US tariffs on copper imports could redirect global trade towards Asia

...

- US expected to announce refined copper tariff decision by end-June amid record import dependence

- Structural mismatch between refining capacity and copper demand has already begun reshaping global copper trade

- India could emerge as a key beneficiary as surplus cathodes are redirected towards Asia

The United States is expected to announce the outcome of its Section 232 investigation into refined copper imports by the end of June, with the proposed tariffs likely to reshape global copper trade while exposing a longstanding mismatch between domestic refining capacity and rapidly growing demand.

While the policy is intended to strengthen domestic critical mineral supply chains and reduce dependence on imported refined metal, it also exposes a longstanding structural weakness within the US copper supply chain, where refining capacity has failed to keep pace with rapidly growing demand.

Despite possessing abundant copper resources and generating significant volumes of recyclable material, the country continues to rely heavily on imported cathodes because domestic smelting and refining capacity has failed to keep pace with rapidly rising demand.

Markets have already begun reacting to the anticipated policy. Record refined copper imports, rising inventories within the United States and tightening availability elsewhere suggest traders have been diverting material into the American market ahead of any formal announcement. Rather than triggering an entirely new trade cycle, the proposed tariffs are therefore more likely to accelerate a redistribution of global copper that is already underway.

Why the US still depends on imported copper

The proposed tariffs come against the backdrop of a widening imbalance in the US copper market. During 2025, the country produced around 1 million tonnes (mnt) of copper ore and approximately 890,000 tonnes of refined copper, while apparent consumption reached roughly 1.6 mnt. The shortfall has left manufacturers dependent on imported cathodes to meet demand from the construction, power, automotive, electronics and renewable energy sectors.

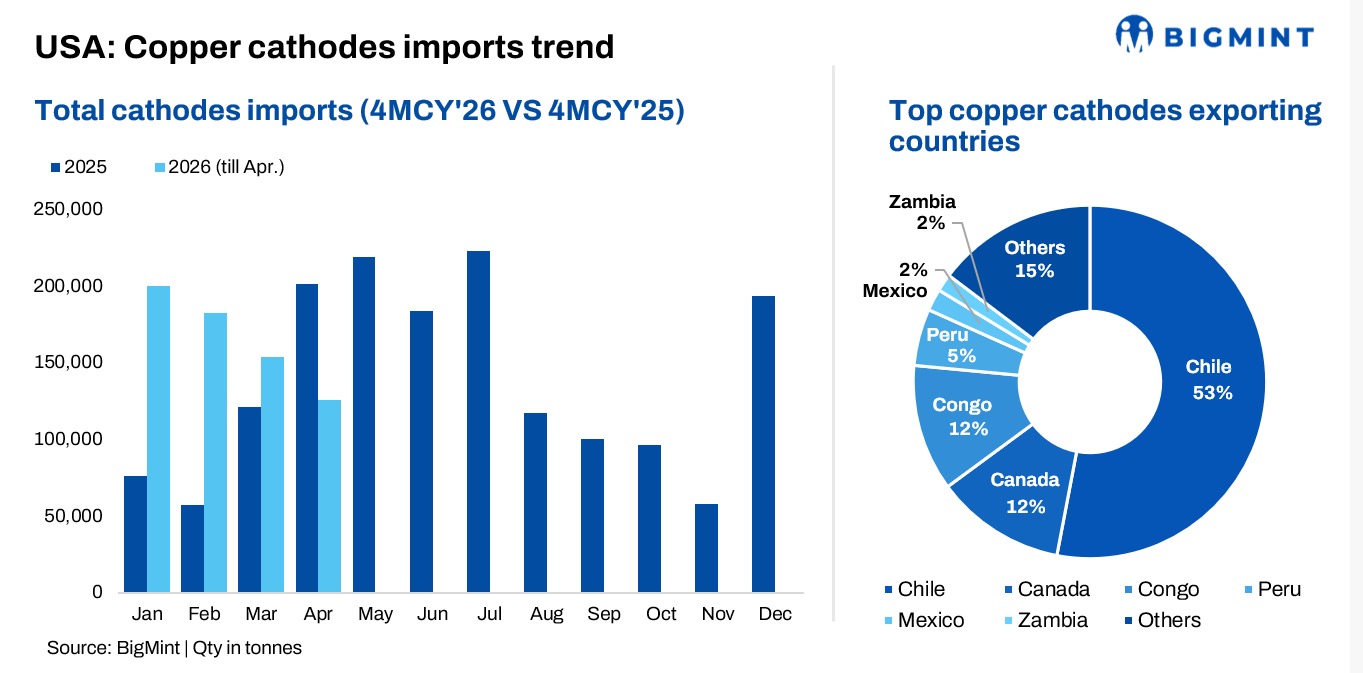

Refined copper imports surged to a record 1.65 mnt in 2025, up from 0.93 mnt in 2024 and well above the average of about 0.82 mnt during 2021-24. Imports remained elevated during January-April 2026 at 0.66 mnt as buyers accelerated procurement ahead of the expected tariff decision. Chile supplied more than half of total imports, while shipments from Canada, the Democratic Republic of Congo, Peru and several other producers also increased.

