Weekly round-up: Steel prices correct amid demand pressure

...

- NMDC raises iron ore prices, but pellet, sponge iron prices weaken

- Rebar, HRC soften amid weak demand; ferro alloys show mixed trends

Indian steel prices continued to weaken in the week ended 6 June 2026, with billets, sponge iron, rebar, and HRC registering declines amid subdued demand and cautious buying activity. While NMDC raised iron ore prices for June, softer pellet prices and weak downstream consumption kept sentiment across the steel value chain under pressure.

Iron ore and pellet

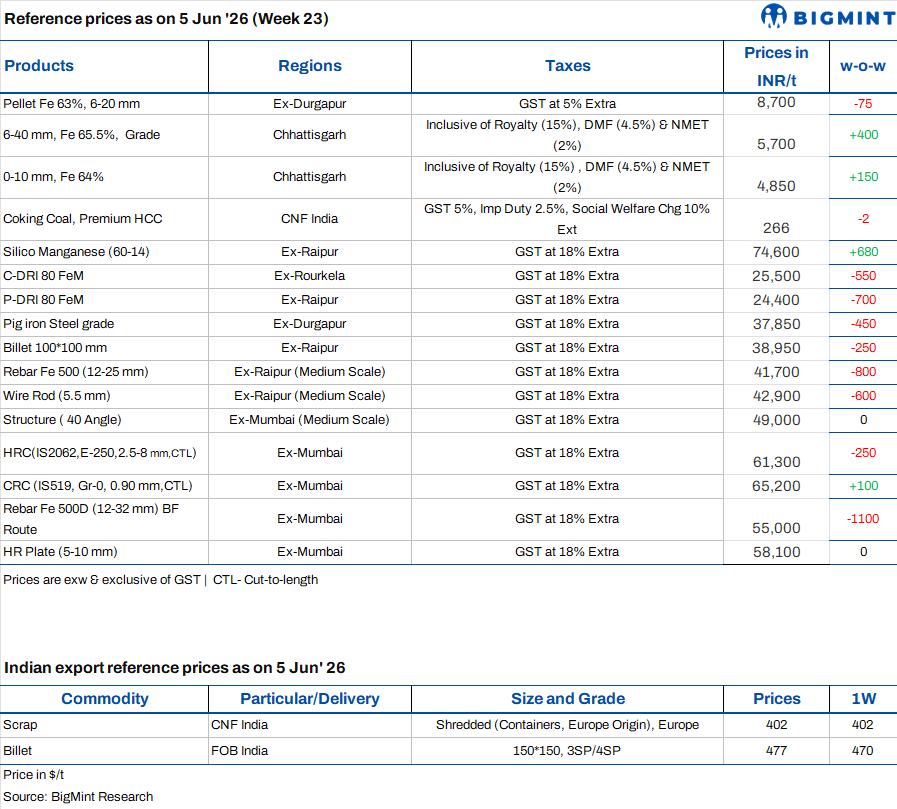

- India's largest merchant iron ore mining company, NMDC, has increased its list prices of iron ore CLO (calibrated lump ore) and fines on 3 June 2026, BigMint learnt from sources. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 6,350/tonne (t) ($65/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,850/t ($49.5/t). Prices are on FOR basis from the miner's Bacheli complex and exclude royalty, DMF, and NMEDT. Prices of all grades rose in the range of INR 150-200/t.

- PELLEX, BigMint's bi-weekly domestic pellet (Fe 63%) index for Raipur, declined by INR 100/t ($1/t) w-o-w to INR 9,400/t ($99/t) DAP, as Raipur-based pellet producers lowered offers earlier in the week. However, NMDC's June iron ore price hike in Chhattisgarh lent support to the market, partly offsetting the impact of the local price reductions.

- BigMints bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $2/t w-o-w to $54.5/t FOB east coast (equivalent to $70.5/t CFR China) on 4 June 2026, amid subdued buying interest from Chinese steel mills and softer global iron ore prices. Trading activity remained limited, as a widening gap between bids and offers restricted the closure of fresh export transactions.

- During SAIL auctions held from Monday to Thursday, around 40,000 t of iron ore dump fines (Fe 58.71-58.99%) were booked at prices ranging between INR 3,260-4,050/t. The prices were on an ex-mines basis, inclusive of royalty, DMF, NMET, and additional premium charges.

Ferrous scrap

- The imported ferrous scrap market remained weak during the week, pressured by poor steel demand, weak mill margins, monsoon-related demand concerns, and the continued preference for domestic scrap and sponge iron. High freight costs and rupee depreciation further reduced import viability, keeping most buyers on the sidelines.

- Trading activity remained limited, with a few spot deals reported, including Brazil-origin HMS 80:20 at around $330/t CFR India and shredded scrap at $405/t CFR Nhava Sheva. UK/EU-origin HMS 80:20 offers were heard at $345-360/t CFR, while buyers remained focused on clearing inventories and recently arrived cargoes amid weak demand and a persistent bid-offer gap.

