Asian thermal coal prices extend correction as comfortable supply in China keeps buyers in control

...

- Indonesian coal remains firm, Australian prices drop sharper

- Rising hydropower generation in China reduces demand

Asian thermal coal prices extended their correction during the week ended 26 June as comfortable supply across China continued to outweigh the onset of peak summer electricity demand. While utilities remained active in the market, procurement continued to be measured rather than aggressive, reflecting confidence in domestic coal availability, elevated inventories, and improving hydropower generation.

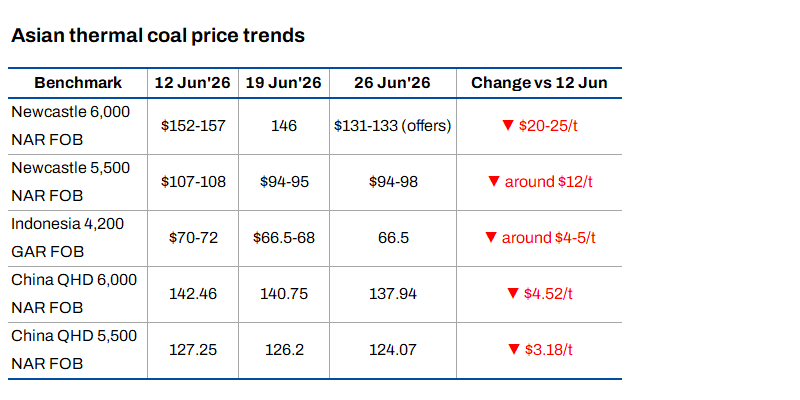

The correction has been led by Australia's premium high-calorific Newcastle market, which has lost more than $20/t from its mid-June highs. By contrast, Indonesian lower-calorific coal has remained comparatively resilient, as its cost competitiveness continues to support demand from price-sensitive buyers across Asia.

The latest Chinese utility tenders reinforce the view that the market is undergoing a gradual price correction rather than experiencing a collapse in demand. Buyers continue to secure cargoes for July and August delivery, but almost every successive procurement round has been concluded at lower price levels, confirming that utilities remain firmly in control of negotiations.

China continues to dictate regional price direction

The latest developments across Asia reaffirm that China remains the principal driver of regional thermal coal pricing. Rather than signalling weakening demand, recent procurement activity points to a market where buyers remain well supplied and are therefore able to purchase selectively.

Domestic thermal coal fundamentals continue to favour consumers. Port inventories remain elevated, power plants are carrying comfortable coal stocks, and domestic mine production remains stable. At the same time, stronger hydropower generation following widespread rainfall has reduced immediate reliance on coal-fired generation, delaying the seasonal increase in utility coal consumption. These factors have collectively allowed Chinese utilities to approach the market without urgency, placing continued downward pressure on both domestic and imported coal prices.

Unlike thermal coal, however, China's coking coal market continues to exhibit much tighter fundamentals. Ongoing mine safety inspections, slower production recovery and continued inventory depletion have provided support to metallurgical coal and coke prices, creating a growing divergence between the two coal markets. This distinction has become an increasingly important feature of the broader Asian coal market.

Utility tenders confirm disciplined procurement

Recent utility tenders provide further evidence that Chinese buyers remain active despite the softer market.

These awards illustrate a market where procurement continues steadily but at progressively lower price levels. Utilities are neither delaying purchases indefinitely nor competing aggressively for prompt cargoes. Instead, buyers appear content to replenish inventories incrementally while taking advantage of improving market conditions.

This measured buying behaviour has become one of the defining characteristics of the current market. Rather than concerns over supply security, purchasing decisions are increasingly being driven by inventory management and price optimisation.

Australia's premium coal market bears the brunt of the correction

The sharpest adjustment across Asia has occurred in Australia's premium Newcastle market.

FOB Newcastle 6,000 NAR prices have fallen by more than $20/t from their mid-June highs as buying interest from Northeast Asia moderated and Chinese import demand became increasingly selective. With comfortable domestic inventories reducing China's dependence on premium imported coal, higher-priced Australian cargoes have faced the greatest downward pressure across the seaborne market.

Trading activity has also slowed noticeably. Bid levels have fallen rapidly while sellers have progressively lowered offers in response to weaker buying interest. Although the correction has been significant, the market continues to function normally, with participants gradually adjusting expectations rather than experiencing a disorderly decline.

The correction has also narrowed the premium traditionally enjoyed by high-calorific Australian coal, reflecting buyers' increasing emphasis on delivered fuel costs rather than maximising calorific value.

Indonesian coal demonstrates relative resilience

Indonesia's export market has remained comparatively resilient despite the broader weakness affecting regional benchmarks.

FOB 4,200 GAR coal has eased from around US$70-72/t earlier in June to approximately US$66.50/t by the final week of the month. While prices have softened, the magnitude of the decline has been considerably smaller than that experienced by Australian premium coal.

This relative resilience reflects Indonesia's continued competitiveness within Asian utility fuel portfolios. Lower-calorific coal remains attractive for many buyers because of its lower delivered cost, particularly in China, India, and Southeast Asia, where cost optimisation remains an important procurement objective.

Consequently, while Indonesian suppliers have also adjusted prices lower, demand has remained sufficiently steady to prevent the sharper correction observed in Australia's higher-quality export market.

Seaborne prices continue to follow China's domestic fundamentals

The recent correction demonstrates that regional thermal coal prices are increasingly responding to developments within China's domestic market rather than to concerns over international supply availability.

Chinese utilities continue to purchase imported cargoes, but elevated inventories have removed the urgency that characterised earlier procurement cycles. This has enabled buyers to negotiate lower prices while suppliers gradually align offers with prevailing market conditions.

The steady decline in Qinhuangdao FOB markers over recent weeks reinforces this trend. Domestic prices have softened alongside imported cargo values, indicating that the regional correction is being driven primarily by comfortable supply-demand fundamentals rather than by any sudden deterioration in consumption.

Outlook

Asian thermal coal markets enter July with buyers maintaining a clear negotiating advantage.

China's domestic market continues to set the tone for the region through comfortable inventories, stable domestic production and stronger hydropower generation. These conditions have reduced procurement urgency and placed sustained pressure on seaborne prices, particularly for Australia's premium export coal.

The principal uncertainty now lies in the weather. Should prolonged heatwaves significantly increase electricity demand across China during July, daily coal consumption could rise sufficiently to accelerate inventory drawdowns and stabilise prices. Until that occurs, however, buyers are likely to remain disciplined and continue purchasing only as required.

Accordingly, the regional thermal coal market is expected to remain under pressure in the near term, although the pace of correction should moderate following the sharp declines already witnessed during June. The contrast with the metallurgical coal market is also likely to persist, with thermal coal continuing to be driven by comfortable supply conditions while coking coal remains supported by tighter domestic production fundamentals and ongoing mine inspections.