China weekly: Steel prices soften amid sluggish consumption, elevated supplies

...

- Supply constraints drive successive coke price hikes

- Weak construction demand widens rebar market imbalance

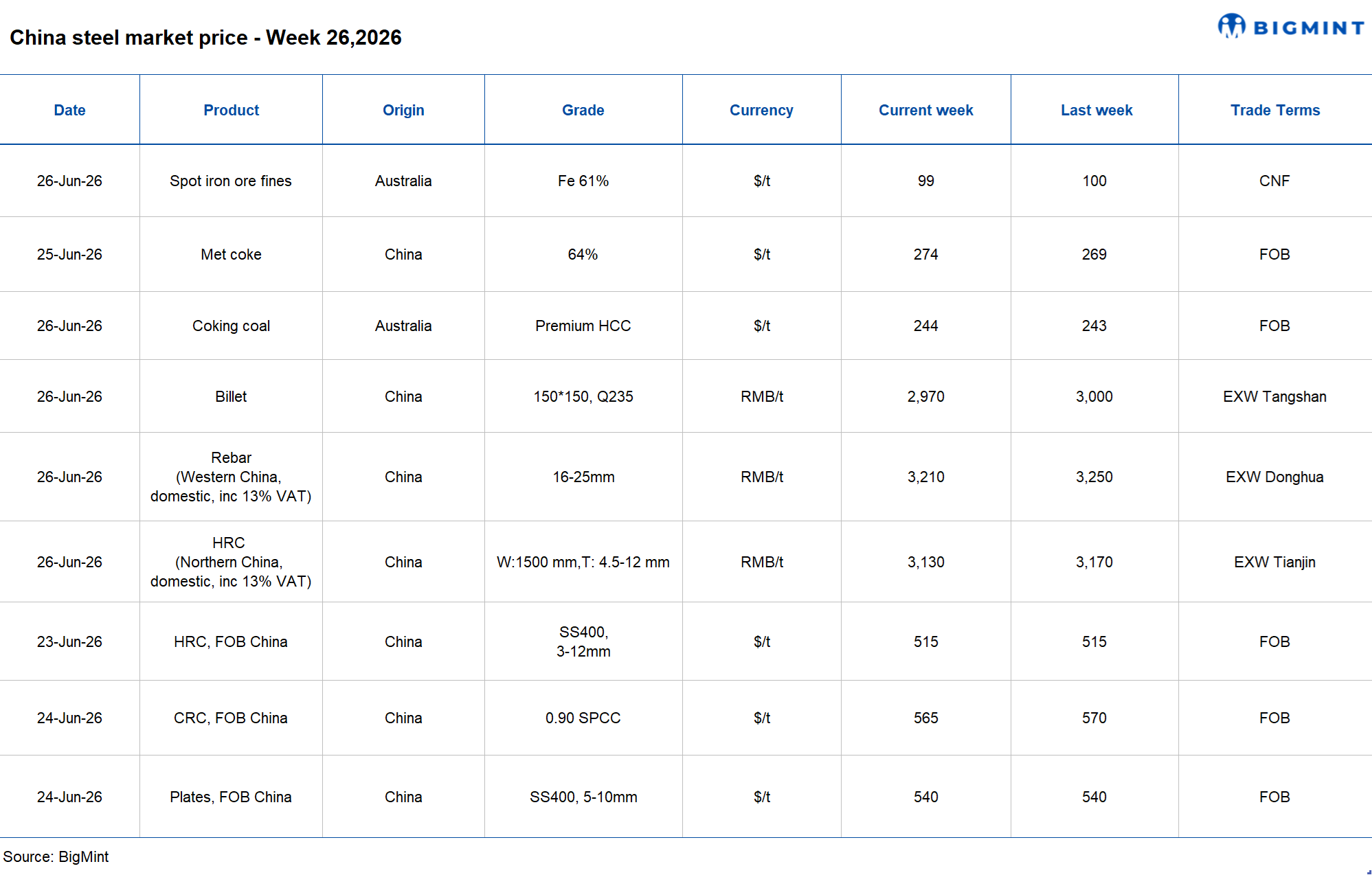

China's steel prices show downward trend in the week ended 26 June 2026. Chinese HRC and rebar prices dropped with the market facing a seasonal slowdown. Furthermore, on the raw materials front, prices of iron ore and billet prices drop, though met coke prices increased w-o-w.

Meanwhile, China Iron and Steel Association (CISA) reported that total steel inventories at key CISA-affiliated industries stood at around 17.9 million tonnes (mnt) during mid-June (11-20 June 2026), marking an increase of 1.03 mnt or 6.1% from 16.87 mnt in early-June.

Furthermore, inventory levels rose by 1.69 mnt or 10.4% y-o-y from 16.21 mnt recorded in the same period last year.

However, inventories dropped by 0.87 mnt or 4.6% m-o-m from 18.77 mnt in mid-May.

Steel inventories increased as demand remained weak and end-user buying was insufficient to absorb available supply. This slowed the pace of inventory clearance, leading to higher stock levels.