- Approximately 2,500-3,000 t of imported ferrous scrap, including HMS 80:20 and shredded grades, were heard booked into India over the past seven days.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices inched up by INR 425/t ($4/t) w-o-w to INR 74,400-75,400/t ($778-787/t) across key markets. Prices edged higher due to improving domestic and export demand, strengthening seller confidence and enabling smelters to maintain firm offers. Meanwhile, HC 65-16 silico manganese export prices edged up by $1/t to $906/t FOB Vizag/Haldia.

- However, state-owned MOIL Limited has cut manganese ore prices, effective 1 June 2026. Prices of ferro grades with over 44% Mn content were decreased by 6%, while grades below 44% saw a 5% drop. Within the SMGR segment, prices of Mn 30%, Mn 25%, fines, and chemical grades were also reduced by 5%.

- Ferro manganese: Indian ferro manganese (70%) prices remained largely stable, with a slight rise of INR 400/t ($4/t) w-o-w to INR 78,400/t ($819/t) in Raipur and by INR 300/t ($3/t) to INR 78,300/t ($817/t) in Durgapur. The increase was driven by improved buying interest and firm market sentiment, which supported a modest rise in ferro manganese prices. Meanwhile, export prices for the 75% grade also increased by $4/t w-o-w to $912/t FOB Vizag/Haldia.

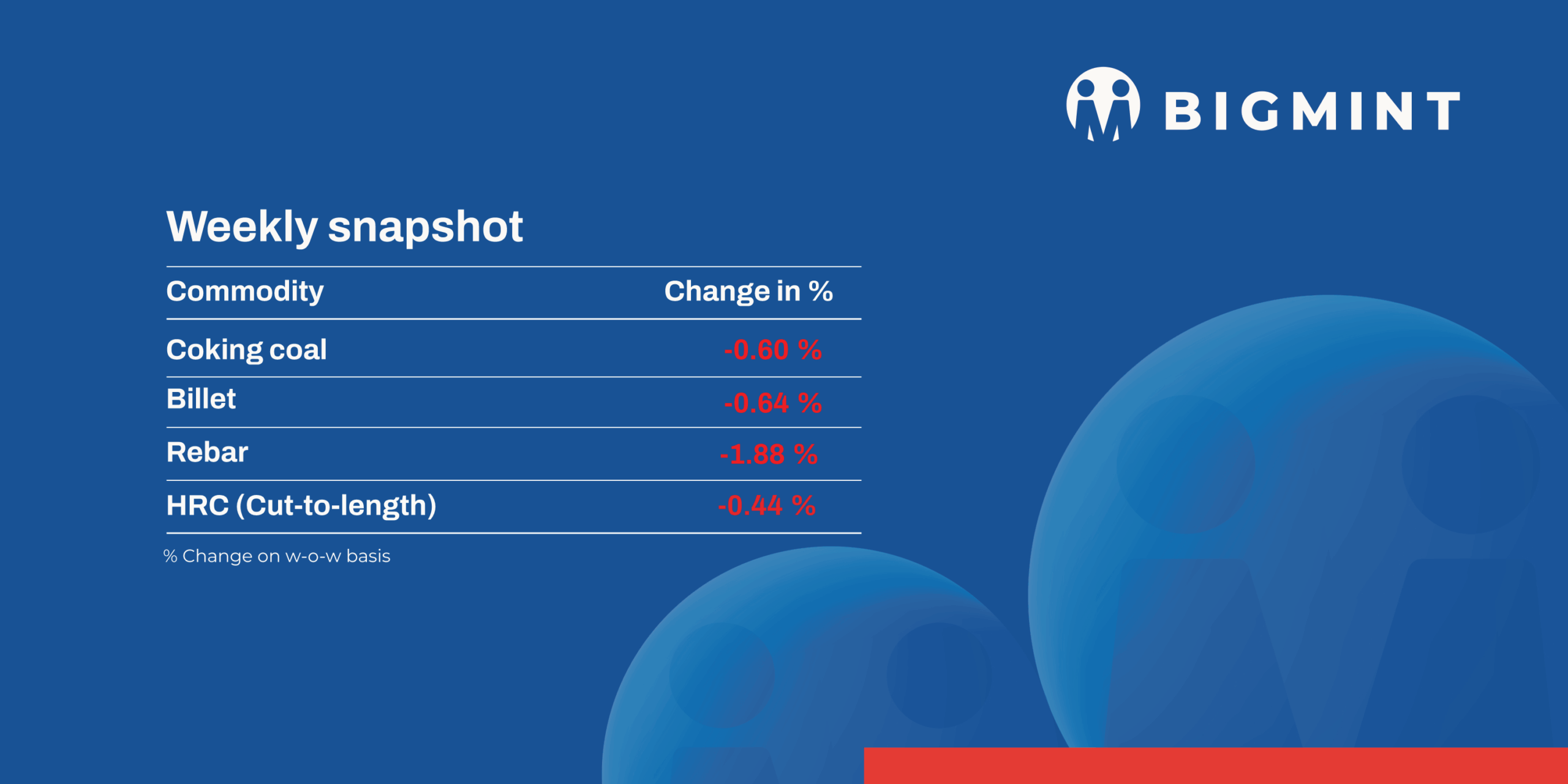

- Ferro silicon: India ferro silicon (Si 70%) prices fell by INR 1,500/t ($16/t) w-o-w to INR 98,500/t ($1,028/t) ex-works Guwahati, while Bhutan prices were also down by INR 1,400/t ($15/t) to INR 98,600/t ($1,029/t). Prices dropped following Bhutan's offer declaration for this month at INR 99,000/t ($1,034/t) exw.

