Weekly round-up: Coal market remained subdued amid ample domestic supply and cautious buying sentiment

...

- Domestic coal dominated procurement decisions

- Imported coal enquiries remained weak

The Indian coal market remained subdued this week as abundant domestic coal availability continued limiting imported coal demand. Buyers largely adopted a wait-and-watch approach, with procurement restricted to immediate requirements amid weak steel sector fundamentals and monsoon-related slowdown. Frequent Coal India auctions ensured sufficient supply, while improved geopolitical sentiment softened freight expectations without translating into higher enquiries. Market participants remained cautious, awaiting stronger downstream demand before returning to the imported coal market.

Indonesian coal prices ease

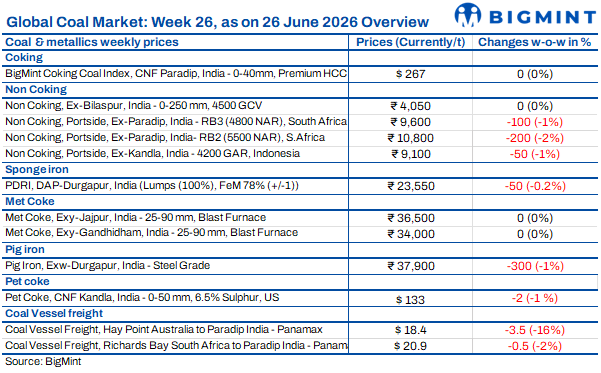

Indian portside prices for Indonesian thermal coal softened during the week ended 26 June amid subdued buying interest and ample domestic coal availability. BigMint assessed 5,000 GAR coal stable at INR 11,000/t at Kandla and INR 10,900/t at Vizag, while 4,200 GAR prices declined by INR 50/t to INR 9,100/t and INR 9,000/t, respectively. Navlakhi 3,400 GAR fell by INR 100/t to INR 7,000/t. Freight from East Kalimantan to Navlakhi dropped by $1.2/t to $20.8/t. Despite tighter Indonesian supply due to higher domestic commitments to PLN, comfortable Indian inventories and cautious buying continued to keep import demand weak.

South African coal weakens

South African thermal coal prices declined across Indian ports during the week as weak demand and sufficient domestic coal availability kept buyers away. As per BigMint's assessment on 26 June, ex-Paradip RB2 (5,500 NAR) fell by INR 200/t w-o-w to INR 10,800/t, while RB3 (4,800 NAR) declined by INR 100/t to INR 9,600/t. Ex-Vizag RB2 and RB3 both dropped by INR 200/t to INR 10,600/t and INR 9,500/t, respectively. India's imported coal inventories rose 11.4% w-o-w to 15.07 mnt. FOB RBCT 5,500 NAR offers were heard at $89.5-92/t against bids of $85-86/t. However, domestic sponge PDRI prices remained stable at INR 23,600/t despite improved enquiries.

Domestic coal prices stable

Domestic 5,000 GCV non-coking coal remained stable w-o-w at INR 5,500/t, while 4,500 GCV coal was unchanged at INR 4,050/t, as per BigMint's assessment. Frequent Coal India subsidiary auctions ensured ample coal availability during June, although only 20-50% of the offered volumes were allocated. While select grades attracted healthy premiums, others cleared close to their base prices, reflecting comfortable domestic supply. Buyers continued meeting requirements through domestic coal, limiting demand for imported cargoes and keeping procurement largely need-based.

US NAPP demand weakens

The US NAPP coal market remained well supplied, but retail demand weakened. Portside prices eased to around INR 13,300-13,600/t, while weekly dispatches declined to 93,000 t from 129,000 t in the previous week. Inventories remained comfortable at around 313,000 t across Kandla and Tuna ports as buyers limited procurement to immediate requirements amid softer petcoke prices and the seasonal slowdown in brick kiln activity.

Met coke prices edge higher

India's imported met coke market recovered marginally during the week, supported by firm global prices and tight raw material availability. BigMint's assessment for Indonesian BF-grade coke (65/63 CSR) increased by $1/t w-o-w to $319/t CFR India, while FOB offers were heard at $294-295/t. Spot trading remained limited as buyers awaited clarity on the government's anti-dumping duty decision. In China, mills accepted the ninth round of coke price hikes, increasing prices by RMB 50-55/t ($7-8/t), amid tightening supply conditions. Domestically, BF-grade coke remained stable at INR 36,500/t ex-Jajpur and INR 34,000/t ex-Gandhidham, while SAIL Bokaro's pig iron auction prices increased by INR 800/t to INR 36,400/t, indicating improved market sentiment.

Petcoke prices correct sharply

Global fuel-grade petcoke prices softened during June, improving its competitiveness for Indian cement producers. FOB US Gulf Coast 6.5% sulphur prices declined by $6/t to $75.5/t, while CFR west coast India prices eased to around $134-135/t. The correction encouraged cement manufacturers to shift back towards petcoke after relying more on imported coal earlier this year. Despite the monsoon slowing construction activity, India's cement production increased 8.3% y-o-y to around 83 mnt during April-May.

Coal freight rates soften

India's dry bulk coal freight market weakened during the week ended 26 June as subdued Pacific cargo demand and ample prompt vessel availability pressured freight rates. BigMint assessed Hay Point-Paradip Panamax freight at $18.4/t, down $3.5/t w-o-w, while RBCT-Paradip declined by $0.5/t to $20.9/t amid limited fresh enquiries. East Kalimantan-Navlakhi Supramax freight fell by $1.2/t to $20.8/t as slower Indonesian coal movement and wider bid-offer gaps weighed on sentiment. Meanwhile, the Baltic Dry Index eased by 62 points to 2,591, while Brent crude declined to $72.78/bbl, reflecting softer overall freight and energy market sentiment.