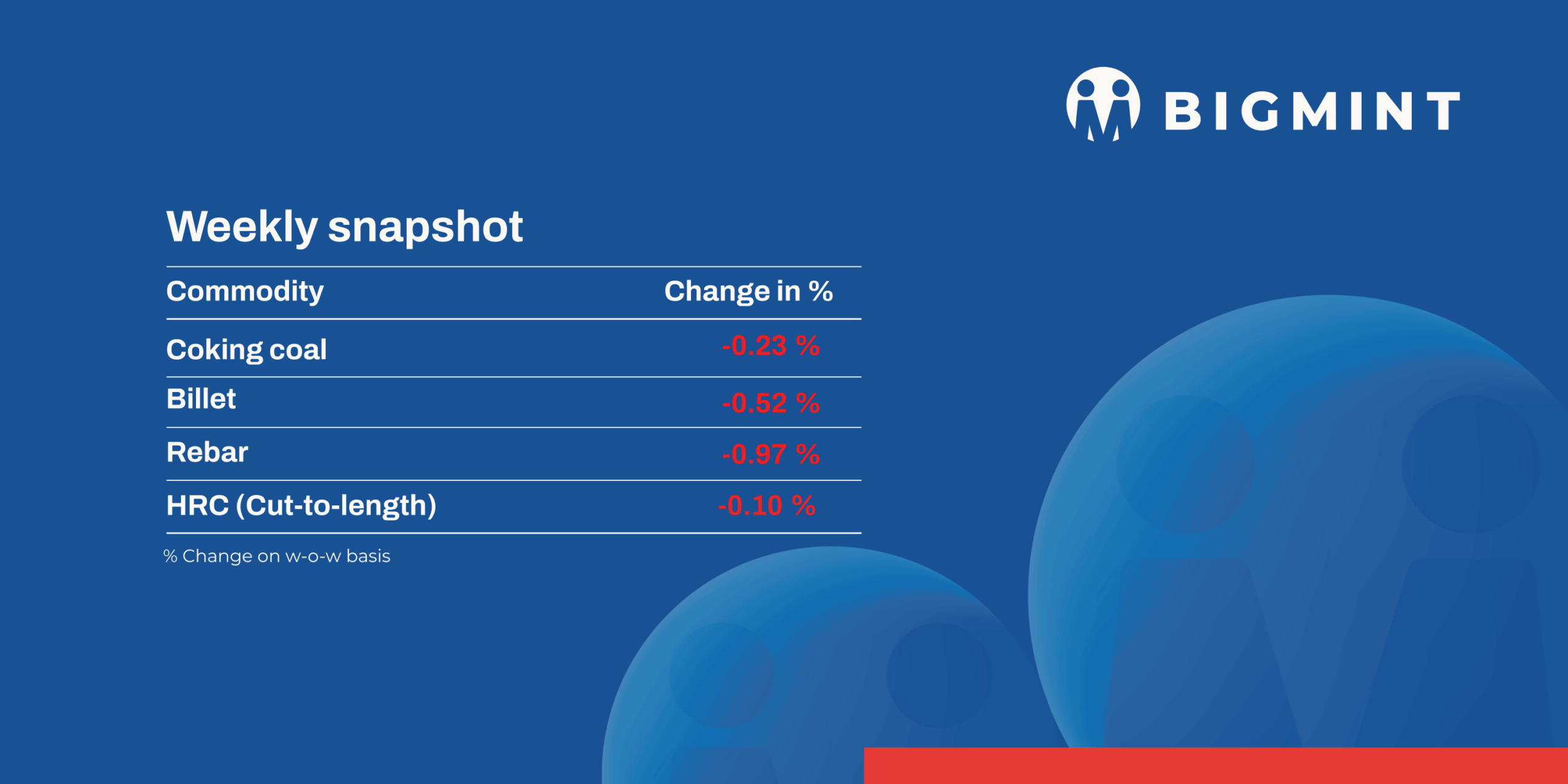

Weekly round-up: Indian steel markets face demand pressure amid monsoon-driven slowdown

...

- Monsoon disruptions and cautious buying continued to weigh on steel demand.

- Raw material trends remained mixed, while project activity supported consumption.

Weak demand and cautious procurement pressured prices across steel and raw material segments.

