UAE: Domestic scrap prices rise w-o-w amid stronger demand, export policy uncertainty

...

- UAE considering introduction of temporary 4-month export restriction

- Billet demand remains firm across the GCC despite logistical challenges

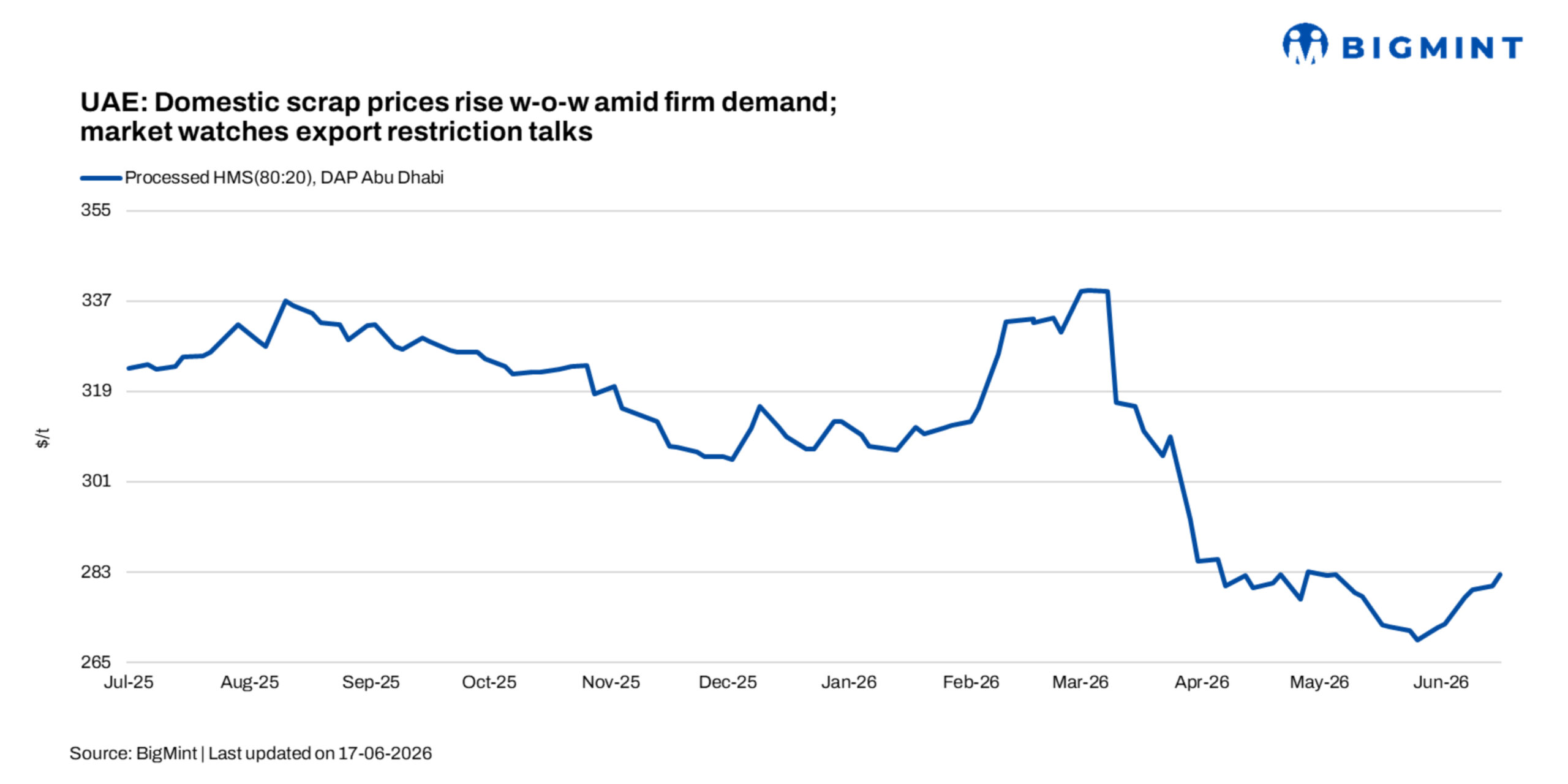

UAE domestic ferrous scrap prices strengthened during the week ended on 19 June, supported by steady demand from steelmakers and growing discussions around a potential temporary scrap export restriction.

BigMint assessed HMS (80:20) processed scrap at AED 1,038/t ($283/t) DAP Abu Dhabi, up AED 11/t ($3/t) w-o-w. Market participants indicated that while material availability remained comfortable across most grades, improving sentiment helped support higher tradable levels.

Delivered domestic scrap prices, excluding 5% VAT, were assessed at AED 750-800/t ($204-217/t) for LMS and AED 900-930/t ($245-254/t) for HMS (80:20), while HMS sheared (processed) stood at AED 1,025-1,040/t ($279-284/t). Processed PNS scrap was assessed at AED 1,030-1,050/t ($281-286/t), fabrication scrap at AED 1,040-1,080/t ($283-294/t).

Export restriction discussions support sentiment

Market participants reported the introduction of a temporary four-month export restriction covering ferrous scrap, aluminium scrap, and copper scrap under a new ministerial decision. While official clarification remains awaited, the development has already drawn attention across regional scrap markets, particularly in Pakistan and India.

The reported measure aligns with the UAE's broader strategy of retaining more recyclable material domestically to support recycling, manufacturing, and industrial development. Industry estimates suggest the UAE generates around 2-3 mnt of ferrous scrap annually, with nearly 50% traditionally exported to South Asian markets, particularly Pakistan.

Buying interest for UAE-origin HMS and shredded scrap was reported at $410-430/t CFR Port Qasim. Despite inquiries, transaction activity remained subdued, as Pakistani buyers largely limited purchases to immediate requirements. Market participants cited elevated offer levels and ongoing regional uncertainty as key factors constraining fresh bookings.

Billet demand remains resilient

Interest in billets across the GCC continues to remain relatively strong as buyers diversify procurement sources to improve supply security and reduce dependence on traditional suppliers amid ongoing logistical uncertainty.

A deal for 50,000 t of Chinese billets for August shipment was reportedly concluded in the UAE last week at around $540-545/t CFR. Market participants noted that tradable billet levels in the UAE currently remain within a similar range.

At the same time, logistical disruptions continue to affect regional trade flows. A previously booked billet vessel destined for the UAE is reportedly still awaiting a berth at Sohar port, highlighting congestion challenges facing the region.

Algerian billet has also emerged as a potential alternative source for GCC buyers. Market sources indicated that offers generated considerable interest among UAE consumers, although transaction and banking-related complexities have limited the development of direct trade.

Steel sector expansion supports long-term scrap demand

The reported export restriction discussions come as the UAE continues to expand its domestic steel-processing sector under the government's 'Make it in the Emirates' initiative.

CIM Steel Industry recently commenced operations at its new 500,000 t/year cold rolling mill, strengthening the country's flat steel processing capabilities and reducing dependence on imported cold-rolled products. The company has also signed memorandums of understanding with Rhino Steel and Dana Steel to support future offtake arrangements and strengthen integration within the domestic steel value chain. Market participants believe these investments could gradually increase domestic scrap consumption and reinforce the rationale for retaining a larger share of locally generated scrap within the UAE.

Outlook

UAE scrap prices are expected to trade within a narrow range in the coming weeks. Ample scrap availability is likely to limit significant upside, but firm billet demand, growing domestic steel-processing capacity, and the prospect of export restrictions could provide underlying support to the market. Participants are closely monitoring regulatory developments, which may influence regional scrap trade flows and domestic procurement strategies.