Weekly round-up: LME base metals prices gain w-o-w; Indian markets show resilience

...

- LME stocks show mixed trends, indicating selective tightness

- Firm Indian scrap demand meets restricted availability

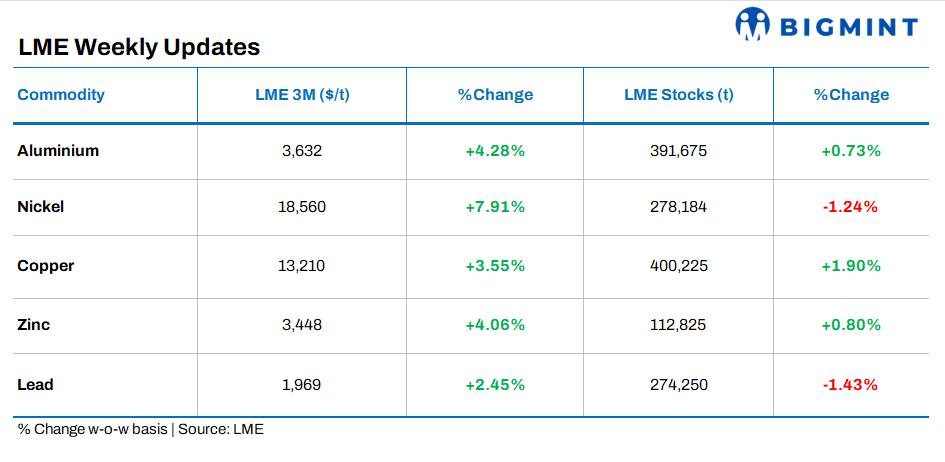

LME base metals moved higher on a w-o-w basis as of 17 April 2026, reflecting improved sentiment across the complex. Nickel recorded the strongest gain of 7.91% to $18,560/t, followed by aluminium, which was up 4.28% to $3,632/t. Similarly, zinc was up 4.06% to $3,448/t, copper increased 3.55% to $13,210/t, and lead gained 2.45% to $1,969/t.

On the inventory side, trends were mixed. Copper stocks saw a notable increase of 1.90% to 400,225 t, while aluminium inventories edged higher by 0.73% to 391,675 t, and zinc stocks rose 0.80% to 112,825 t. In contrast, nickel inventories declined by 1.24% to 278,184 t, and lead stocks fell 1.43% to 274,250 t, indicating selective tightness in supply.

Aluminium

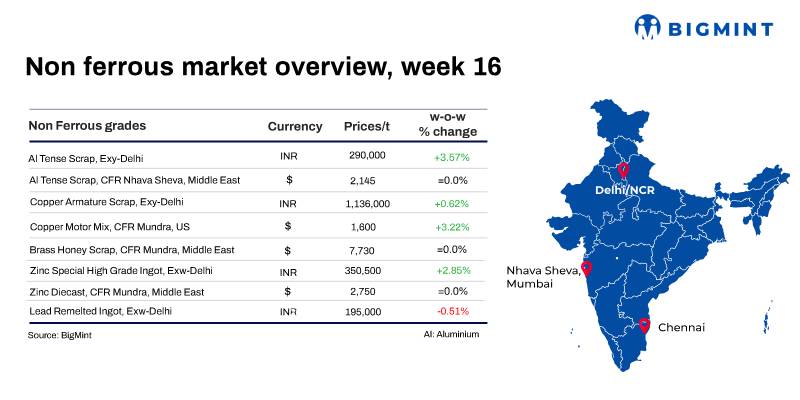

India's imported aluminium scrap market displayed a steady-to-firm trend w-o-w as of 17 April 2026, supported by elevated global benchmarks, although momentum moderated towards the end of the week in line with a cooling LME trend.

As per the latest assessment, UK-origin Zorba 95-5 scrap, CFR Nhava Sheva, remained stable w-o-w at $2,870/t, showing no change from the previous week. Meanwhile, US-origin tense scrap (6-7%), CFR Nhava Sheva, increased to $2,745/t from $2,580/t, marking a sharp rise of $165/t w-o-w, reflecting a strong recovery after prior weakness and continued buying interest.

