India IF-route rebar prices decline on slow demand, softer raw materials

...

- Softer raw material prices weigh on IF-route rebar

- Monsoon-led slowdown, need-based buying to keep prices range-bound

India's Induction furnace route rebar prices declined by INR 100-2,200/t across most regions during the month, reflecting cost pressure and mills inability to sustain higher selling prices amid moderate to limited demand. The decline was driven by slow demand in the semi-finished steel segment, particularly billet and sponge iron prices, which exerted downward pressure on rebar offers.

Trading activity remained limited, with buyers continuing to procure material only to meet immediate requirements. Mills initially attempted to maintain prevailing price levels during the first half of the month. However, as demand remained moderate, they revised offers downward in the latter half, resulting in improved buying enquiries at lower price levels. Consequently, mill inventory levels declined to around 12 days from nearly 15 days earlier in the month, while order bookings improved to approximately 3-5 days. Meanwhile, the BF-IF route rebar price gap narrowed to around INR 6,900/t in June from INR 10,100/t in May, reflecting the sharper correction in IF-route rebar prices.

As per Joint Plant Committee (JPC) data, India's rebar production through the IF and BF routes reached 1.27 million tonnes (mnt) during the first two months of FY'27, registering a 2% year-on-year increase from 1.24 mnt in the corresponding period of FY'26.