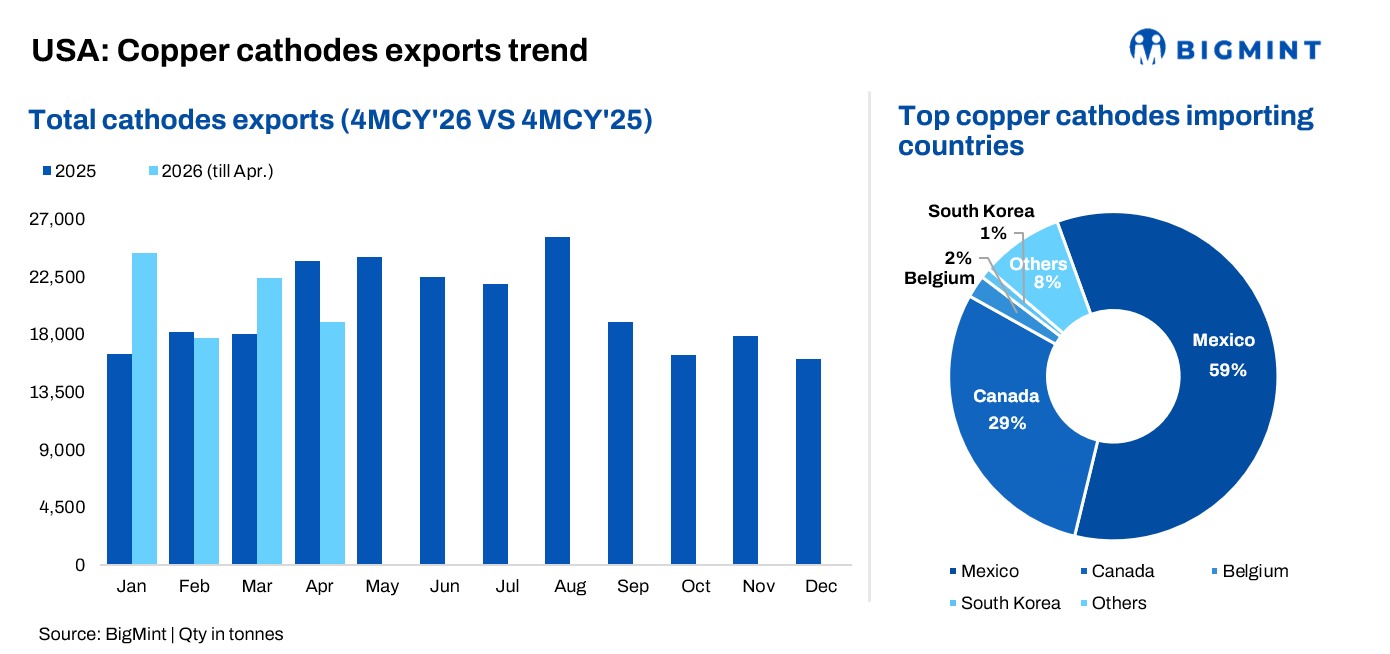

Trade flows highlight that the US challenge lies in processing rather than resource availability.Despite relying heavily on imported refined copper, the United States continues to export large volumes of copper-bearing materials. Combined exports of copper scrap and concentrates reached 1.47 mnt during 2025, almost matching refined copper imports. During January-April 2026, total copper exports increased 8.3% year on year to 623,865 tonnes, led by a 19.5% rise in scrap exports and a 57.3% increase in anode shipments.

The data point to a structural processing bottleneck rather than a shortage of copper. The US possesses abundant raw material and generates significant scrap volumes but lacks sufficient smelting and refining capacity to convert those resources into refined cathodes. As a result, copper-bearing materials continue to leave the country while manufacturers import refined metal to satisfy domestic demand. Tariffs may discourage imports, but they cannot eliminate this dependence until new refining capacity becomes operational, a process likely to take several years.

Energy transition and AI are reshaping copper demand

The urgency surrounding US copper policy reflects profound changes in global copper demand. Electrification, renewable energy, electric vehicles, battery manufacturing and expanding power transmission networks continue to increase copper consumption, while artificial intelligence has emerged as one of the fastest-growing new sources of demand. Data centres alone consumed more than 200,000 tonnes of copper during 2025, compared with less than 30,000 tonnes only four years earlier.

