Weekly round-up: Indian steel prices show mixed trends as demand stays cautious

...

- Iron ore, pellet prices rise; domestic met coke prices climb up

- Flat steel, IF rebar prices soften amid ceasefire announcement

Indias steel market exhibited mixed trends in the week ended 10 April 2026, as strengthening iron ore and pellet prices contrasted with cautious finished steel demand, keeping overall sentiment uncertain and trade activity moderate.

In intermediates, semi-finished steel and sponge iron markets showed regional disparities, reflecting uneven demand recovery across geographies. Billet and sponge iron prices also moved in divergent directions depending on local demand conditions, while pig iron auctions indicated firm underlying demand through improved bids.

Finished steel segments remained cautious, with both long and flat products seeing limited buying and minor price corrections. Overall, the steel value chain reflects cost-push pressures at the upstream level but demand-side hesitancy downstream.

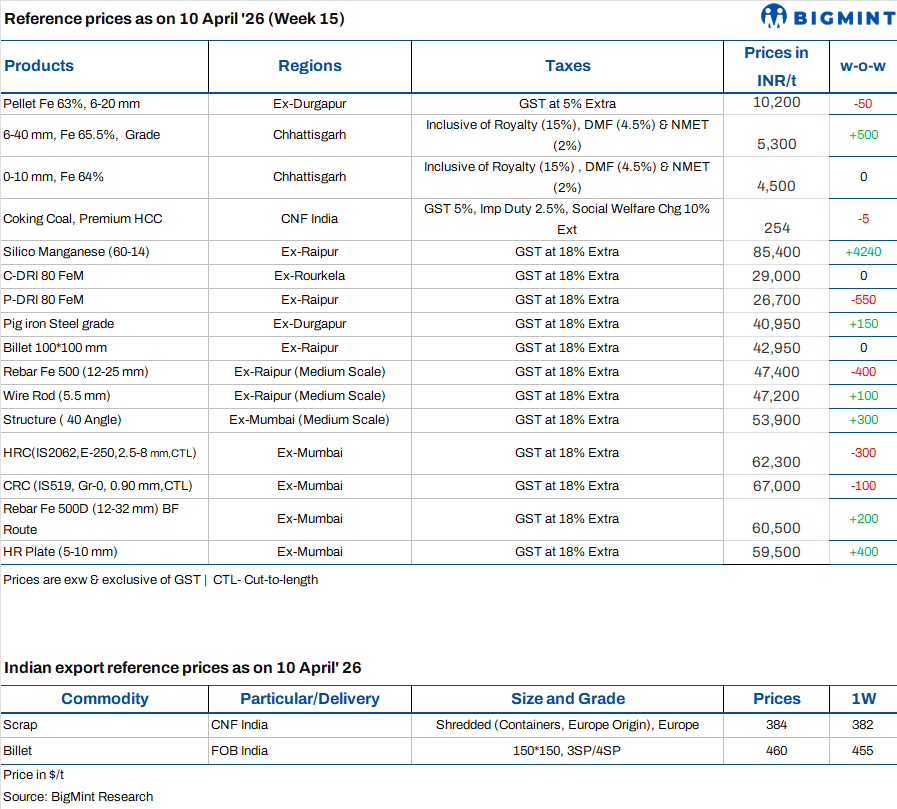

Iron ore, pellet

- India's largest merchant iron ore mining company, NMDC, announced its list prices of iron ore CLO (calibrated lump ore) and fines on 5 April 2026, BigMint learnt from sources. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 5,900/tonne (t) ($63/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,500/t ($48/t). Prices are on FOR basis from the miner's Bacheli complex and exclude royalty, DMF, and NMEDT. Prices of all grades were raised by INR 450-550/t.

- Lloyds Metals and Energy has raised its prices for iron ore fines, lumps, and pellets in Chandrapur by INR 400-500/t. Iron ore fines (Fe 63%) increased by INR 400/t ($4/t) w-o-w to INR 6,600/t ($71/t) FOR Balharshah as of 5 April 2026. Lump offers rose by around INR 500/t ($5/t) to INR 9,885/t ($106/t) FOR Chandrapur, while pellet prices were also hiked by INR 500/t ($5/t) to INR 11,835/t ($127/t) exw. The revision reflects improving domestic fundamentals, supported by firm steel prices and stronger sponge iron demand, along with the recent hike in NMDC's iron ore prices for April delivery from Chhattisgarh.

