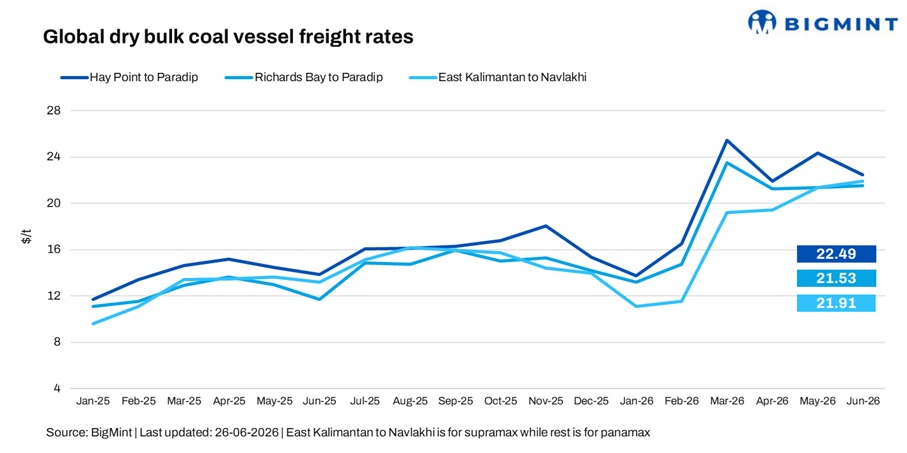

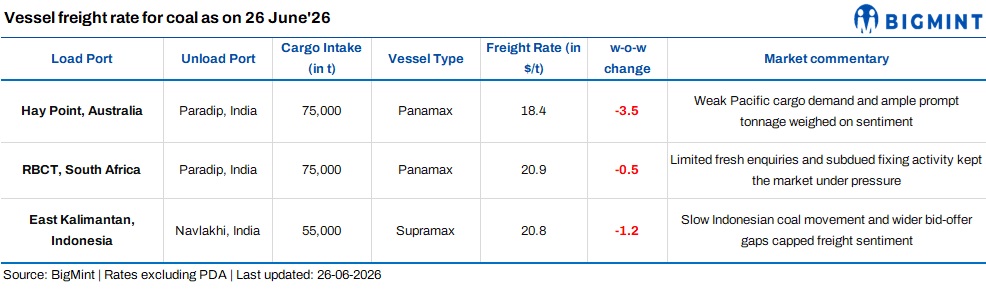

India: Coal freights lose ground as Pacific weakness overshadows Atlantic support

...

- Panamax pressured by weak Pacific cargo demand

- Supramax eases amid muted Indonesian activity

India's dry bulk coal freight market weakened in the assessment week ended 26 June 2026, with freight rates retreating across key Panamax and Supramax routes as the Pacific basin continued to grapple with subdued cargo demand and abundant prompt vessel availability. Although owners showed greater resistance to lower freight ideas, particularly after firmer Forward Freight Agreements (FFAs), oversupply of vessels and limited fresh enquiries kept overall sentiment under pressure.

The Atlantic continued to lend some underlying support, but weaker activity across Southeast Asia and Indonesia outweighed the positive signals, preventing a broader market recovery.

A shipbroker said, "The market has softened a bit recently, but I believe it's only a temporary phase. It should recover once fresh cargoes start coming in."

Another trader echoed the mixed regional picture, saying, "The Cape market has softened, Panamax is holding on for the time being, Supramax has eased, while the Handy segment remains largely unchanged."

Despite the recent correction, market participants largely expect the weakness to be short-lived. "The market is taking some time to adjust. Once things settle, we should see freight rates returning to levels seen previously," another shipbroker said.

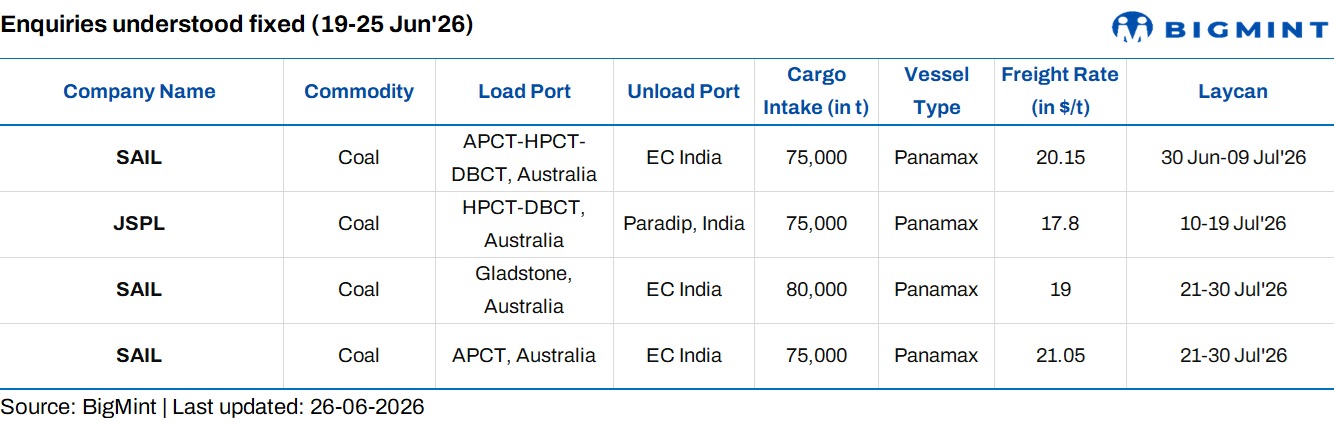

Route-wise update

Market highlights

- Baltic Dry Index (BDI) extends losses w-o-w: The BDI declined by 2.3% (62 points) w-o-w to 2,591 on 25 June, from 2,653 a week earlier, reflecting continued weakness across the larger vessel segments. The Panamax index fell by 5.7% (127 points) to 2,096, weighed down by excess prompt tonnage and subdued cargo demand across the Pacific. Meanwhile, the Supramax index slipped by 1.6% (27 points) to 1,678, as slower trading activity in Asia and wider bid-offer gaps offset relatively steady demand in the Atlantic.

- Bunker prices rebound w-o-w: Bunker prices increased by $46/t w-o-w to $713/t as of 26 June, from $667/t a week earlier, supported by firmer fuel oil values and higher crude oil prices amid ongoing geopolitical uncertainties and improving energy market sentiment.

- Brent crude futures extend losses w-o-w: Brent crude oil (August 2026 contract) was assessed at $72.78/bbl on 26 June, down $7.12/bbl w-o-w from $79.90/bbl a week earlier, as easing geopolitical tensions and improving supply expectations outweighed concerns over global demand, keeping crude prices under pressure.

- DCE coke futures soften w-o-w: Coke futures on the Dalian Commodity Exchange eased to RMB 1,946/t ($286.01/t) for the September 2026 contract as of 26 June, down from RMB 2,019.50/t ($298.33/t) a week earlier. The decline reflected weaker market sentiment amid subdued steel demand, softer coke fundamentals and cautious expectations surrounding China's steel production outlook.

Outlook

Coal freight rates to India are expected to remain range-bound in the near term. While the Pacific market continues to face pressure from ample prompt tonnage and measured cargo activity, expectations of vessels repositioning towards the South Atlantic could gradually tighten regional supply and stabilise freight levels. Market participants anticipate that a pickup in fresh cargo enquiries, particularly from Australia and Indonesia, will be key to restoring momentum, although near-term sentiment is likely to remain cautious.