Turkiye scrap import prices slide as focus returns to pre-war pricing

...

- Mills target $370-375/t CFR to restore profitability

- Steel market weakness continues to weigh on buying interest

Turkish deep-sea imported ferrous scrap prices remained under downward pressure during the week ended 25 June, as weak finished steel demand, falling rebar prices, and limited booking activity continued to weigh on market sentiment. Mills remained largely cautious, prioritising margin preservation and inventory management while pushing for lower raw material costs amid subdued steel sales.

Price assessments

- US-originHMS 80:20 around $383/t CFR Turkiye, down by $12/t w-o-w.

- US East CoastHMS 80:20 around $353/t FOB, down $9/t w-o-w.

On the supply side, US exporters continued to resist deeper price cuts despite softer Turkish demand, supported by relatively stable domestic market conditions. In contrast, European recyclers faced increasing pressure from weaker regional demand, inventory-carrying costs, and a softer euro, making them more willing sellers at lower price levels.

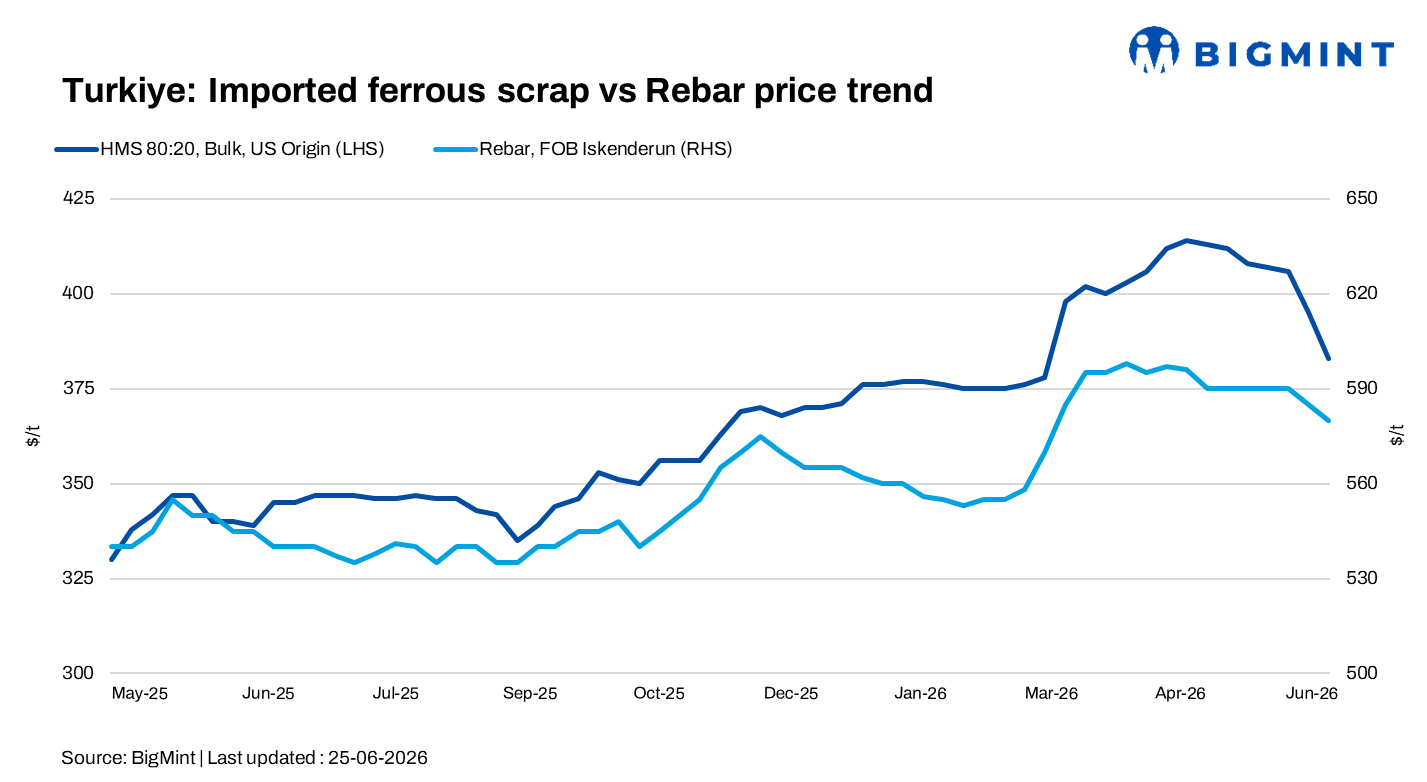

Domestic rebar prices remained under pressure while export rebar hovered around $578-580/t FOB, leaving the scrap-to-rebar spread compressed at around $190-195/t. As profitability across the steel value chain continued to deteriorate, mills intensified efforts to lower raw material costs, with many market participants indicating that HMS 80:20 would need to decline toward $370-375/t CFR to restore a more sustainable spread near $200/t.

Around 4-5 deep-sea scrap transactions were heard to have been concluded during the week. These included a Netherlands-origin HMS 80:20 cargo at $380/t CFR Turkiye, a France-origin cargo at $379/t CFR for 19,000 t, another France-origin cargo at $383/t CFR, and a US-origin HMS 80:20 cargo at around $388/t CFR. Market sources also reported rumours of potential transactions involving TSR Germany and TSR Netherlands, although these remained unconfirmed. Fresh US-origin offers were subsequently indicated at $385-388/t CFR, while European-origin HMS 80:20 was largely discussed at $375-380/t CFR. Some major recyclers were reportedly willing to conclude deals at $380-382/t CFR to secure prompt bookings.

Trading activity remained subdued throughout the week, with market participants divided over the near-term outlook. While weak finished steel demand continued to weigh on sentiment and supported expectations of further downside, the absence of aggressive selling from US exporters helped prevent a sharper correction in prices.