On the domestic front, sentiment softened. P1020 aluminium ingot, ex-Delhi NCR, was assessed at INR 375,000/t, increasing INR 16,500/t w-o-w from INR 358,500/t. This correction reflects the easing in global benchmarks after the recent peak, even as prices continue to hover at relatively elevated levels supported by tight inventories.

Overall, while imported scrap markets remained resilient, the domestic ingot segment showed a firm upward trend, supported by stronger pricing, even as the broader LME aluminium trend moderated after recent highs.

Copper

India's copper scrap market witnessed a firm uptrend w-o-w as of 17 April, supported by gains in LME copper prices, alongside improving demand from the key consuming hub of Jamnagar.

The upside was supported by active procurement from brass manufacturers and recyclers, amid a pickup in downstream activity. At the same time, tight spot availability of scrap and limited arrivals continued to exert upward pressure on prices, with market participants reporting constrained supply conditions.

As per BigMint's assessment, brass honey scrap, exw-Jamnagar, increased by INR 40,000/t w-o-w to INR 770,000/t from INR 730,000/t, reflecting strong buying interest during the period.

Overall, improved domestic demand and restricted scrap availability remained the key price drivers, while supportive global cues provided additional strength, keeping market sentiment firm despite some resistance at elevated levels.

Zinc

India's zinc ingot (Zn 99.995%) prices inched up w-o-w as of 14 April, supported by stable spot demand and marginally firmer global cues. SHG zinc ingot, ex-Delhi, increased by INR 1,000/t to INR 343,000/t from INR 342,000/t a week earlier, reflecting steady procurement from galvanizing units.

The uptick tracked firm LME zinc trends, indicating continued support from global markets. On the domestic front, Hindustan Zinc Limited (HZL) increased zinc ingot prices by INR 6,300/t to INR 349,000/t, ex-Chanderiya, aligning with prevailing market strength.

In the secondary segment, prices also moved higher. Zinc dross, ex-Delhi, increased by INR 4,000/t to INR 279,000/t, while western India levels were reported at around INR 277,000/t ex-works. Meanwhile, zinc oxide (99% Zn) prices rose by INR 4,600/t to INR 269,600/t, ex-Delhi, supported by steady downstream demand.

Overall, firm global cues and stable domestic demand supported the upward bias in primary prices, while cautious buying activity in the secondary segment continued to limit sharper gains despite the positive trend.

Lead

India's domestic lead market remained largely stable with a marginal downward bias w-o-w as of 17 April 2026. Lead primary ingot, ex-Delhi, was assessed at INR 203,000/t, down INR 1,100/t w-o-w from INR 204,100/t, while lead remelted ingot, ex-Delhi, declined to INR 195,000/t, easing INR 1,000/t w-o-w from INR 196,000/t, reflecting slightly subdued spot demand.

The softening in prices came despite recent revisions from Hindustan Zinc Limited (HZL), which increased lead ingot prices by INR 2,300/t to INR 212,300/t, ex-works, aligning with relatively firm global cues. LME lead was also trading marginally higher at around $1,969/t, providing some underlying support.

Overall sentiment remained stable to slightly weak, with minor corrections seen in domestic prices despite producer price hikes, as balanced demand-supply conditions and cautious buying activity limited upward momentum.

Other updates

Chinese copper smelters may press ahead with production curbs amid acid export ban

China's copper smelters are likely to move forward with output cuts following Beijing's decision to ban sulphuric acid exports, which is expected to pressure prices of the key by-product.

The export ban will increase domestic acid availability, potentially reducing smelter revenues at a time when treatment charges are already at historic lows due to tight concentrate supply. As a result, several smelters may advance maintenance schedules or trim production to manage margins.

Overall, the development signals a potential tightening in refined copper supply in the near term.