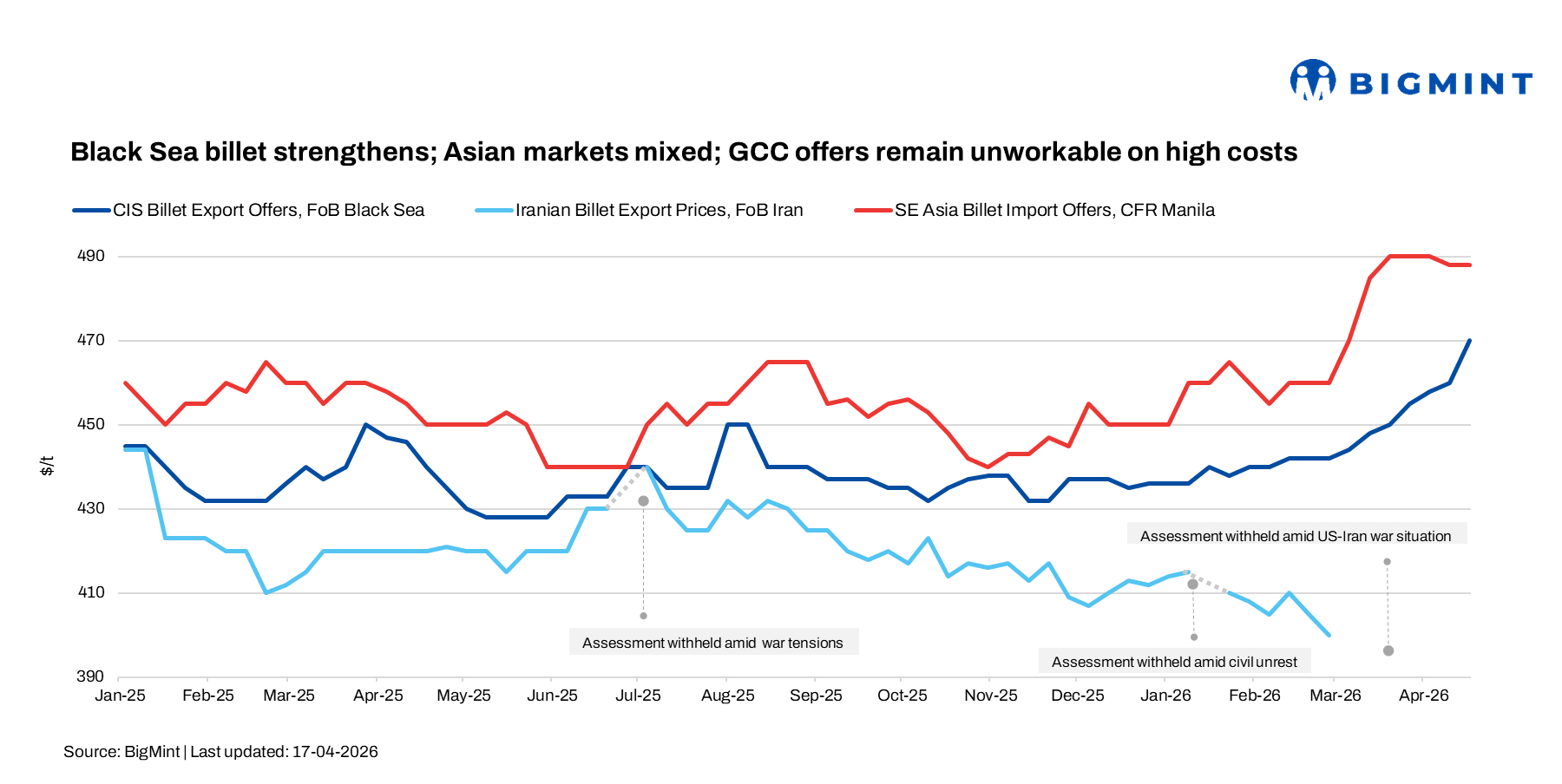

Weekly round-up: Black Sea billet strengthens on currency gains, Chinese offers remain stable

...

- Iran remains absent from export market

- GCC offers unworkable on high freight

Global billet markets showed mixed trends this week, with CIS/Black Sea prices strengthening on a firmer rouble and firm seller control, while China lent support through stronger domestic billet and rebar futures, keeping export offers largely stable w-o-w. Southeast Asia remained cautious, with slight softening in Manila and weak demand in Taiwan, while reliance on Chinese supply increased amid limited Iranian availability.

