Weekly round-up: LME base metals trade mixed w-o-w; Indian prices broadly ease

...

- Aluminium scrap prices track weaker LME cues

- HZL cuts zinc and lead prices

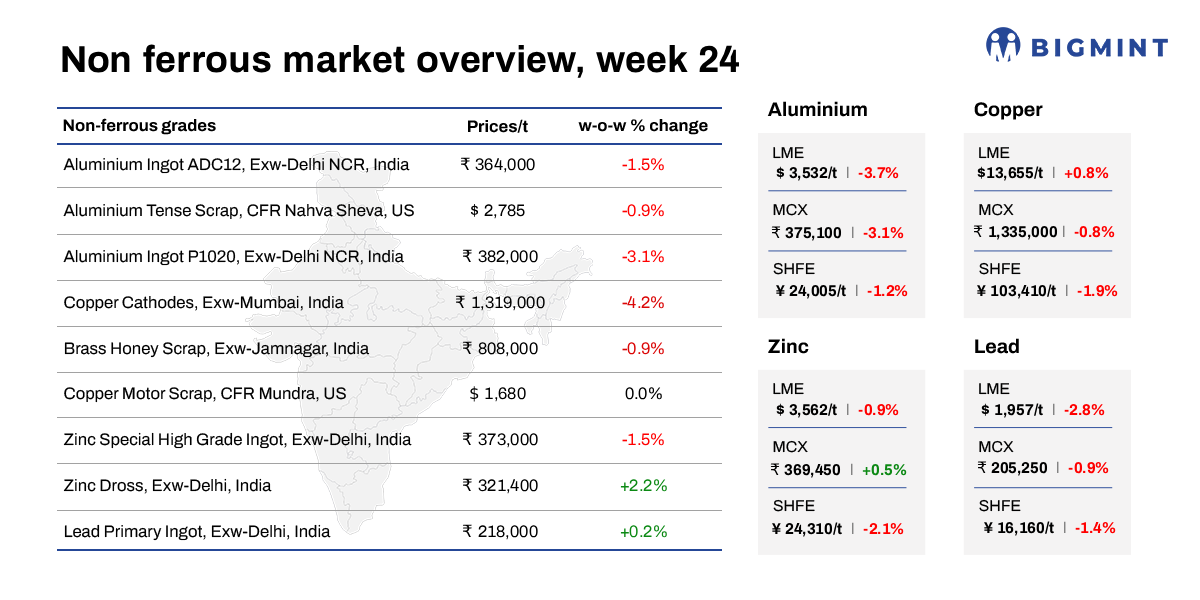

LME base metals prices showed a broadly weaker trend in the week ended 5 June 2026. Aluminium declined 3.7% to $3,532/t from $3,669.5/t, while copper eased 0.8% to $13,655/t from $13,763/t. Zinc edged down 0.9% to $3,562/t compared with $3,594.5/t, and lead fell the most, dropping 2.8% to $1,957/t from $2,013/t.

On the inventory side, base metals stocks showed a broad-based decline in the week ended 12 June 2026. Copper inventories recorded the steepest fall, easing 3.99% to 364,100 t, followed by aluminium, which declined 3.98% to 319,925 t. Zinc stocks fell 2.89% to 107,750 t, while lead registered the mildest decline, down 1.44% to 305,875 t.

Aluminium

India's imported aluminium scrap prices traded lower w-o-w, tracking softer trends in LME aluminium prices. According to BigMint's latest assessment for CFR Nhava Sheva deliveries, UK-origin zorba 95-5 scrap prices declined by $15/t w-o-w to $3,025/t from $3,040/t previously, reflecting subdued buying interest and weaker conditions in overseas scrap markets.

Domestic aluminium prices in India declined significantly w-o-w as of 12 May'26, pressured by weaker trends on both the Multi Commodity Exchange (MCX) and the London Metal Exchange (LME).

According to market assessments, P1020 ingot prices in Delhi NCR declined by INR 12,000/t (3%) w-o-w to INR 382,000/t on 12 May'26, from INR 394,000/t on 5 May'26.

NALCO reduced its primary aluminium ingot (P1020, 99.7%) prices by INR 14,000/t ($154/t) on 10 Jun'26, reversing the gains recorded in the previous revision amid weaker global aluminium market trends.

Copper

Copper scrap prices in India declined w-o-w on 10 June 2026, as benchmark prices fell and domestic market sentiment remained cautious. London Metal Exchange (LME) copper prices fell $400/t to around $13,430/t from $13,900/t a week back, as traders booked profits after the recent rally and remained cautious amid macro-economic uncertainty.

At the domestic level, buying activity remained largely requirement-driven across key trading hubs. According to BigMint's assessment, copper armature scrap, ex-Delhi, fell around 2% w-o-w to INR 1,260,000/t from INR 1,280,000/t last week.

Copper cathode prices in western India declined w-o-w on 11 June 2026 following subdued demand and a correction in global copper prices, leading to lower domestic offers.

As per BigMint's assessment, ex-Mumbai copper cathode prices fell to around INR 1,319,000/t on 11 June from nearly INR 1,377,000/t last week.

India's brass honey scrap prices declined w-o-w on 12 June 2026, pressured by subdued demand and softer global prices. BigMint's assessment placed brass honey scrap prices at around INR 808,000/t exw-Jamnagar, down by INR 7,000/t w-o-w.

Zinc

India's zinc ingot (99.995%) prices declined w-o-w by around INR 7,700/t ($90/t) to INR 376,300/t ($4,395/t) ex-Delhi on 9 June 2026, pressured by softer global zinc prices and weaker producer pricing.

Demand from galvanisers and alloy manufacturers remained largely need-based, with buyers limiting purchases to immediate requirements amid sluggish downstream consumption.

Domestic sentiment weakened after Hindustan Zinc Ltd (HZL) reduced zinc ingot prices by INR 2,300/t ($27/t) on 8 June.

HZL's benchmark SHG zinc prices were lowered to INR 381,300/t ($4,451/t), narrowing the gap with spot market levels.

Lead

On the London Metal Exchange (LME), lead prices remained largely unchanged at $1,962/t as of 12:30 PM IST.

Lead prices in India showed a mixed trend in the week ended 12 June 2026. Lead remelted ingot (Pb 99%) stood at 206,000/t, while lead primary ingot (Pb 99.99%) increased 0.23% to 218,000/t.

Hindustan Zinc Ltd (HZL) on 11 June 2026 reduced lead ingot prices by INR 2,400/t ($28/t) compared with its previous revision announced on 8 June.

Following the revision, HZL's benchmark Special High Grade (SHG) lead ingot prices declined to INR 225,300/t ($2,631/t).

Other updates

Norsk hydro declares second force majeure on qatalum aluminium sales

Norsk Hydro has declared a second force majeure on aluminium sales from its Qatalum joint venture in Qatar after the smelter terminated its marketing agreement with the company. The move follows an earlier disruption in March 2026 due to gas supply issues amid Middle East tensions, which had already led to partial curtailment of operations. Although production has resumed at around 60% capacity, Hydro has disputed the termination and warned of possible delivery disruptions, adding further uncertainty to global aluminium supply.