Infrastructure investments and export activity provided selective support amid broader market

Iron ore and pellet

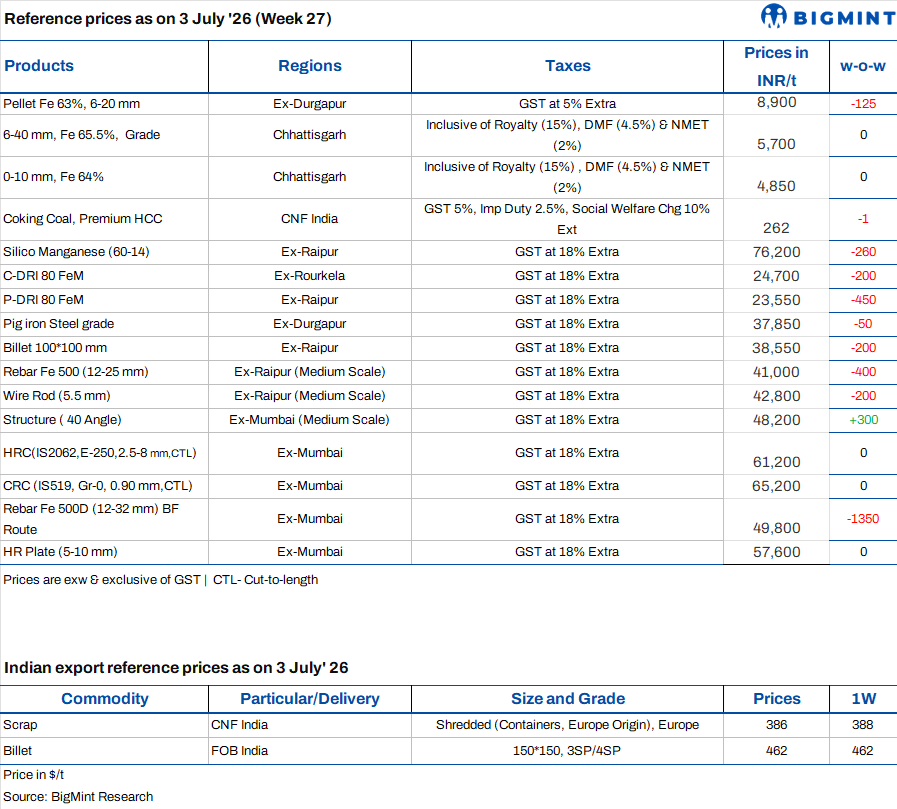

- PELLEX, BigMint's bi-weekly domestic pellet (Fe 63%) index for Raipur, increased by INR 200/t to INR 9,300/t ($97/t) DAP. The uptick followed a similar INR 200/t increase in pellet offers announced by local producers yesterday. However, despite the higher offer levels, spot trading activity remained subdued as buyers adopted a wait-and-watch approach, holding back purchases amid uncertainty over market direction ahead of NMDC's July iron ore price revision.

- BigMint's India pellet (Fe 63%, 3-3.5% Al) export index rose by $1.5/t to $99/t FOB east coast on 3 Jul'26 against 1 Jul'26, supported by active export trading, with around 170,000 t booked during the assessment period. An eastern India-based producer concluded a deal for 115,000 t of pellets (Fe 63/64%, 1.5% AlO and SiO) at $124-125/t CFR India, while another producer sold 55,000 t of pellets (Fe 63%, 1.5% AlO and SiO) at $107-108/t FOB India, reflecting improved export demand and firmer market sentiment.

- During SAIL auctions held from Monday to Thursday, around 135,770 t of iron ore (Fe 55.74-61%) was booked at prices ranging between INR 2,600-4,727/t. The prices were on an ex-mines/FOR loaded into rake basis, inclusive of royalty, DMF, NMET, and additional premium charges.

Coal

- South African thermal coal prices declined further during the week, with ex-Paradip RB2 (5,500 NAR) falling by INR 250/t w-o-w to INR 10,550/t and RB3 (4,800 NAR) by INR 200/t to INR 9,400/t. At Vizag, RB2 eased by INR 200/t to INR 10,400/t, while RB3 declined by INR 200/t to INR 9,300/t. The correction reflected weak steel and sponge iron demand, comfortable domestic coal availability and muted buying interest. Consumers continued purchasing only immediate requirements, while traders struggled to liquidate existing inventories during the monsoon.

