LME lead slips w-o-w as profit booking emerges; falling inventories cushion downside

...

- Prices retreat from weekly highs on cautious participation

- SHFE prices remain firm amid stable domestic demand

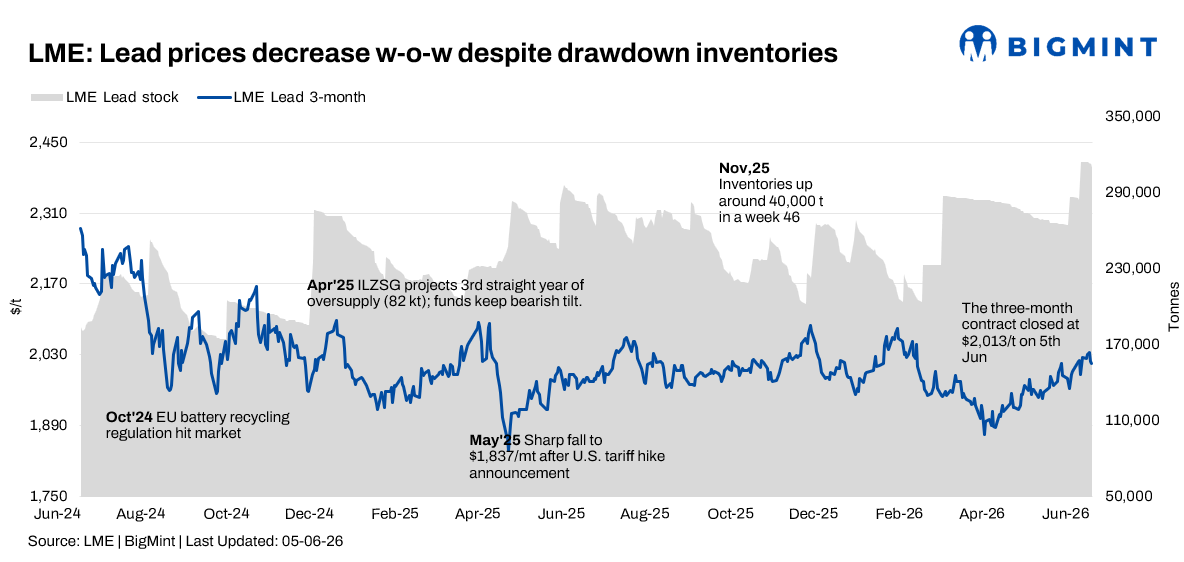

Lead prices on the London Metal Exchange (LME) edged lower during the week ended 5 June 2026, as profit booking emerged after the previous week's rally above the psychological $2,000/t mark. While broader base metals sentiment remained relatively supportive, gains were capped by cautious downstream demand and a lack of strong bullish triggers.

However, declining LME inventories provided some support to prices and helped limit downside pressure, indicating steady warehouse outflows despite mixed demand conditions.

Price trends

The LME three-month lead contract opened the week at $2,023/t on 1 June and strengthened initially, reaching a weekly high of $2,035/t on 3 June.

However, prices failed to sustain higher levels and gradually eased during the latter half of the week amid profit booking and cautious market participation. The contract settled at $2,013/t on 5 June.

LME cash lead prices followed a similar pattern. Cash settlement prices rose from $2,008/t on 1 June to a weekly high of $2,035/t on 3 June before retreating to $2,003/t by the end of the week.

On a w-o-w basis, the three-month contract declined by $11.5/t from $2,024.5/t recorded on 29 May, while cash prices fell by $13/t from $2,016/t over the same period.

Despite the correction, lead prices continued to hold above the key $2,000/t level, suggesting underlying support remains intact. Immediate resistance is seen near $2,035-2,050/t, while support is emerging around $1,990-2,000/t.

Inventory analysis

LME lead inventories declined steadily throughout the week, offering support to the market despite softer price action.

Stocks remained unchanged at 313,950 t on 1 and 2 June before falling to 313,675 t on 3 June, 312,525 t on 4 June, and further to 310,350 t on 5 June.

Overall, exchange inventories declined by 3,600 t during the week, reversing part of the sharp stock build witnessed in the previous reporting period.

The inventory drawdown suggests improving warehouse outflows and relatively balanced supply conditions, although overall stock levels remain elevated compared with recent months.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices remained broadly stable and showed a modest upward bias towards the end of the week.

SHFE lead prices eased from $2,374/t on 1 June to $2,369/t on 2 June before recovering gradually to $2,384/t on 5 June.

The resilience in Chinese lead prices indicates relatively stable domestic demand conditions and helped provide support to broader market sentiment.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures traded within a narrow range and ended marginally lower during the week.

The June 2026 lead contract opened at INR 207.35/kg on 1 June and touched a weekly high of INR 208/kg on both 2 and 5 June. The contract recorded a weekly low of INR 205.05/kg on 2 June before settling at INR 206.65/kg on 5 June.

Market participation improved during the week, with open interest rising from 360 lots on 1 June to 404 lots on 5 June. The increase in open interest alongside relatively stable prices suggests fresh positions were being added as participants assessed the market's ability to sustain levels above INR 206/kg.

Trading volumes remained moderate, reflecting cautious sentiment amid mixed global cues.

Outlook

Lead prices are expected to remain largely firm in the near term, with support from declining LME inventories and relatively stable Chinese market conditions. However, the inability to sustain gains above $2,035/t indicates that bullish momentum remains limited amid cautious downstream demand and ongoing profit booking activity.

Market participants will continue to monitor inventory trends, developments in the battery sector, and broader macroeconomic indicators for clearer directional signals. Immediate resistance is seen around $2,035-2,050/t, while support is expected near $1,990-2,000/t. The overall market tone remains neutral to mildly positive as tightening inventories partially offset demand-side concerns.