China weekly: Steel prices show mixed trends w-o-w as raw material costs fluctuate

...

- Gradually improving demand supporting prices

- Crude steel production reaches 247.55 mnt in Jan-Mar'26

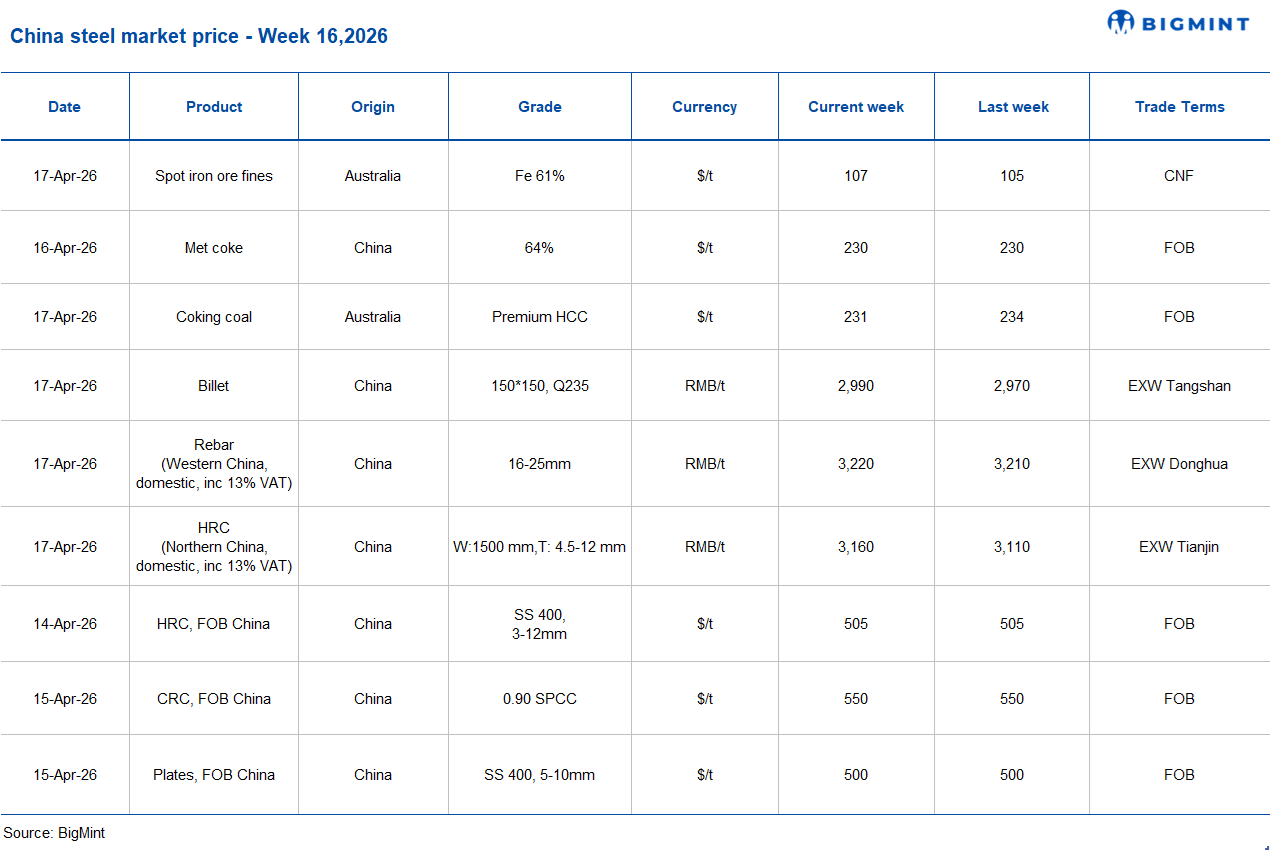

China's steel prices remained mixed in the week ended 17 April 2026, with domestic hot-rolled coil (HRC) prices increasing w-o-w, while rebar prices remain rangebound. Raw materials, including iron ore, billet prices rise, while met coke and coking coal prices remain range bound w-o-w.

China's crude steel production reached 247.55 million tonnes (mnt) in January-March 2026, marking a 4.6% decline y-o-y, according to data from the National Bureau of Statistics (NBS). Moreover, crude steel output in March 2026 stood at 87.04 mnt, down by 6.3% y-o-y.

China's steel exports stood at around 24.717 mnt during January-March, down by 9.9% y-o-y, according to data from the General Administration of Customs.

Additionally, exports in March reached 9.135 mnt, up by 16.5% from around 7.84 mnt in February. However, the same was 12.6% lower y-o-y compared with the same period last year.

