UAE: Domestic ferrous scrap eases w-o-w; regional mills follow Emirates Steel's rebar price hike

...

- Need-based procurement keeps the domestic scrap market under pressure

- Export restrictions strengthen long-term domestic scrap supply outlook

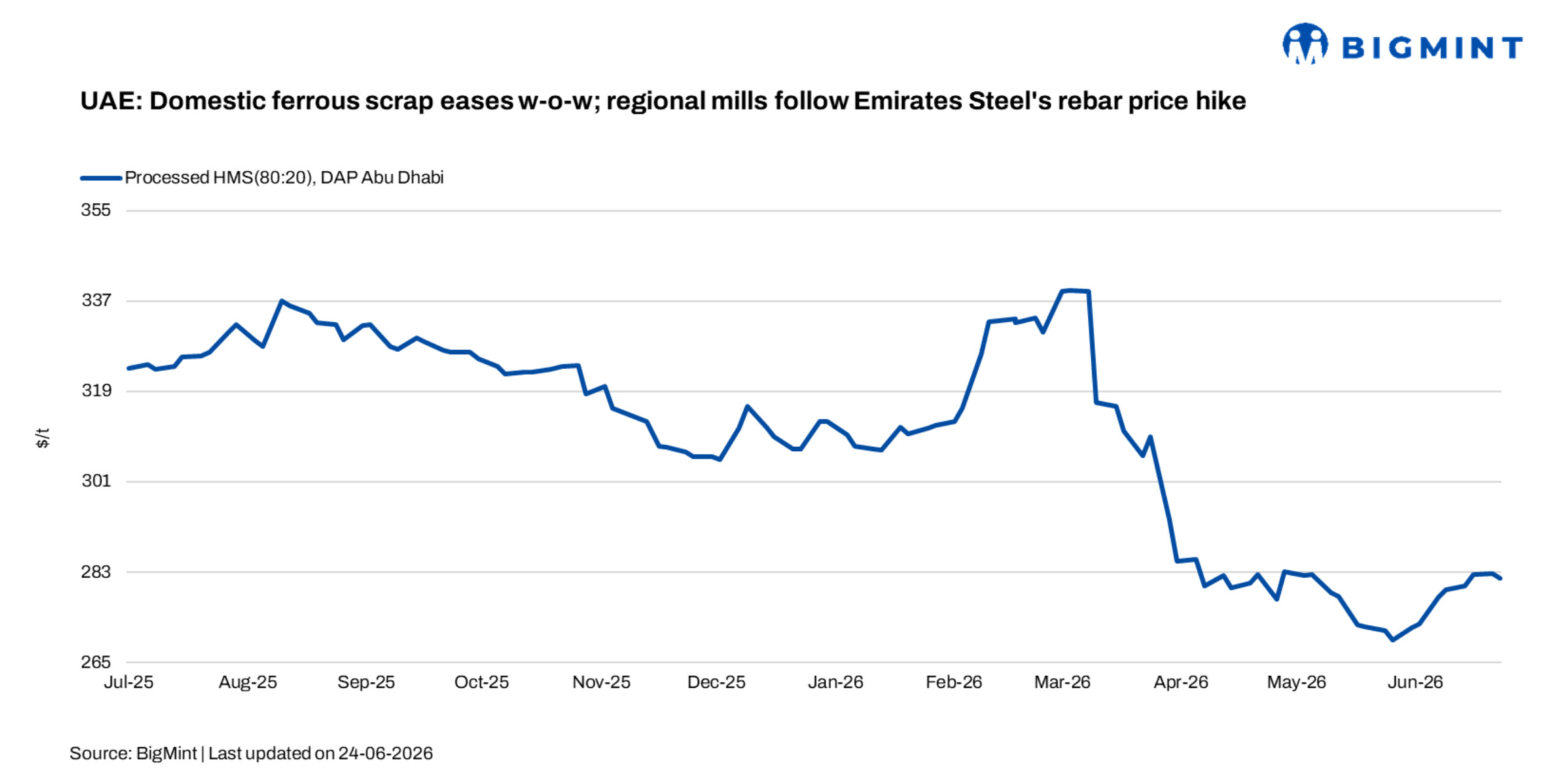

In the UAE's domestic scrap market, prices edged lower in the week ended 26 June 2026, reflecting subdued buying activity despite supportive policy developments. BigMint assessed HMS (80:20) processed scrap at AED 1,035/t ($282/t) DAP Abu Dhabi, down AED 3/t ($1/t) w-o-w, as need-based mill procurement outweighed positive sentiment stemming from the UAE's tightening scrap export policy.

Steelmakers continued to purchase cautiously despite expectations that the government's latest export restrictions will improve domestic scrap availability and strengthen raw material security over the coming months.

Indicative domestic scrap prices were assessed at AED 740-780/t ($201-212/t) for LMS, AED 900-910/t ($245-248/t) for HMS (80:20), AED 1,030-1,035/t ($280-282/t) for processed HMS (80:20), AED 1,030-1,050/t ($280-286/t) for processed PNS, and AED 1,020-1,070/t ($277-291/t) for fabrication scrap.

UAE imposes four-month scrap export ban

The key development during the week was the UAE's formal implementation of a temporary ban on exports of ferrous, aluminium, and copper scrap, effective from 10 June to 8 October 2026. The measure builds on earlier initiatives, including the AED 400/t ($109/t) ferrous scrap export duty and the reverse-charge VAT mechanism, as the government continues to prioritise domestic availability of secondary raw materials.

While the policy had little immediate impact on domestic scrap prices, market participants expect it to gradually improve feedstock availability for local electric-arc furnace (EAF) steelmakers and strengthen raw material security.

However, traders noted that previous restrictions did not completely disrupt exports, suggesting the practical impact will depend on how exemptions are implemented and enforced.

The UAE's temporary scrap export ban also weighed on sentiment in Pakistan's imported scrap market. Market participants had expected buying activity to gradually recover following the easing of geopolitical tensions in the Middle East. However, the latest export restrictions have renewed concerns over raw material availability, as the UAE remains one of Pakistan's key sources of ferrous scrap.

Buying activity in Pakistan remained subdued during the week due to seasonal holidays and weak long-steel demand. While some buyers expressed concerns that the export ban could tighten scrap availability and complicate procurement, market participants noted that previous UAE restrictions did not completely disrupt trade flows. As a result, the market is closely monitoring whether exemptions under the new policy will allow shipments to continue.

In the finished steel segment, regional producers adopted a more bullish pricing strategy after the benchmark UAE mill increased July rebar prices by AED 100/t ($27/t) to AED 2,921/t ($795/t) exw. An Omani integrated producer subsequently raised its July offers to around AED 2,900-2,910/t ($789-792/t) CPT UAE, while other UAE- and Qatar-linked mills announced similar price levels in an effort to maintain pricing parity across the region.

Despite the coordinated price increases, buyer acceptance remained cautious. Retail rebar prices rose by only AED 35-40/t ($10-11/t) to around AED 3,070-3,100/t ($836-843/t) DAP, well below the announced mill hikes. Market participants attributed the limited pass-through to comfortable distributor inventories, cautious project buying, and continued competition for sales volumes.

Outlook

Overall, the UAE market ended the week with contrasting fundamentals. Government policy is expected to strengthen domestic scrap availability and improve long-term raw material security for steelmakers. However, subdued scrap procurement and cautious downstream steel demand indicate that producers' ability to sustain higher rebar prices will depend on stronger construction activity and improved buying interest during the July sales cycle.