In the Middle East, Iran's disruptions tightened flat steel supply and constrained exports, while GCC billet offers remained elevated but largely unworkable due to high conversion and logistics costs. Overall, competitive billet flows and logistical uncertainty continued to shape trade dynamics and cap aggressive buying.

In Turkiye, deep-sea scrap prices remained stable at $395-405/t CFR, supported by tight US/EU supply, a stronger euro, and firm freight rates. However, mills remained cautious, with April requirements largely covered, resulting in limited deal activity and a wait-and-watch approach.

CIS/Black Sea Market

CIS export billet prices strengthened to $475-480/t FOB Black Sea, up from $460-470/t last week, supported by a nearly 3% appreciation in the Russian rouble and firmer competing offers. Some suppliers pushed offers to $490-500/t FOB, though these were widely viewed as unworkable. Sellers remained firm, anticipating delayed deal closures.

In Turkiye, import billet prices were assessed at $495-500/t CFR, with expectations of up to $505/t CFR in near-term bookings. However, buyers remained resistant above the current levels, keeping negotiations slow. Domestic billet offers from Kardemir were steady at $540/t exw and $550/t exw for different grades, while other mills quoted $550-560/t exw, though higher levels saw weak traction amid subdued rebar demand.

Alternative origins remained available but less competitive. Chinese billet for June shipment was heard at $500-520/t CFR, facing limited interest due to longer lead times, while Malaysian billet at $530-540/t CFR also saw muted demand. Overall, sentiment improved, but actual trade volumes remained limited.

According to market participants, Russia-origin billet has re-emerged in Taiwan, with a deal concluded at $485-490/t CFR for a 45,0000-50,000 t cargo.

A Southeast Asia-based trader said lower-priced Russian billets could start influencing import dynamics and may put pressure on scrap prices, although the extent of the impact remains uncertain at this stage.

Asian billet market

Asian billet markets showed mixed movement this week, with Chinese export offers (3SP 150 mm) steady at $463-465/t FOB, indicating a seller-driven market. Domestic sentiment remained supportive, with Tangshan Q235 billet at RMB 2,990/t and SHFE rebar futures at RMB 3,103/t, reflecting improved demand visibility and tighter supply.

Another Southeast Asian billet supplier added that Chinese FOB offers remain stable at $460-465/t, with transactions typically closing in the $480-490/t CFR range depending on grade, size, and cargo volume.

In Southeast Asia, Manila prices softened slightly, with China-origin 5SP billet at $485-490/t CFR, while Indonesian offers held at $490-495/t FOB. Taiwan market activity remained weak, with Chinese billet offers at $480-485/t CFR and no bids reported, reflecting cautious buying and sufficient short-term coverage.

A Singapore-based trader said Chinese-origin 3SP billet traded around $480/t CFR Thailand for 25,000-30,000 t cargoes, while 5SP offers to Manila were heard at $485-488/t CFR, with limited fresh deals concluded.

Despite some softness, regional sentiment remained supported by firm Chinese domestic trends and limited rebar availability, as mills increasingly prioritised billet exports over finished steel.

Middle East/Iran market

Iran's steel sector remains disrupted after previous airstrikes on key facilities, including Khouzestan Steel Company (KSC) and Mobarakeh Steel Company (MSC). These producers are expected to take 6-12 months or longer to resume operations, tightening flat steel supply and impacting sectors like automotive and appliances. As a result, import demand is expected to rise to around $4 billion, mainly from Russia and China.

Billet supply, however, remains relatively stable due to Iran's large production base (around 20 mnt annually). Still, exports are limited by logistics disruptions, energy shortages, and regional instability, with most trade focused on essential shipments. Iranian billet is largely absent from export markets such as Jordan, while Saudi-origin billet at $530-550/t exw remains unworkable due to high conversion and freight costs.

The UAE rebar market remains active, driven mainly by contractor-led stockpiling amid supply and logistics concerns, rather than real demand. While April demand is seen around 0.35-0.4 mnt, actual consumption is lower at 0.3-0.32 mnt as some volumes shift to May.

Prices remain firm, with retail rebar at AED 2,800-2,900/t ($762-790/t) and mill offers at AED 2,650-2,700/t ($721-735/t), with imports at similar levels. However, improving scrap inflows and weaker demand could pressure margins and lead to price corrections.

Outlook

Outlook

Billet markets are expected to remain supported on currency strength, elevated input costs, and constrained supply, particularly in the Black Sea region. However, weak downstream demand and cautious buyer participation are likely to cap any meaningful upside. At the same time, ongoing disruptions in Iran and evolving trade flows across Asia and the Middle East will continue to reshape regional flow.