Global coking coal market diverges as premium HCC holds firm but broader weakness emerges

...

- Tight availability, Chinese demand supports PHCC

- Chinese supply recovery pressures domestic prices

The global seaborne metallurgical coal market is showing the first signs of divergence after several weeks of strength. While premium hard coking coal (HCC) prices remained resilient in the week ended 27 June 2026, supported by Chinese buying interest and limited spot availability, weakness is beginning to emerge across lower-quality coking coal grades and the broader Chinese domestic market.

The latest market developments suggest that the rally may be entering a more mature phase. Domestic mine production in China is gradually recovering, auction activity has weakened, unsold cargoes are beginning to appear, and Indian steel mills continue to purchase cautiously amid subdued steel margins.

At the same time, Chinese coke producers have announced another round of domestic coke price increases, highlighting the complex balance between tightening coke supply and increasingly cautious raw material procurement.

Premium hard coking coal continues to outperform

Premium low-vol (PLV) hard coking coal remains the strongest performer in the seaborne metallurgical coal market.

FOB Australia prices have remained around$243-244/t, while CFR China values continue to trade near$265/t, maintaining a healthy arbitrage for cargoes destined for China.

The resilience reflects two key factors. First, the availability of premium Australian cargoes remains limited, with very few prompt-loading parcels available in the spot market. Second, Chinese steel mills continue to favour premium-quality coking coal that improves blast furnace productivity and reduces coke consumption, particularly as steel production remains relatively healthy.

The result is a market where premium material continues to command strong support despite broader uncertainty.

Weakness spreads across lower-quality grades

The picture is markedly different for lower-quality coking coal. Low-vol hard coking coal (LVHCC) prices have started to weaken as buying activity slows.

Chinese buyers are increasingly sourcing lower-grade coal from domestic mines and port inventories rather than committing to forward seaborne cargoes. Several traders also reported a growing number of unsold cargoes seeking buyers, particularly among non-premium Australian and Canadian coals.

The divergence between premium and lower-quality material suggests buyers are becoming increasingly selective rather than uniformly bullish.

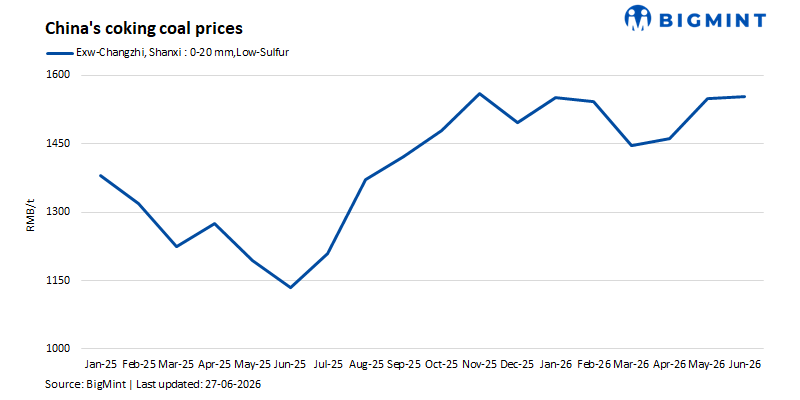

Chinese domestic market begins to soften

Another notable development is the gradual softening of China's domestic coking coal market.

Although premium grades remain relatively firm, several domestic coal auctions have reportedly attracted limited participation, with some lots either remaining unsold or clearing at lower prices. At the same time, domestic mine production has started recovering following earlier production constraints. The gradual return of domestic supply is reducing the urgency for Chinese mills to secure imported cargoes at elevated prices.

Market participants are also awaiting adjustments to July domestic long-term contract prices, which are expected to influence buying decisions for imported coal during the coming weeks.

Indian buying remains measured

Indian steel producers continue to adopt a cautious procurement strategy. Although seaborne prices remain well below the peaks witnessed during 2022 and 2023, weaker domestic steel prices and comfortable raw material inventories have limited aggressive spot buying.

Instead, many mills continue to purchase only against immediate production requirements while monitoring developments in both Australia and China. The absence of strong Indian buying has removed an important source of support for the seaborne market and has contributed to the softer tone developing across lower-quality grades.

Coke market tells a different story

Interestingly, developments in the coke market continue to contrast with those in coking coal.

Chinese coke producers have announced a ninth consecutive round of domestic coke price increases since early March, proposing another increase of RMB 50-55/t. ($7-8/t). The proposed increase reflects continued supply discipline among coke producers and relatively healthy demand from steel mills.

However, higher coke prices have not translated into stronger demand for imported coking coal. Instead, steel producers appear increasingly focused on controlling raw material costs, purchasing premium coal where operationally necessary while limiting exposure to higher-priced lower-quality imports.

This divergence highlights that the coking coal and coke markets are no longer moving in lockstep.

Freight provides some support

Lower freights have partially offset recent weakness in seaborne coal prices. Reduced shipping costs have improved the competitiveness of Australian cargoes delivered into China and other Asian markets.

This has helped maintain healthy arbitrage opportunities for premium Australian HCC despite relatively stable FOB prices. However, freight savings alone are unlikely to offset the impact of weaker buying should domestic Chinese supply continue improving.

Outlook

The metallurgical coal market is entering a more balanced phase after several weeks of strong performance. However, a clear two-tier market is emerging. Premium hard coking coal continues to benefit from structural supply constraints and steady Chinese demand, while lower-quality grades are becoming increasingly vulnerable to recovering domestic production and more cautious purchasing behaviour.

For market participants, this divergence means product quality is once again becoming a critical pricing driver. Premium hard coking coal is likely to remain relatively well supported due to limited spot availability and continuing Chinese demand for high-quality material.

However, downside risks are increasing for lower-quality grades. A combination of recovering Chinese mine production, weaker domestic auctions, cautious Indian buying, and growing availability of unsold cargoes suggests that price pressure could gradually spread across the broader market.

The next major determinant will be China's July domestic contract prices and the pace of steel production during the third quarter. Should Chinese steel output remain robust, premium HCC is likely to retain its relative strength even if lower grades continue to weaken.

Overall, the coming weeks will determine whether weakness remains confined to secondary grades or eventually spreads into the premium segment that has underpinned the market's resilience throughout the second quarter.