- Domestic thermal coal prices remained unchanged during the week, with BigMint's 5,000 GCV index stable at INR 5,500/t and 4,500 GCV at INR 4,050/t. Comfortable Coal India supplies, regular subsidiary auctions and competitive pricing continued to support the domestic market. Buyers preferred domestic coal over imported material as higher import costs and weak steel and sponge iron demand discouraged discretionary purchases. Overall sentiment remained stable, with procurement largely limited to immediate requirements.

- Domestic met coke prices softened during the week, with BF-grade coke in eastern India declining by INR 500/t w-o-w to around INR 36,000/t ex-Jajpur, while western India remained stable at INR 34,000/t ex-Gandhidham. Imported Indonesian BF-grade coke also eased by $1/t w-o-w to around $318/t CFR India. Market sentiment remained cautious as uncertainty over the anti-dumping duty on low-ash imports kept buyers and sellers on the sidelines, while weak steel demand continued to limit spot transactions.

Ferrous Scrap

- India: Imported ferrous scrap market remained subdued throughout the week, with poor import economics and competitive domestic scrap continuing to limit buying, while higher July freight rates further weighed on fresh bookings.

- UK-origin HMS 80:20 was heard at $325-335/t CFR, while UK-origin shredded scrap was offered at $385-390/t CFR. US-origin HMS 80:20 was assessed at $335-340/t CFR, with Australia-origin HMS at $330/t CFR Chennai and shredded at $360/t CFR Chennai. Buyers continued to seek prices $15-20/t below prevailing shredded scrap offers. Market participants expect mills to continue need-based procurement in the near term.

- In the last seven days, India imported around 4,500-5,000 t of ferrous scrap, including 2,500-3,000 t of HMS grades (HMS 80:20 and HMS 60:40) and 2,500-3,000 t of turning & boring scrap. The cargoes were sourced from the UK, Costa Rica, Israel and the US, with deliveries to Mundra, Chennai and Nhava Sheva.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices edged down by INR 475/t ($5/t) w-o-w to INR 75,800-76,300/t ($803-808/t) across key markets. Prices edged down due to weak buying interest and slow trade activity. Steel mills continued need-based procurement, while sufficient material availability forced some producers to adjust offers to attract bookings.

- Meanwhile, HC 65-16 silico manganese export prices edged up by $1/t to $924/t FOB Vizag/Haldia.

- Additionally, State-owned MOIL Limited has revised its manganese ore prices, effective 1 July 2026. Prices of ferro-grade ores containing more than 44% Mn have been reduced by 5%, while ferro grades with Mn content below 44% have also witnessed a 5% price cut. In the SMGR category, prices of 30% Mn, 25% Mn, fines, and chemical-grade ores have been lowered in the range of 5-10%.

- Ferro Manganese:Indian ferro manganese (70%) prices inched down w-o-w by INR 200/t ($2/t) to INR 79,000/t ($837/t) in Raipur and by INR 500/t ($5/t) to INR 78,800/t ($834/t) in Durgapur.Prices edged lower as limited buying interest and need-based procurement from steel mills pressured offers, while sufficient availability kept market sentiment subdued.

- However, export prices for the 75% grade remained flat w-o-w to $930/t FOB Vizag/Haldia.

- Ferro Silicon:India ferro silicon (Si 70%) prices dropped by INR 2,000/t ($21/t) w-o-w to INR 89,500/t ($948/t) ex-works Guwahati, while Bhutan prices also fell by INR 2,300/t ($24/t) to INR 89,700/t ($950/t). Prices continued to decline last week as weak demand and competitive offers weighed on market sentiment. Buyers remained cautious amid expectations of further corrections, while sellers lowered offers to sustain sales and maintain plant operations.

Semi finished

- India's semi-finished steel market remained under pressure during the week, as billet prices declined across key producing regions amid weak downstream demand and growing competition from neighbouring markets. As per BigMint's assessment, domestic billet prices fell by INR 100-500/t ($1-5/t) w-o-w across key production regions, with producers lowering spot offers to align with buyers' expectations and attract buying activity.