- PELLEX, BigMint's bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 250/t ($2/t) to INR 10,900/t ($113/t) DAP Raipur on 10 April compared to last week. Raipur-based pellet producers raised offers for Fe 62/63% (+/-0.5%) material by INR 200/t ($2-3/t) to INR 10,700-10,800/t ($115-116/t) exw. The increase in pellet prices was followed by a hike of INR 450-550/t ($5-6/t) in iron ore prices by NMDC Chhattisgarh and Lloyds Metals for April 2026 deliveries.

Coal

- South African thermal coal prices declined amid muted buyer enquiries and weak sponge iron demand. BigMint assessed exw-Paradip RB2 (5,500 NAR) down INR 200/t w-o-w at INR 11,200/t, while RB3 (4,800 NAR) slipped INR 50/t to INR 10,200/t. Continued softness in seaborne offers, lower freight, and rising port inventories further weighed on sentiment, while buyers continued favouring domestic coal over imports.

- Domestic thermal coal prices remained stable w-o-w, with 5,000 GCV assessed at INR 6,600/t and 4,500 GCV at INR 5,200/t. However, market momentum weakened as fresh SECL auction announcements increased supply-side pressure. Trading activity stayed dull during the week, and participants expect that traders may be forced to lower offers if buying interest does not improve amid the anticipated supply influx.

