Steel prices hold steady despite subdued demand in South India

...

- Rebar inventories at mills rise sharply to around 30-35 days

- Higher production costs support prices despite slow demand

Steel prices across the southern Indian states remained largely stable or experienced minor corrections during the week ended 19 June 2026 amid subdued demand, which was partially offset by elevated production costs. Manufacturers maintained their offers as lower realisation could further pressure already thin operating margins.

Market activity remained slow, with bulk transactions being limited. Both intermediaries and end-users continued to adopt a cautious, wait-and-watch approach, preferring to assess market trends before making large-volume purchases.

Sponge iron, melting scrap

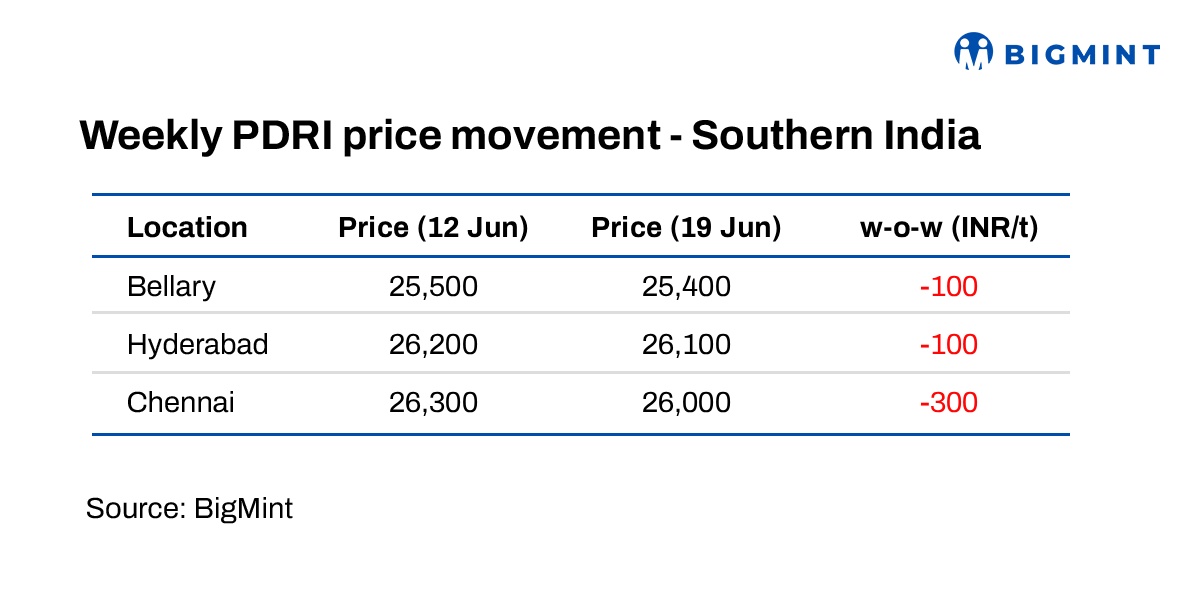

Sponge iron prices in the Bellary market remained largely stable or experienced minor corrections of INR 100-200/t during the week, with no significant fluctuations observed. PDRI prices in Bellary were assessed at around INR 25,400/t on 19 June 2026. The market continued to draw support from steady lifting by steel manufacturers for previously booked orders.

Trading activity in the spot market remained subdued as most sponge iron producers are currently focused on executing existing commitments. Fresh procurement inquiries from steel manufacturers were limited, resulting in a cautious market sentiment.

A market participant stated, Despite a major merchant supplier diverting its sponge iron supplies to units in neighboring states and limiting local market offerings, no significant supply concerns were heard in the Bellary pellet-based sponge iron market, as there were limited buying enquiries from buyers."

Steel producers continued to follow a wait-and-watch approach amid weak finished steel demand and poor conversion margins, resulting in limited sponge iron bookings. Consequently, several small-scale sponge iron units have suspended operations, while mid- and large-scale producers have reduced production by around 30-40% across the region.

On the raw material front, iron ore pellet (Fe 63%) prices witnessed a correction. As of 19 June 2026, pellet prices were hovering around INR 9,850/t ex-Bellary, down by INR 200/t, providing some cost relief to sponge iron manufacturers.

Similarly, imported RB2 coal prices softened by approximately INR 150/t w-o-w to around INR 11,400/t ex-Gangavaram as of 19 June 2026. The decline in coal prices has marginally eased production costs for sponge iron producers.

Melting scrap prices also witnessed slight down during the week, with HMS (80:20) assessed at around INR 31,700/t FOR Chennai. Lower prices of alternative raw materials, particularly sponge iron, limited any upward movement and prompted scrap suppliers to reduce prices.