- Ferro chrome: India high-carbon ferro chrome (HC 60%, Si 4%) prices rose by INR 1,200/t ($13/t) w-o-w to INR 122,200/t ($1,274/t) ex-works Jajpur.Prices increased due to tight supply, supported by strong auction bids, favourable export arbitrage, and steady procurement from end users.

Semi finished

- India's semi-finished steel market witnessed a moderate correction this week, as per BigMint's assessment. Domestic billet prices across key regions declined by INR 300-1,300/t ($3-13/t) w-o-w, as sellers lowered offers in an attempt to stimulate buying interest. The reduction in prices resulted in a modest improvement in booking activity compared to the previous week. The sharpest correction was recorded in Hyderabad, where billet prices fell by INR 1,300/t ($13/t) amid weak demand and slow offtake in the finished steel segment, which failed to provide the necessary support for market recovery.

- The sponge iron (DRI) market also moved lower, mirroring the trend seen in billets. Pan-India sponge iron prices declined by INR 200-700/t ($2-7/t) w-o-w, as soft demand and volatile market sentiment continued to weigh on prices. While booking activity improved moderately at lower price levels, overall procurement remained cautious. In contrast, the Chennai market remained stable, with limited activity and slow market movement kept prices unchanged.

- On the export front, Indian DRI offers remained firm with marginal weakness, while bookings improved from neighbouring countries as buyers showed greater interest at lower price levels. Export offers to Nepal edged down by $1/t w-o-w to $310/t CPT Raxaul, whereas offers to Bangladesh remained unchanged at $316/t CPT Benapole. The stable-to-soft pricing environment helped improve export transactions this week.

- SAIL-Rourkela Steel Plant (RSP) auctioned 3,400 t of steel-grade pig iron on 2 June 2026, with the entire quantity booked at an average price of INR 37,150/t exw. The auction price declined by INR 400/t compared to the previous auction held on 28 May, when only 1,600 t out of 5,000 t offered were sold at INR 37,550/t exw.

- NMDC Nagarnar Steel Plant auctioned 12,000 t of steel-grade pig iron on 2 June 2026, with the entire quantity booked at the base price of INR 36,000/t exw. The booking price was INR 500/t lower than the previous auction on 29 May, where only 3,000 t out of 12,000 t offered were sold at INR 36,500/t exw. The improved booking response at lower prices suggests that consumers utilised the correction to replenish inventories, although overall sentiment across the steel value chain remains cautious.

Finished long steel

- IF-rebar: IF-route rebar prices witnessed a downward trend across major markets this week, while overall trading activity remained subdued. Buyers continued to adopt a need-based procurement approach and resisted higher offer prices, limiting market participation. Sellers attempted to push prices higher amid expectations of improved demand; however, weak buying interest at elevated levels forced them to offer discounts to conclude deals.

- Market sentiment remained cautious throughout the week, with most participants preferring to wait for clearer price signals before making bulk purchases. Mill inventory levels were reported at around 12-15 days, indicating rising inventory pressure in the mills.

- IF-route rebar prices are expected to remain under pressure in the near term amid subdued demand and cautious buying activity. However, any upward movement in billet and sponge iron prices could lend cost-side support and help stabilise rebar prices.

- On a w-o-w basis, rebar prices declined by INR 200-1,300/t across key regions, with the sharpest decline observed in the southern region, according to BigMint's assessment.

- BF-rebar: India's BF-route steelmakers reduced June 2026 rebar list prices by INR 1,000-4,000/t to INR 55,250-57,700/t exy Mumbai, responding to weak buying enquiries, limited distributor bookings, and mounting inventory pressure across the supply chain.

- The correction was also influenced by sluggish construction activity amid extreme heatwave conditions and a nearly INR 10,000/t gap between BF-route and IF-route rebar prices during May.

Flat steel

- BigMint's bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.58 mm/CTL) inched down by INR 200/t ($2/t) w-o-w to INR 58,300/t ($612/t) as of 5 June against INR 58,500/t ($614/t), a week ago. However, CRC (IS513, Gr O, 0.9 mm/CTL) remained stable w-o-w at INR 65,200/t ($684/t) on 5 June.

- Leading mills have rolled over flat steel prices for June sales as weak demand and cautious market sentiment persist.

- India's bulk imports of HRCs touched 423,925 t in May. Around 154,895 t of additional cargoes are expected by early-July.

- India's bulk exports of HRCs touched 231,749 t in May. Around 20,465 t of additional cargoes are expected to be shipped.

- Indian HRC export activity remained subdued, with unchanged offers due to regulatory uncertainty in Europe. Moreover, logistical disruptions, coupled with Eid-related slowdowns in the Middle East, continued to weigh on demand.