Global bunker prices decline w-o-w amid crude oil correction

...

- Crude oil correction weighs on bunker prices

- Middle East tensions ease, improving supply outlook

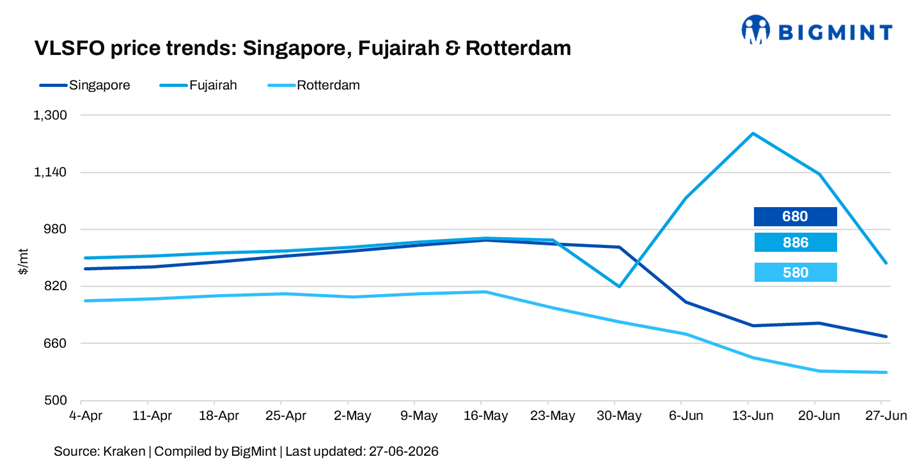

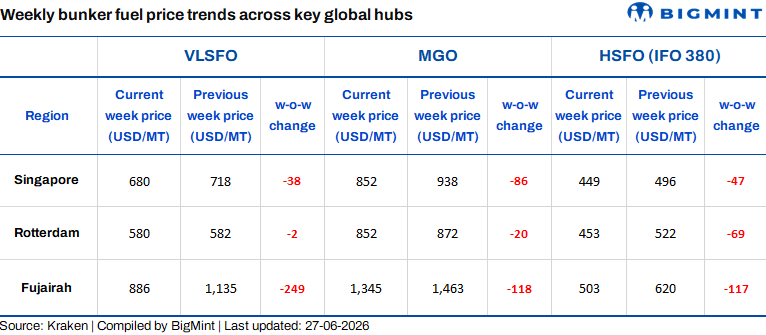

Global bunker fuel prices moved mostly lower in the week ended 26 June 2026, mirroring the sharp correction in crude oil markets following easing geopolitical tensions in the Middle East. Benchmark VLSFO prices in Singapore stood at $680/metric tonne (mt), down by $38/mt w-o-w, while Fujairah witnessed the steepest decline as concerns over supply disruptions through the Strait of Hormuz eased.

Regional bunker markets

- Singapore: VLSFO prices stood at $680/mt on 27 June, down by $38/mt w-o-w. Prices weakened amid lower crude oil benchmarks and ample bunker fuel availability, with buying interest remaining cautious as shipowners anticipated further softness in fuel costs.

- Rotterdam: VLSFO prices stood at $580/mt, down by $2/mt w-o-w. The marginal decline reflected a well-supplied market and stable bunker demand across Northwest Europe, limiting sharper price movements despite the broader fall in crude oil prices.

- Fujairah: VLSFO prices fell sharply by $249/mt w-o-w to $886/mt, as easing geopolitical tensions and the normalization of vessel movements through the Strait of Hormuz triggered a steep unwinding of the regional risk premium.

Factors influencing bunker prices

- Brent crude futures decline w-o-w: Brent crude oil (August 2026 contract) was assessed at $72.78/barrel (bbl) on 26 June, down $7.12/bbl w-o-w, as easing geopolitical tensions in the Middle East and the resumption of oil shipments through the Strait of Hormuz reduced the geopolitical risk premium.

- WTI crude falls sharply: WTI futures declined 9.55% w-o-w to $69.23/bbl on 27 June from $76.54/bbl a week earlier, pressured by easing Middle East tensions, improved oil supply outlook, and expectations of higher OPEC+ production.

Outlook

Global bunker fuel sentiment is expected to remain soft in the near term. Lower crude oil prices and improving oil flows through the Strait of Hormuz are likely to keep bunker prices under pressure across major hubs.

However, refining margins remain healthy and refined fuel availability in Asia continues to be relatively tight, which could limit further downside, particularly for low-sulphur marine fuels.