- Buying activity stayed need-based throughout the week, while competitively priced material from nearby markets intensified pressure on local producers. The softer pricing environment limited sellers' bargaining power, resulting in lower spot prices across most the major markets. In contrast, southern markets outperformed the broader trend, with billet prices rising by INR 300-800/t ($3-8/t) w-o-w on improved regional buying activity and relatively balanced supply-demand conditions.

- The sponge iron market also witnessed a modest correction this week. Prices across major producing regions declined by INR 100-550/t ($1-5.7/t) w-o-w as producers adopted more competitive pricing strategies to attract buyers. Unlike the billet market, however, the lower offers helped stimulate procurement, resulting in an improvement in weekly booking volumes as mills and traders replenished inventories at more attractive price levels.

- On the export front, Indian direct reduced iron (DRI) offers weakens marginally amid muted buying interest from neighbouring countries. Export offers to Nepal declined by $1/t w-o-w to $299/t CPT Raxaul, while offers to Bangladesh slipped by $2/t to $303/t CPT Benapole.

NMDC's Nagarnar Steel Plant auctioned 6,000 t of steel-grade pig iron on 2 July, with the entire quantity sold at an average price of INR 36,100/t ex-works. The auction price increased by INR 300/t from the previous sale held on 25 June, when 6,100 t out of the 10,000-t offered was booked at INR 35,800/t ex-works. The higher realised price alongside complete allocation indicates stronger buying interest and improving confidence in the pig iron market despite continued weakness across the broader semi-finished steel segment.

Finished long steel

- IF-rebar:IF-route rebar prices declined across most major markets this week, primarily tracking the weakness in key raw materials, particularly billet and sponge iron. Trading activity remained limited as buyers continued to procure material only to meet immediate requirements amid cautious market sentiment and slow construction demand. To support sales, mills offered discounts amid subdued buying interest. Mill inventory levels remained comfortable at around 10-15 days, while order booking visibility was limited to approximately 3-5 days, reflecting the absence of fresh demand. IF-route rebar prices are expected to remain range-bound in the near term as the onset of the monsoon is likely to weigh on construction activity and buying sentiment. Procurement is expected to remain need-based unless demand improves.

- On a week-on-week basis, rebar prices declined by INR 100900/t across key regions, except in the Ahmedabad, Mandi Gobindgarh and Chennai and Raigarh where the prices rose by INR 100/t, 100/t and 300/t respectively, according to BigMint's assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (1025 mm size) were assessed at INR 40,80041,200/t exw Raipur and INR 44,60045,200/t exw Jalna.

- BF-rebar:Trade-level BF-route rebar prices declined to INR 49,800/t exy-Mumbai amid elevated distributor inventories and cautious procurement activity.

- Demand remained average across major regions, while northern India continued to witness weaker buying interest.

- Project and infrastructure demand provided partial support, although buying activity in the projects segment remained cautious.

Flat steel

- BigMint's bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) in Mumbai remained stable w-o-w at INR 58,200/t ($615/t) as of 30 June.

Likewise, the benchmark assessment for CRC (IS513, Grade O, 0.9 mm/CTL) was unchanged at INR 65,200/t ($689/t) as of 30 June.

- India's trade-level HRC market softened marginally during the week as subdued buying activity and a wait-and-watch approach continued to weigh on the market amid expectations of potential price corrections and upcoming mill price announcements.

- A significant development for the domestic flat steel market comes with The Directorate General of Trade Remedies (DGTR) under India's Ministry of Commerce has opened an anti-dumping (AD) investigation into hot-rolled flat steel products originating in or exported from China, Japan and Russia.

- India's bulk imports of HRCs touched 209,731 t as on 26 June. Around 199,898 t of additional cargoes are expected by mid-July.

- India's bulk exports of HRCs touched 176,704 t as of 26 June. Around 48,550 t of additional cargoes are expected to be shipped.

- Indian HRC export activity remained subdued during the assessment week ended 30 June 2026, as weak overseas demand across key destinations continued to suppress buying interest with market participants largely adopting a wait-and-watch approach.

- Moreover, the European Union has formally adopted a new steel trade framework,Under the revised regime, the EU has allocated 18.35 mnt of annual TRQs across steel products, with imports beyond the quota now subject to a higher 50% out-of-quota duty, compared with the previous 25%.

- BigMint's bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) in Mumbai remained stable w-o-w at INR 58,200/t ($615/t) as of 30 June.