Steel inventories at key China Iron and Steel Association (CISA) industries stood at around 17.51 mnt in early-April marking an increase of 960000 tonnes (t) or 5.9% compared with 16.55 mnt in late-March. Inventory level dropped by 300,000 t or 1.7% m-o-m compared with from early-March. Furthermore, the same rose by 1.47 mnt or 9.2% y-o-y against 16.04 mnt a year ago.

1.Iron ore spot prices rise w-o-w: Iron ore fines benchmark prices for Fe 61% inclined by $2/t w-o-w to $107/dmt CFR China on 17 Apr'26. Prices rose on improved liquidity from fresh increased supply post easing restrictions and stronger-than-expected China macro data, though gains were capped by weak trading activity. Meanwhile, expectations of stronger steel exports amid Middle East peace talks, along with potential sintering curbs, favouring high-grade ore demand, lent additional support to prices.

a) Spot pellet premium edges down w-o-w: Spot pellet premium for Fe 65% grade pellet declined by $0.15/t to $17.35/t CFR China on 15 April.

b) Spot lump premium largely stable w-o-w: Spot lump premium held firm w-o-w at $0.1680/dmtu on 17 April.

2.Billet edges up as demand picks up: China's billet market saw a mild upward move this week, with prices rising by RMB 20/t ($3/t) w-o-w to RMB 2,990/t ($439/t). The week started on a relatively steady note, with balanced demand-supply keeping prices range-bound.

However, momentum gradually built from mid-week onwards as rebar consumption improved, supported by healthy March-April sales and faster inventory drawdowns across markets.

On the export front, sentiment turned firmer. Mills showed more confidence by pushing up base offers and reducing room for negotiations. Billet export prices also inched up to around $465/t FOB, reflecting this improved outlook.

Cost support remained intact, with steady iron ore prices and expectations of further coke price hikes lending strength, although high port inventories continued to cap any sharp upside.

The uptick was largely driven by better demand visibility and stronger trading activity. That said, intra-week volatility persisted, highlighting that while sentiment has improved, buyers are still cautious and not chasing the market aggressively.

3. China's coking coal market stable: China's domestic coking coal market remained largely stable during the week, with normal mine supply and slight spot price corrections due to cautious procurement and limited downstream orders. Despite this, strong steel production and high blast furnace utilisation supported healthy margins and kept coking plant inventories low. Additionally, Chinese coke producers have proposed a second round of price increases, though steel mills have yet to respond, keeping the market in a negotiation phase.

In the seaborne market, Australian premium hard coking coal (PHCC) prices fell $3/t to $231/t FOB on 17 April, while BigMint's PHCC index declined $2/t w-o-w to $253/t CNF Paradip, pressured by weak buying interest and almost stable Australia-India freight rates.

4. Domestic HRC prices surge w-o-w: The Chinese HRC prices stood at around RMB 3160/t ($463/t) on 17 April increasing by RMB 50/t ($7/t) w-o-w from RMB 3110/t ($456/t) a week ago. Furthermore, SHFE HRC futures (October 2026 contract), also increased by RMB 52/t ($8/t) to RMB 3,323/t ($487/t) from RMB 3,271/t ($479/t) a week earlier. Meanwhile, China's HRC export offers remained stable at around $505/t FOB a week earlier.

HRC demand has been slowly picking up, helping reduce excess stock levels across markets. As more material moves into end-use sectors, inventories are easing, which is offering some support to prices. However, with supply still available and buyers remaining cautious, any price improvement is likely to stay gradual in the near term.

5. Rebar prices up w-o-w: The rebar prices in China rose by RMB 10/t ($1/t) stood to RMB 3,220/t ($472/t) as on 17 April from RMB 3,210/t ($471/t) in the previous week. Furthermore, SHFE Rebar futures (October 2026 contract), also increased by RMB 39/t ($6/t) to RMB 3,133/t ($459/t) from RMB 3,094/t ($453/t) a week earlier.

China's Shagang Steel has continued to keep its long steel prices unchanged for mid-Apr'26 sales, with no price revisions announced since 11 Sep'25. Prices of rebars, coiled rebars, and wire rods are as follows:

Rebars (16-25 mm): RMB 3,450/t ($506/t)

Coiled rebars (8-10 mm): RMB 3,560/t ($522/t)

Wire rods (6-10 mm): RMB 3,470/t ($509/t)

Outlook

China's steel market is showing early signs of improvement, with demand gradually strengthening and inventories beginning to ease. While this offers some relief to market participants, cautious buying and ample supply may keep price gains gradual and prevent any sharp upward movement in the near term.