Data centres alone consumed more than 200,000 tonnes of copper during 2025, compared with less than 30,000 tonnes only four years earlier. The rapid expansion reflects the copper-intensive nature of AI infrastructure, where high-capacity power cables, transformers, switchgear and cooling systems are essential for supporting increasingly energy-intensive computing facilities. Copper is therefore no longer simply an industrial metal; it is becoming a strategic resource underpinning the global energy transition and digital economy.

Markets have already moved ahead of the tariff

Although Washington has yet to announce its final decision, copper markets have already begun pricing in the prospect of import tariffs. The expectation of higher duties created a significant premium for copper delivered into the United States, encouraging traders to divert metal towards the American market well before any policy takes effect. As a result, the market has effectively front-loaded imports, with the US accumulating large inventories while material has been drawn away from other consuming regions.

Outside the United States, tightening LME inventories suggest copper availability has become increasingly constrained. LME three-month copper prices have remained above $13,000 per tonne through June despite heightened market uncertainty, underscoring that global demand continues to outpace readily available supply. At the same time, LME inventories have declined steadily from around 367,000 tonnes in mid-June to about 342,000 tonnes by 24 June, suggesting that physical copper availability outside North America has tightened as traders redirected material towards the more profitable US market.

The divergence highlights an important feature of the current market. The tariff itself has yet to be implemented, yet it has already begun influencing physical trade flows. Rather than marking the start of a new market cycle, the policy is likely to reinforce an adjustment that has been unfolding for several months as suppliers, traders and consumers reposition inventories in anticipation of higher import costs.

Global copper trade flows could be redrawn

Once tariffs come into force, those trade patterns are likely to shift again. Exporters that have traditionally relied on the United States will need to identify alternative markets if American imports become less competitive under higher duties.

Chile, Canada, the Democratic Republic of Congo and Peru supplied more than four-fifths of US refined copper imports during 2025. Even a partial reduction in US purchases would release substantial cathode volumes back into international markets, increasing availability across Asia and Europe.

Asia is expected to absorb a significant share of the displaced material. Demand across China, India and Southeast Asia continues to expand, supported by investments in renewable energy, power transmission, electric vehicles, electronics manufacturing and industrial infrastructure. Greater cathode availability would improve procurement flexibility for buyers while increasing competition among overseas suppliers, potentially easing regional physical premiums even if benchmark copper prices remain supported by robust global consumption.

Europe could also benefit from improved availability as electrification projects and grid investment continue to gather pace. The result is unlikely to be a collapse in copper prices, but rather a redistribution of physical supply that eases tightness outside the United States.

India could emerge as one of the principal beneficiaries

India appears well positioned to benefit from this potential realignment. Domestic refined copper production stands at around 0.70 mnt, while annual consumption has reached approximately 1.8 mnt, leaving the country dependent on imports of about 0.24 mntof refined cathodes.

That import requirement is becoming increasingly important as copper demand accelerates across the economy. Expansion of renewable energy capacity, transmission networks, electric vehicle manufacturing, consumer electronics and conventional infrastructure is steadily increasing the country's need for refined copper, while rapid industrialisation continues to support downstream fabrication.

India's import requirement is therefore set to increase alongside its industrial ambitions. Continued investment in transmission infrastructure, renewable energy, electric mobility and electronics manufacturing will require secure access to refined copper, making procurement flexibility increasingly important for the country's downstream value chain.

If suppliers displaced from the US market redirect more cathodes towards Asia, Indian consumers could gain access to a broader supplier base and greater physical availability. Increased competition among exporters would strengthen procurement flexibility for wire rod producers, cable manufacturers and electrical equipment companies while moderating regional import premiums.

For India, the principal benefit is likely to be improved access to imported cathodes and softer regional premiums rather than materially lower benchmark copper prices, as structural demand continues to support the global market.

Outlook

The effectiveness of the proposed tariffs will ultimately depend on whether they stimulate meaningful investment in domestic smelting and refining capacity.They expose a structural imbalance within the American copper industry, where refining capacity has failed to keep pace with rapidly growing demand from electrification, renewable energy, advanced manufacturing and increasingly AI-driven infrastructure.

Whether the policy ultimately succeeds will depend less on the tariff itself than on its ability to stimulate investment in domestic smelting and refining capacity. Until that happens, the United States is likely to remain dependent on imported refined copper even as it continues exporting significant volumes of copper-bearing raw materials.

For global markets, the immediate impact is likely to be a redistribution rather than a reduction in copper trade. Material that has increasingly flowed into the United States ahead of the tariff announcement could gradually return to Asia and Europe once new duties take effect, improving physical availability across key consuming regions. Among the likely beneficiaries, India stands out.

As investment in power infrastructure, renewable energy, electric mobility and electronics manufacturing continues to accelerate, improved access to imported cathodes could strengthen feedstock security for downstream manufacturers and reinforce India's position as one of the world's fastest-growing copper-consuming markets.