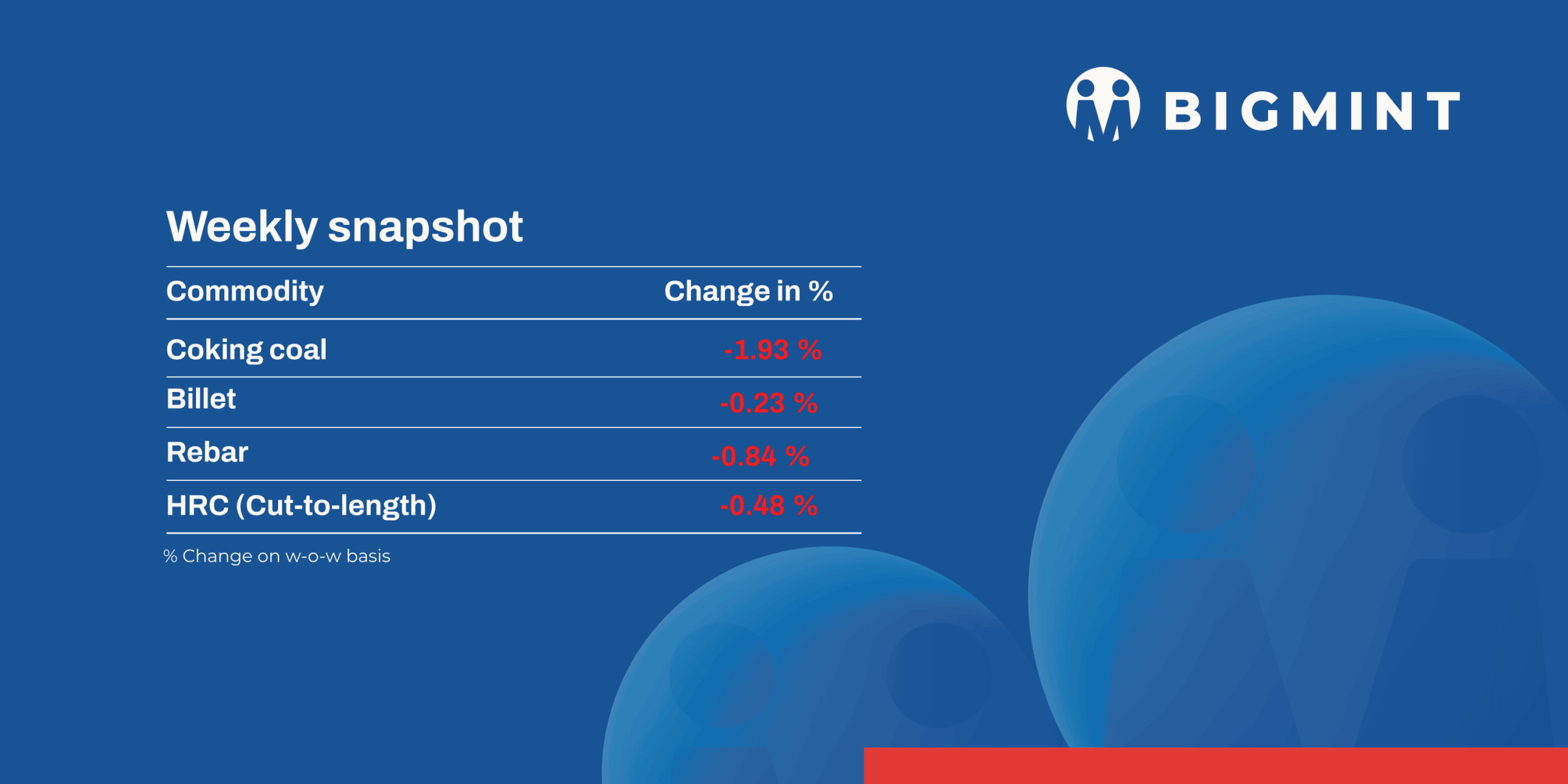

- Domestic metallurgical coke prices moved up w-o-w, supported by elevated production costs and import parity. BF-grade coke prices in eastern India rose INR 400/t to INR 36,400/t, while western India saw a sharper INR 2,500/t increase to INR 33,500/t. However, further upside remained capped due to weak trade activity and cautious procurement by steelmakers despite higher raw material-linked cost support.

- US-origin high-CV thermal coal and petcoke markets witnessed corrections this week amid slowing demand and growing buyer resistance. US NAPP coal prices at west coast ports declined by nearly INR 2,000/t w-o-w to around INR 14,500-15,500/t.

Ferrous scrap

- The imported scrap market remained weak through the week, with firm seller offers clashing against cautious buyer sentiment. HMS offers largely stayed at $380-390/t CFR, while workable buyer levels were lower at $370-375/t. Shredded offers increased to $410-420/t, but bids remained near $390-400/t, widening the spread and limiting deal activity amid weak finished steel demand and poor margins.

- Towards the end of the week, prices showed signs of stabilisation, with HMS deals reported around $370-385/t CFR, while shredded remained largely unworkable above $400/t. Notably, suppliers diverted cargoes to stronger markets like Turkiye and Bangladesh. Additionally, ceasefire-related developments eased bullish sentiment, halting further price increases.

- In the last seven days, around 4,500-5,000 t of imported scrap cargoes were reported into India, including around 4,100-4,200 t of HMS (from West Africa, South Africa, Brazil, and CI mix cargoes) and the remaining volumes comprising LMS bundle and other mixed grades.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices corrected downward after a sharp prior increase, declining by INR 525/t w-o-w to INR 84,600-85,900/t across key markets. The fall was primarily driven by abundant inventory availability and growing buyer resistance to elevated offer levels, prompting sellers to adjust quotes to stimulate transactions.

- Meanwhile, HC 65-16 silico manganese export prices remained largely stable with a marginal $6/t increase to $985/t FOB Vizag/Haldia, supported by routine trade activity. However, export sentiment remained subdued due to slow inquiry levels. Near-term outlook appears cautious, as mounting inventories and sustained production may trigger pressure selling and weigh on prices.

- Ferro manganese: Indian ferro manganese (70%) prices increased w-o-w by INR 800/t ($57/t) to INR 86,800/t ($932/t) in Raipur, while prices went up by INR 500/t ($5/t) to INR 86,500/t ($929/t) in Durgapur. Prices rose amid stronger raw material costs, firm export demand, and strong seller sentiment limiting lower-priced deals. Meanwhile, export prices for 75 grade saw a sharp increase by $38/t w-o-w to $1,006/t FOB Vizag/Haldia. However, export sentiment remained weak due to limited fresh inquiries, and the recent price rise may face downward pressure if booking activity does not improve.

- Ferro silicon: Indian ferro silicon (Si 70%) prices were stable w-o-w at INR 106,000/t ($1,144/t) exw Guwahati, while Bhutan prices edged up by INR 1,000/t ($11/t) at INR 107,000/t ($1,149/t). Following Bhutan's announcement of April ferro silicon offers at INR 106,000/t ($1,140/t) exw, sellers across Bhutan and Northeast India aligned their quotations. Steady buying interest in the market supported price stability and enabled sellers to maintain firm offers.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices were mostly stable with a slight rise of INR 500/t ($3/t) to INR 117,500/t ($1,268/t) exw Jajpur. Prices were largely steady as market conditions stayed largely muted, with limited domestic buying.

- Additionally, at Vedanta-FACOR's ferro chrome auction on 8 April, the larger lot (Cr: 56% min, 10-150 mm) achieved an H1 price of INR 116,000/t ($1,253/t) exw, higher by INR 1,000/t ($11/t) from the base price of INR 115,000/t ($1,243/t).

