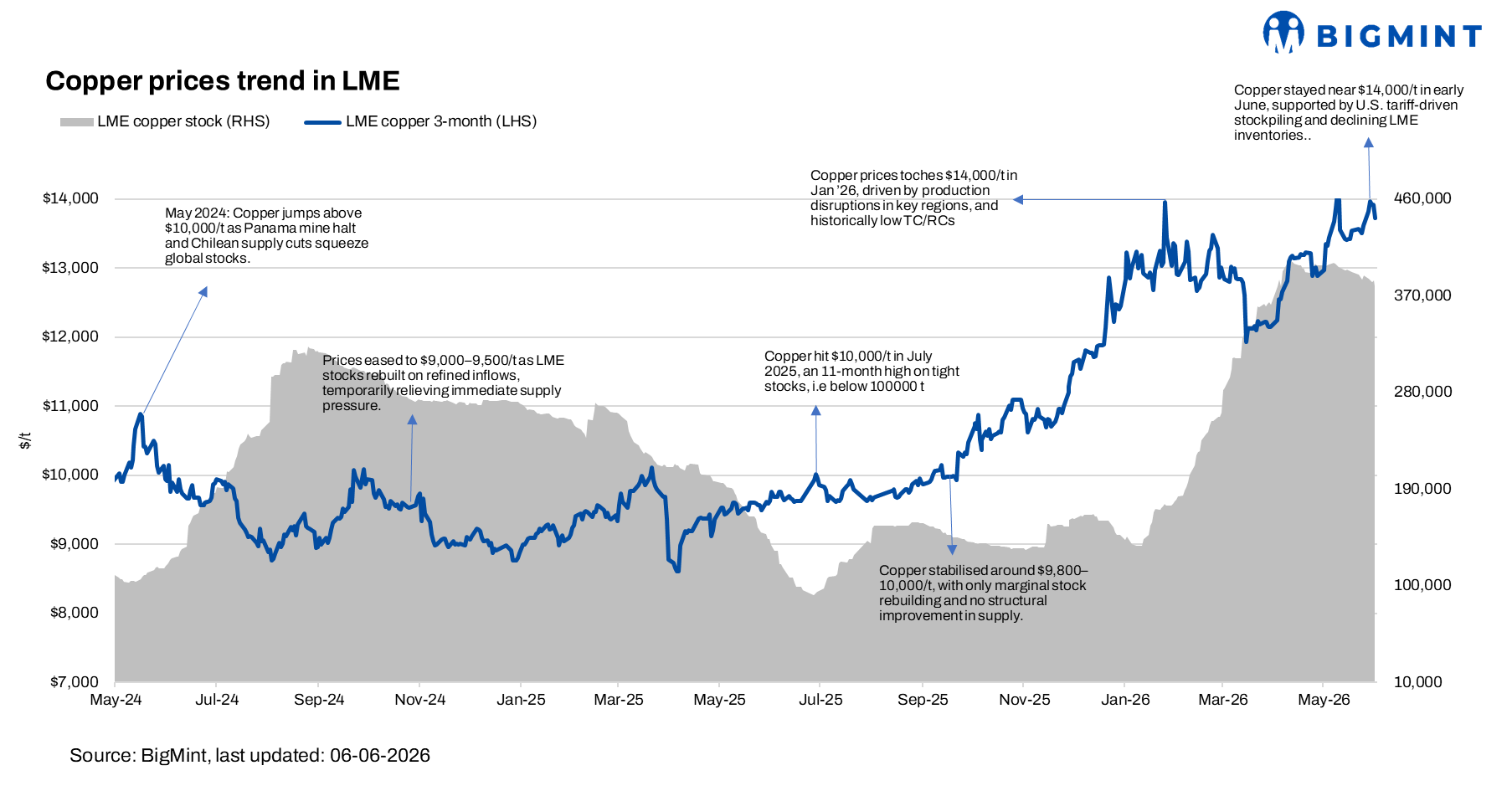

LME copper trades near record highs amid US stockpiling and tightening global supplies

...

- Copper hovers near record highs around $14,000/t weekly

- Trafigura-led stock withdrawals tighten LME supply

Benchmark copper prices on the London Metal Exchange (LME) remained elevated this week, hovering near the record-high level of $14,000/t during the first half of the week. However, prices eased towards the end of the week, settling at approximately $13,700/t on Friday amid profit-booking. Prices continued to draw support from expectations of potential US tariffs on copper imports, which have encouraged sustained inventory movements into the US market and tightened available supplies elsewhere.

Additional support came from significant cancellations of LME warehouse stocks in New Orleans, where more than 30,000 t of copper was earmarked for delivery during the week. Total cancelled stocks across the LME system approached 30% of overall inventories, reflecting strong demand for physical metal and reinforcing concerns over tightening nearby availability.

The tightening supply situation was also reflected in the LME forward curve. The premium of the cash copper contract over the benchmark three-month contract surged to its highest level in more than two years during the week, highlighting increasing competition for prompt material.

However, gains were partially capped towards the end of the week as the nearby premium eased and investors booked profits after copper approached record-high levels.

Overall, copper prices remained well supported during the week, driven by tightening availability outside the US, elevated warehouse cancellations, and continued tariff-related inventory shifts, although profit-taking limited further upside near record highs.

Global updates

China's infrastructure push fuels copper demand amid supply hurdles

Copper market fundamentals remained supportive, driven by resilient Chinese demand and tightening inventories. China's unwrought copper imports rose 3.2% y-o-y in April to a seven-month high, while power grid investment surged 37% y-o-y in Q1 2026, supporting consumption across infrastructure and electrification sectors.

On the supply side, sulfur shortages in Chile and delayed recoveries at major mines such as Grasberg and Kamoa-Kakula continued to constrain output growth. While the ICSG still expects a refined copper surplus in 2026-27, Goldman Sachs and Citi have raised their price forecasts, citing slower mine supply growth, strong US imports, and robust demand trends.

India's updates

India continued strengthening its position as a key destination for Japanese copper material, with imports from Japan rising around 14% y-o-y during January-April 2026 to nearly 0.08 mnt. The increase reflects growing demand from infrastructure, renewable energy, cable manufacturing, EVs, and precision engineering sectors, alongside India's rising requirement for high-quality copper semis and refined products.

Hindustan Copper Ltd (HCL) awarded LOHUM the rights to revive and operate the dormant Gujarat Copper Project under a 20-year revenue-sharing agreement. The project includes a 50,000 t/year secondary copper smelter and refinery, which will be upgraded to produce high-purity Grade-A copper cathodes, supporting India's growing copper demand.

Outlook

Copper's outlook remains positive, with Goldman Sachs forecasting a deeper non-US copper deficit over the next two years due to continued US stockpiling and delayed recoveries at key mines, including Grasberg and Kamoa-Kakula. As a result, the bank has raised its long-term copper price forecasts, citing tighter global supply conditions.

However, prices may remain vulnerable to bouts of profit-booking after the recent rally towards record highs. Any clarity regarding US tariff policy and the pace of inventory withdrawals from exchange warehouses will remain key factors influencing price direction in the coming weeks.