Market comments

Market sentiment softened during the week as Turkish mills stepped up efforts to secure imported scrap at lower prices amid shrinking steel margins and weak finished steel demand. With profitability under pressure, buyers remained focused on reducing raw material costs, with some targeting HMS 80:20 prices in the low-$370s/t CFR range.

A US trader said, "Mills are reluctant to pay higher scrap prices while rebar values remain under pressure and margins have virtually disappeared. The maximum workable level for US-origin cargoes is around $380-382/t CFR."

A Baltic-origin supplier said workable levels for Europe- and Baltic-origin HMS 80:20 had eased to $370-375/t CFR, adding that several deals were heard around $375/t CFR in recent days, indicating that sellers were becoming more flexible to secure business.

A European trader said major European recyclers were willing to negotiate prompt cargoes at $380-382/t CFR amid weaker regional demand and mounting inventory pressure. However, the trader noted that US exporters continued to benefit from relatively firm domestic scrap prices, limiting the scope for deeper price reductions.

Pressure intensifies in steel market

Weakness in downstream steel markets remained the primary bearish driver for scrap demand. Turkish rebar demand remained sluggish across both domestic and export markets despite recent price reductions, while billet continued to offer a competitive alternative to scrap-based steel production. At the same time, Turkish mills continued purchasing scrap only on a hand-to-mouth basis, limiting buying visibility and reducing support for higher prices.

Outlook

Turkish imported scrap prices are expected to remain under pressure in the coming weeks as weak rebar demand, squeezed mill margins, and cautious buying continue to weigh on market sentiment. Although firm US domestic scrap prices may limit the pace of any further decline, increasing willingness among European recyclers to negotiate at lower levels points to continued downside pressure.

Market participants also noted that Turkish mills have increasingly opted for billet imports in recent months as imported scrap prices rose, reducing their dependence on deep-sea scrap. Unless finished steel demand improves and mill profitability recovers, buyers are likely to maintain pressure on scrap prices by seeking lower procurement levels.