Mild steel billet

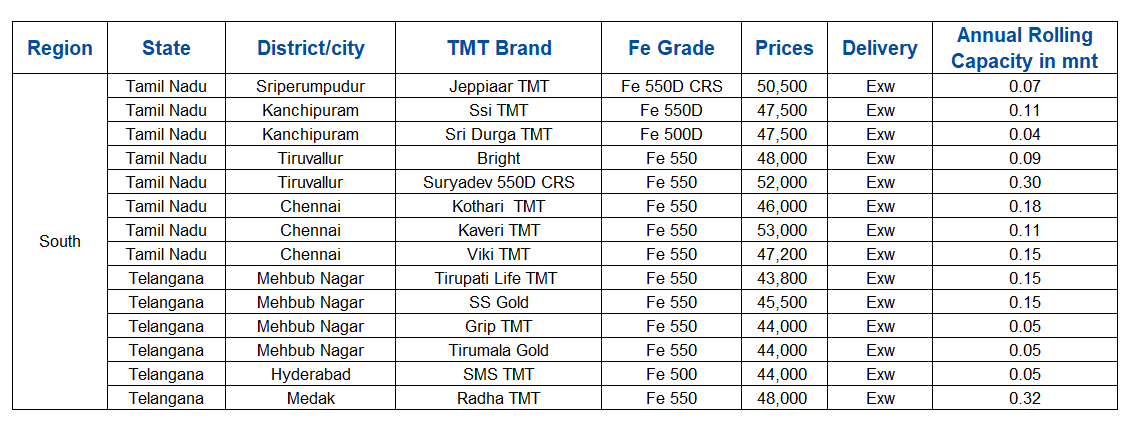

Mild steel (MS) billet prices across the southern Indian market remained largely stable during the week, with no major price movements observed. Market participants reported that billet producers maintained prices at existing levels amid weak demand from re-rolling mills.

Demand from re-rollers remained slow due to subdued finished steel consumption and limited order bookings. However, billet manufacturers refrained from reducing prices further as production costs remain elevated.

The conversion cost from imported HMS (80:20) scrap to MS billet in Chennai was estimated at around INR 9,500/t as of 19 June 2026. Higher raw material and processing costs supported billet prices despite sluggish market activity.

Meanwhile, a major billet manufacturer in Chennai indicated that discussions are ongoing for an export order. The deal has not yet been finalized, and market participants are closely monitoring its progress as it could provide some support to demand.

As of 19 June 2026, MS billet prices in Hyderabad were assessed stable w-o-w at around INR 40,300/t, while Chennai billet prices were higher at approximately INR 41,200/t, again stable w-o-w.

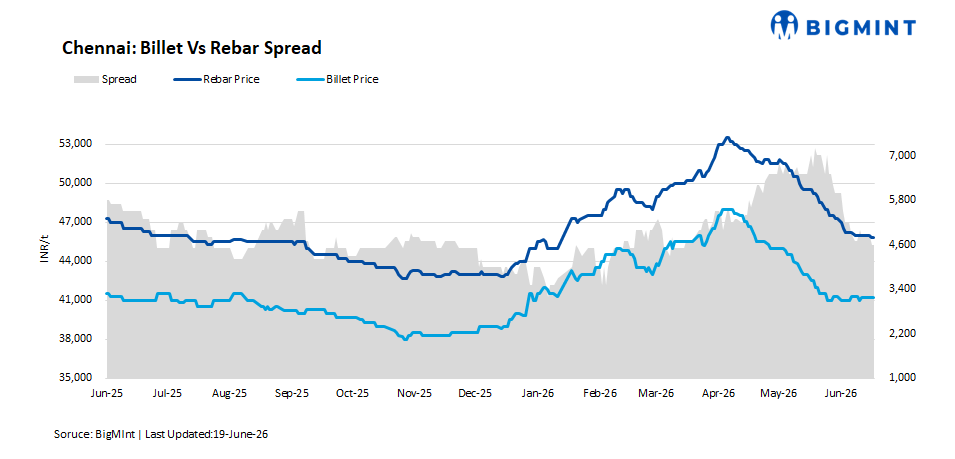

Rebar

Induction furnace (IF) rebar prices in the southern Indian markets, particularly Hyderabad and Chennai, remained largely stable during the week, witnessing only a marginal fluctuation of around INR 200-300/t w-o-w. Limited buying activity and cautious market sentiment kept prices within a narrow range.

According to major rebar manufacturers, inventory levels at mills have increased significantly and are currently estimated at around 30-35 days, depending on the size and category of the mill. The inventory build-up has been primarily driven by slower sales and weak demand from end-users.

Market participants reported that trading activities remain subdued, resulting in slower cash flow and limited money rotation across the supply chain. This has negatively impacted overall business sentiment and restricted fresh procurement by traders and distributors.

Meanwhile, blast furnace (BF) route rebar prices witnessed a correction of approximately INR 1,000-1,500/t in Hyderabad and Chennai. The decline was mainly attributed to weak demand from the construction sector and increased pressure on manufacturers to liquidate inventories amid sluggish market conditions. Prices of blast furnace route rebar were at around INR 52,500/t ex-Hyderabad.

Outlook

Steel prices are expected to witness a mild correction in the near term due to the accumulation of finished steel inventories at plant levels. Demand from end-users and traders remains subdued, resulting in slower material offtake and limited fresh bookings across the market.

Consequently, steel manufacturers may face increased sales pressure and could be compelled to offer discounts to liquidate inventories and maintain cash flows. Unless there is a notable improvement in demand from the construction, infrastructure, and manufacturing sectors, steel prices are likely to remain under pressure in the short term.