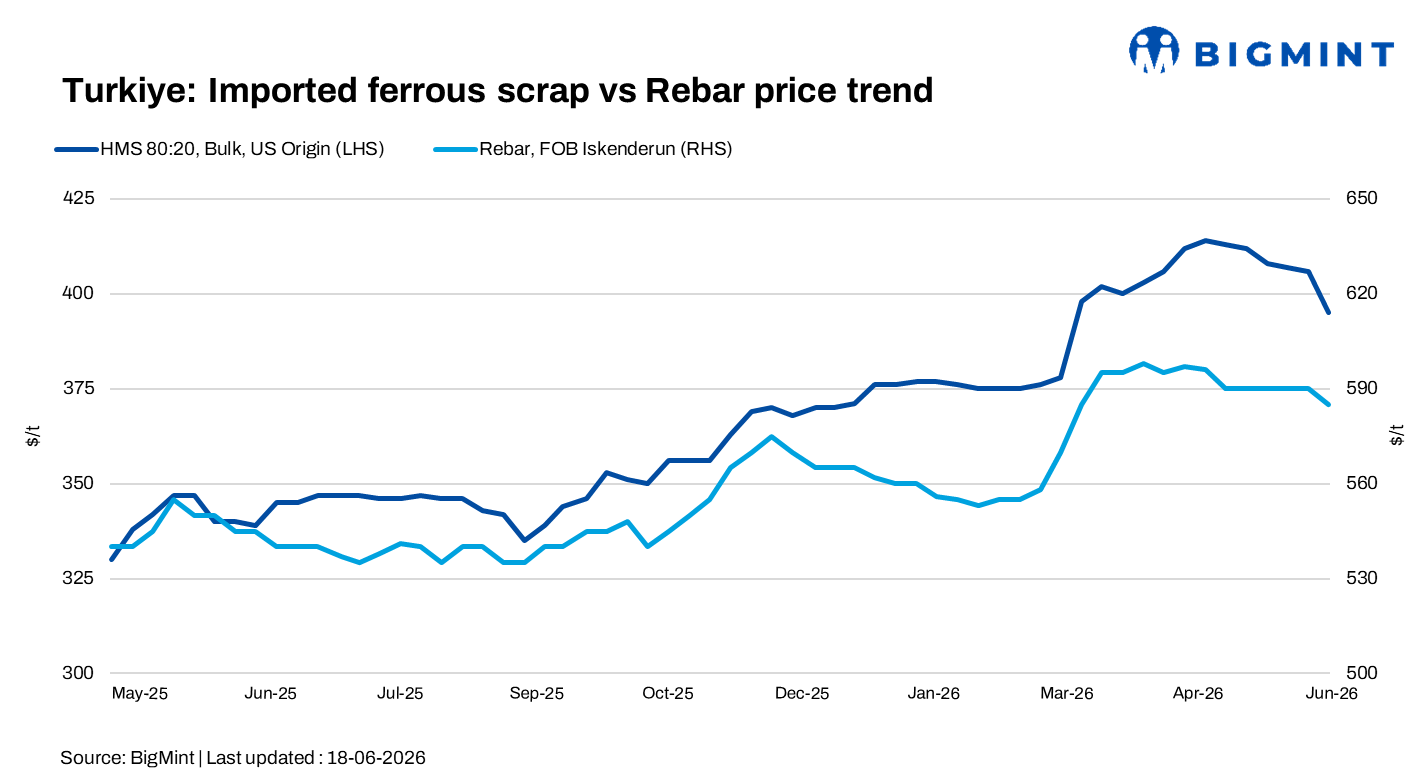

Turkiye: Weak steel demand drags imported scrap prices lower by $10/t w-o-w

...

- Scrap-to-rebar spread hovers under $190/t

- Mills target lower scrap levels as sentiment deteriorates

Turkish deep-sea imported scrap market sentiment weakened further during the week ended 18 June, as sluggish finished steel demand, declining rebar prices, and limited booking activity continued to pressure both buyers and suppliers. Mills largely remained on the sidelines, focusing on finished steel sales and margin protection rather than rebuilding scrap inventories. Market participants noted that the market has been moving lower consistently, with some expecting the next support level to emerge around $380-385/t CFR if steel demand fails to improve.

Price assessments

- US-origin HMS 80:20 around $395/t CFR Turkiye, down by $11/t w-o-w.

- US East Coast HMS 80:20 around $362/t FOB, down $9/t w-o-w.

US-origin material continued to command a premium due to limited availability and stronger domestic demand. However, lower-priced deals during the week reflected softer market sentiment. Overall, around 5-6 deals were concluded within the range of $386-392/t CFR.

Deals earlier in the week were concluded at $391-392/t CFR for Germany- and France-origin cargoes. However, prices eased later, with Netherlands- and France-origin cargoes booked at $386/t CFR, Russia-origin material at $387/t CFR, and Bulgaria-origin scrap at $363-365/t CFR, indicating a softer market tone as the week progressed.

Turkish export rebar offers slipped below $585/t FOB during the week, while domestic rebar sales were heard around $580-600/t exw. Weak finished steel demand and lower rebar prices continued to pressure mill margins, keeping the scrap-to-rebar spread constrained at around $189-190/t and weighing on scrap buying sentiment.

Market comments

Market participants reported that Turkish mills continued resisting higher prices, with bids for US-origin HMS 80:20 heard in the low $390/t CFR range. However, US suppliers remained reluctant to reduce offers below $400/t CFR, supported by stronger domestic demand and stable US market conditions.

A Europe-based recycler commented, "Mills are struggling to move rebar volumes, so naturally they continue pushing for lower scrap prices."

Market sources added that Western European and UK exporters may be forced to accept lower prices if bookings do not improve, as prolonged inventory holding becomes increasingly expensive.

Another Baltic-based supplier noted, "US exporters are in no hurry to sell aggressively into Turkiye because domestic demand remains supportive. However, European suppliers face greater pressure due to financing costs and inventory-carrying expenses."

Steel market pressure continues

Weakness in the finished steel market remained the primary factor weighing on scrap demand. Domestic rebar offers were heard at $580-600/t exw depending on region, while export rebar offers fell below $590/t FOB. Market participants reported that demand has failed to recover despite recent price reductions, leaving mills under pressure to further reduce raw material costs.

At the same time, billet prices remained under pressure, further weighing on scrap demand. Lower-priced billet alternatives continued to compete with scrap-based steel production, reducing mills' urgency to secure fresh scrap cargoes and encouraging buyers to push for lower raw material prices.

Although some market participants expected demand to improve later in the summer, the majority remained cautious due to poor steel consumption and limited export sales.

Additionally, Turkish integrated steelmakers Erdemir and Isdemir announced new solar power investments as part of their decarbonisation strategies. The projects support broader plans to reduce carbon emissions through renewable energy, electric arc furnace investments, and future hydrogen-based DRI production. While the developments are unlikely to impact near-term scrap demand, they reinforce the long-term importance of scrap-based steelmaking in Turkiye.

Outlook

Turkish mills are expected to continue purchasing scrap on a hand-to-mouth basis in the coming weeks as weak rebar demand and squeezed steel margins limit buying appetite. Although suppliers remain reluctant to reduce prices aggressively, continued weakness in finished steel markets and comfortable inventory levels are likely to keep pressure on scrap prices. Market participants increasingly view the $380-385/t CFR range as the next key support level, with any recovery dependent on a meaningful improvement in domestic and export steel demand.