Semi finished

- India's semi-finished steel market witnessed a mixed trend this week, as per BigMint's assessment. Domestic billet prices in the eastern, southern, and northern regions increased by INR 150-750/t ($1.6-8/t), while the central and western regions recorded a decline of INR 200-600/t ($2-6/t) w-o-w. The variation was due to region-specific demand patterns and pricing dynamics, while weak demand and slow offtake in the finished steel segment continued to weigh on overall market sentiment.

- The sponge iron market also reflected a variation across the regions. Prices in Durgapur and Ramgarh increased by INR 250-400/t ($2-4/t), whereas central and southern regions saw a decline of INR 200-700/t ($2-7.5/t) w-o-w. Other markets largely remained firm, as elevated offer levels kept buyers cautious, limiting procurement to need-based only amid weakness in finished steel demand.

- On the export front, DRI offers edged up slightly this week despite subdued demand. Export offers to Nepal rose by $4/t w-o-w to $350/t CPT Raxaul, while offers to Bangladesh increased by $2/t to $361/t CPT Benapole. The rise in offers was supported by higher domestic sponge iron prices, although enquiries remained limited at elevated price levels.

- SAIL Bokaro Steel Plant (BSL) conducted a steel-grade pig iron auction on 8 April, offering 3,500 t, with the entire quantity booked at an average price of INR 38,900/t. Prices increased by INR 550/t compared to the 1 April auction, where 3,500 t were sold at INR 38,350/t. This indicates stronger demand and a modest improvement in market outlook.

- NMDC's Nagarnar Steel Plant auctioned 7,000 t of steel-grade pig iron on 9 April, with the entire quantity booked at an average price of INR 38,200/t. Bids increased by INR 1,250/t from the 30 March auction, when the entire 3,000 t offered was sold at INR 36,950/t. The outcome reflects firm demand conditions and continued upward price momentum.

Finished long steel

- IF-rebar: IF-route rebar trade prices showed mixed trends across major markets this week, primarily influenced by reports of a ceasefire, which created a panic situation in the market. The easing of geopolitical tensions created uncertainty, prompting buyers to adopt a cautious approach and prevent fresh bookings.

- Manufacturers initially attempted to maintain prices at elevated levels; however, buying activity remained limited at higher price points. To sustain sales momentum and liquidate material, mills offered selective discounts during the latter half of the week. At the same time, traders who had procured material at varied price levels looked to release material while preserving margins, resulting in a cautious and slow-moving market.

- Overall trading activity remained moderate, with purchases largely need-based. In the near term, market sentiment is expected to remain range-bound, with prices likely to fluctuate within a narrow band depending on demand recovery and raw material movements.

- On a week-on-week basis, rebar prices varied in the range of INR 100-1,000/t across major regions, as per BigMints assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 53,700-54,300/t exw Jalna and INR 47,200-47,600/t exw Raipur.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 48,800-49,200/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 46,900-47,500/t ex-Raipur.

- BF-rebar: Trade-level BF-rebar prices (distributor to dealer) edged down by INR 100/t ($1/t) w-o-w to INR 60,500/t ($651/t) exy-Mumbai, as per BigMint's assessment on 10 April 2026. Buying activity remained moderate across key regions, while north India witnessed relatively subdued demand, according to sources. Distributors are holding ample inventories, leading to cautious procurement at elevated price levels. Overall, market sentiment remained mixed during the week.

- Rebar project prices were workable in the range of INR 59,000-60,000/t ($635-646/t) on landed basis, as per market sources.

Flat steel

- BigMint's benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices inched down by INR 400/t ($4/t) w-o-w to INR 59,300/t ($638/t) on 10 April against INR 59,700/t ($642/t) in the same period last week.

- CRC (IS513, Gr O, 0.9 mm/CTL) prices stood at INR 67,000/t ($721/t) as assessed on 10 April, a slight decrease of INR 200/t ($2/t) w-o-w against INR 67,200/t ($723/t).

- Trade sentiment for HRC and CRC turned cautious this week amid ceasefire news. Additionally, slow trading activity prompted sellers to soften rates, though demand remains largely unmoved.

- India's bulk imports of HRCs touched 76,450 t as of 6 April, based on vessel line-up data. Around 210,709 t of additional cargoes are expected by mid-April.

India's bulk exports of HRCs touched 14,378 t as of 6 April. Indian HRC export activity remained largely subdued during the week 31 March-7 April 2026, as escalating geopolitical tensions and persistent disruptions across key maritime routes continued to weigh on trade flows. Amid elevated freight-related uncertainty, limited logistical visibility, and ongoing operational challenges, market participants largely adopted a cautious wait-and-watch approach, keeping overall export activity muted.