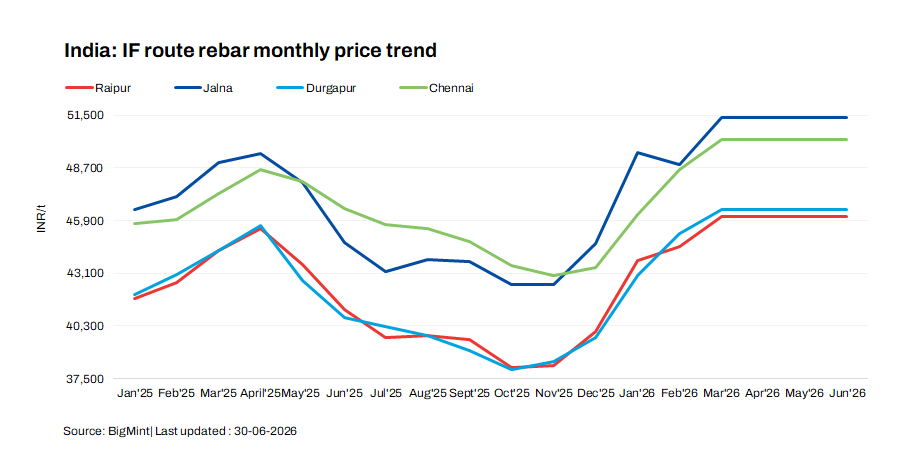

Region-wise price movements

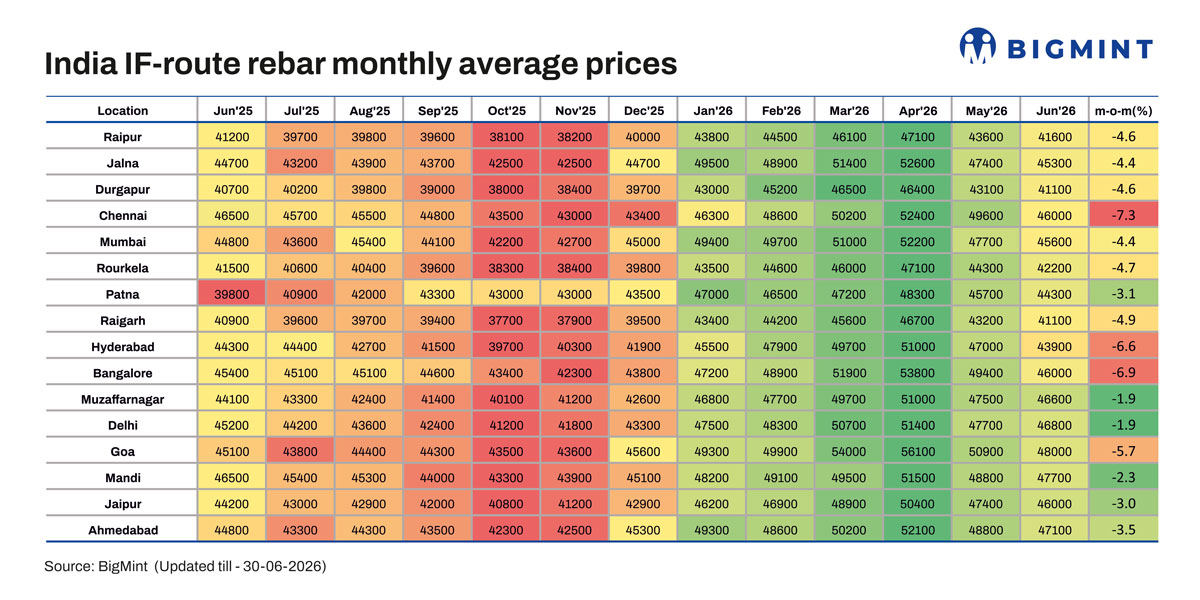

The northern region's rebar market remained under pressure in the range of INR 700-1200/t during the month, with slow construction activity and the onset of the monsoon weighing on demand. Buyers continued to procure material only to meet immediate requirements, keeping trading activity limited. Although Mandi Gobindgarh witnessed marginal price support due to scrap shortages, labour constraints, and intermittent power outages, the overall market sentiment remained weak. Mill inventories were maintained at around 7-10 days, while order bookings remained limited at 2-4 days. Additionally, narrowing billet-to-rebar conversion margins continued to pressure mill profitability, prompting manufacturers to adopt a cautious approach toward production and pricing. Market participants also indicated the possibility in near term of increased material movement from eastern India into the northern region. With Durgapur rebar prices hovering around INR 41,100/t and Mandi Gobindgarh prices at approximately INR 47,700/t, the price differential of nearly INR 6,600/t could make inter-regional procurement commercially viable, subject to freight economics and order volumes.

In the western region, rebar prices saw a sharp m-o-m decline of INR 400-2,000/t, with Ahmedabad down by INR 1,900/t, Mumbai by INR 1,200/t, and Jalna by INR 400/t. Slower construction activity and limited to moderate demand kept market sentiment cautious. Mills reduced offers and offered discounts to boost sales. Buyers procured sufficient material at lower rates. Lifting and dispatching of the previously sold material was smooth throughout the month. While spot sales operated at ~50-70% of production. Inventory levels remained maintained at 12-15 days.

In central India, rebar prices in Raigarh and Raipur eased by INR 400/t and INR 100/t, respectively, during the month. Buying activity remained moderate, supported by local demand and orders from neighbouring markets, particularly Madhya Pradesh and Maharashtra. The increase in industrial electricity tariffs in Chhattisgarh, effective 1 July 2026, strengthened mills' pricing sentiment by raising production costs. However, subdued construction demand capped price recovery. Mills maintained order bookings at around 5-6 days, while inventory levels improved to 10-12 days from 12-15 days in the previous month.

In Eastern region prices declined by INR 700-1200/t m-o-m, with sharpest fall of INR 1200/t seen in the Rourkela. Weaker demand and slower buying from the North-East kept market sentiment subdued, while steady demand from Uttar Pradesh, Bihar, and Jharkhand prevented a sharper correction. Mill inventories remained at moderate levels amid a balanced supply-demand scenario. However, margins continued to remain under pressure due to intense price competition, leaving limited scope for profitability despite stable operating conditions.

In Southern region, particularly in Chennai and Hyderabad, IF route rebar prices declined by around 6-7% month-on-month during July 2026. The correction was primarily driven by weak demand from the construction and infrastructure sectors, along with elevated finished steel inventories that prompted manufacturers to lower prices to support sales. Market sentiment remained weak as shrinking conversion margins pressured mill profitability. Amid subdued demand and limited pricing power, manufacturers adopted a cautious production approach while closely monitoring market conditions.

Raw material price trends

The drop in finished steel prices was mainly driven by lower prices of key raw materials -- steel billets and sponge iron -- used in IF-route rebar production.

Prices of key raw materials, particularly billet and sponge iron, remained under pressure during the month due to slow demand from the finished steel segment. Buying activity stayed cautious, with billet manufacturers and rebar producers limiting procurement to immediate requirements amid cautious market sentiment. Although the billet market witnessed some recovery towards the latter half of the month in select regions, overall demand remained limited. Elevated inventories and slow material offtake continued to weigh on the market, keeping raw material prices under pressure.

Considering Raipur as the benchmark, billet prices recorded a decline of INR 250/t m-o-m to INR 38,950/t ex-works on 30 June while sponge iron (PDRI FeM 80% 1) also weakened, falling by INR 1000/t m-o-m to INR 24,050/t ex-works.

BF rebar sentiment

Indian primary steelmakers have reduced rebar list prices for early June 2026 by up to INR 1,000-6,000/t, market sources informed BigMint. Following the revisions, list prices stood at INR 52,000-54,000/t on a landed basis.

Trade-level BF-route rebar prices (distributor-to-dealer) also declined by up to INR 5,800/t m-o-m to around INR 50,000/t exy-Mumbai, according to BigMint's assessment on 30 June 2026. Buying activity in the trade channel remained subdued throughout June, with buyers largely staying on the sidelines and restricting purchases to immediate requirements. Market participants reported comfortable inventory levels amid slower material offtake in recent weeks.

In the projects segment, rebar prices stayed in the INR 48,500-49,500/t range (FOR). Demand remained subdued due to weak inquiries, labour shortages, and construction disruptions, delaying project execution and procurement. Buyers stayed cautious amid price volatility.

Outlook

IF-route rebar prices are expected to remain range-bound in the near term as monsoon-related disruptions and slow construction activity continue to weigh on demand. Buying is likely to remain need-based, while mills may continue to offer competitive prices to support order bookings amid comfortable inventory levels.