Raw material prices

Iron ore spot prices drop w-o-w: Iron ore fines benchmark prices for Fe 61% decline w-o-w by $1/t w-o-w to $99/dmt CFR China on 26 Jun'26.

The correction was driven by deteriorating steel demand and bearish expectations across China's steel sector. Apparent steel consumption, particularly for rebar, softened compared with the previous week, underscoring the ongoing supply-demand imbalance. Weak steel mill margins prompted mills to increase the use of lower-grade fines in blending strategies, while some speculative trading activity among traders persisted.

a) Spot pellet premium stable: Spot pellet premium for Fe 65% grade pellet remained largely stable at $19.60/t CFR China on 24 June.

b) Spot lump premium edges down: Spot lump premium lowered w-o-w by $0.011/t to $0.1850/t CFR China on 26 June.

China's coke market gains momentum: China's coking coal and coke markets remained firm w-o-w, supported by constrained supply and steady steel mill demand. Slow mine restarts, ongoing safety inspections, and limited supply recovery supported coking coal prices, while high raw material costs led some coke producers to reduce output.

Strong blast furnace operations and higher pig iron production kept coke demand stable, resulting in low inventories. Tight supply-demand conditions supported the eighth round of coke price hikes by RMB 55/t (~$7/t), with a ninth round initiated, sustaining a positive near-term outlook.

Australian Premium Hard Coking Coal (PHCC) prices edged up by $1/t w-o-w to $244/t FOB Australia as easing geopolitical concerns reduced supply risk premiums. BigMint's coking coal index remained stable w-o-w at $267/t amid limited spot market activity.

Domestic billet extends weekly decline: Chinese billet prices extended their decline during the week ended 26 June, with buyers largely staying on the sidelines as seasonal weakness in construction activity continued to weigh on steel consumption. BigMint assessed domestic billet at RMB 2,970/t ($439/t), down from RMB 3,010/t ($445/t) a week earlier.

Spot trading remained sluggish throughout the week, with daily transaction volumes hovering around 80,000 t, while domestic finished steel prices slipped by RMB 5-10/t across most regions. Rising social inventories further reflected slower offtake, prompting mills and traders to adopt a cautious stance.

On the cost side, easing raw material prices reduced support for billet. However, relatively resilient iron ore demand and tight coke availability prevented a sharper correction. Sentiment was also dampened by a stronger US dollar and broader weakness across global commodity markets, which discouraged aggressive buying.

The softer domestic market was mirrored in exports. Chinese billet export offers eased to around $460-464/t FOB, compared with $468-470/t FOB a week earlier, as overseas buyers remained cautious and fresh enquiries were limited.

Weekly steel price trend

Domestic HRC prices decrease w-o-w: Chinese HRC prices decreased by RMB 40/t ($6/t) w-o-w to around RMB 3,130/t ($460/t) on 26 June from RMB 3,170/t ($466/t) from the previous week. Moreover, SHFE HRC futures (October 2026 contract) down by RMB 43/t ($6/t) w-o-w to RMB 3,306/t ($485/t) from RMB 3,349/t ($492/t) a week earlier. However, Chinese HRC export offers remain stable w-o-w at around $515/t FOB Rizhao.

Subdued downstream demand keeps market participants cautious, prompting some sellers to lower offer prices to secure transactions. However, higher coke prices continue to provide strong cost support, limiting the scope for further price declines.

Weak overseas demand continued to weigh on export market sentiment, keeping buying activity subdued.

Rebar prices decrease w-o-w: Rebar prices in China were down by RMB 40/t ($6/t) w-o-w to around RMB 3,210/t ($472/t) as on 26 June, compared with RMB 3,250/t ($478/t) in the previous week. Furthermore, SHFE rebar futures (October 2026 contract) also dropped by RMB 43/t ($6/t) w-o-w to RMB 3,308/t ($486/t) as on 26 June from RMB 3,131/t ($460/t) a week earlier.

Rebar prices in the Chinese market declined as steel mills gradually resumed production after blast furnace maintenance, increasing overall supply. With demand remaining weak during the off-season, the widening supply-demand imbalance intensified market pressure, weighing on rebar prices.

China's Shagang Steel has kept its long steel prices unchanged for late-June 2026 sales. The producer maintained prices for rebars (16-25 mm) at RMB 3,400/t ($500/t), coiled rebars (8-10 mm) at RMB 3,530/t ($519/t), and wire rods (6-10 mm) at RMB 3,440/t ($506/t).

The price rollover comes amid a challenging domestic market environment. Demand remains under pressure as widespread rainfall across several regions continues to disrupt construction activity, reducing steel consumption.

Outlook

Upcoming macroeconomic policy announcements and steel mill production trends will be closely watched. With seasonal demand remaining weak and supply relatively ample, the construction steel market is likely to fluctuate within a weaker range next week. Meanwhile, traders are expected to continue offering discounts to accelerate inventory clearance amid rising stock levels, keeping pressure on the HRC market. As a result, HRC prices are expected to extend their downward movement in the coming week.