Iron ore freights remain under pressure amid sluggish trading, weaker market indicators

...

- Capesize weakness pulls Baltic index lower amid holiday slowdown

- DCE iron ore futures soften, weighing on freight sentiment

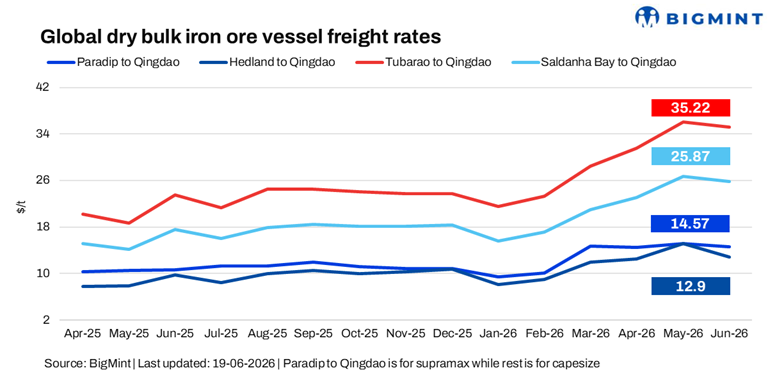

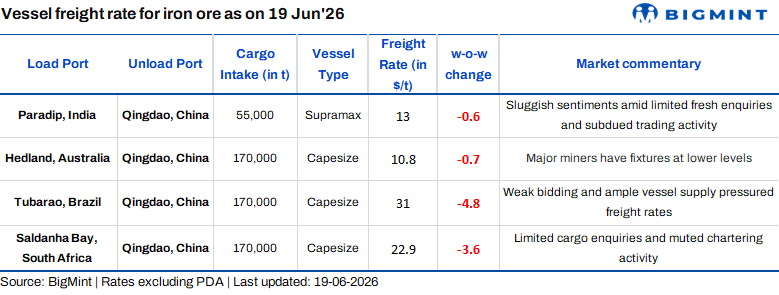

Dry bulk iron ore freight sentiment remained weak on 19 June 2026, with sluggish market activity and fixtures concluded at lower levels amid limited enquiries and cautious chartering.

Overall freight sentiment stayed bearish, as declines in the Baltic indices, bunker prices, Brent crude futures, and DCE iron ore futures reflected subdued demand and slower trading ahead of China's three-day Dragon Boat Festival holiday.

Supramax market sentiment remained weak amid limited fresh cargoes and subdued fixing activity. Soft demand for minor bulks and cautious chartering interest kept freight rates under pressure, with abundant tonnage availability further weighing on earnings.

Capesize sentiment remained weak across major iron ore routes, as limited fresh enquiries, ample vessel supply, and muted chartering activity weighed on rates. Slower trading ahead of China's three-day Dragon Boat Festival holiday and rising ballaster availability in the Atlantic further dampened market momentum.

A shipbroker stated, "Capesize and Panamax segments are softening amid limited enquiries and subdued activity ahead of China's three-day holiday, while Supramax and Handysize markets continued to hold firm despite relatively fewer cargoes."

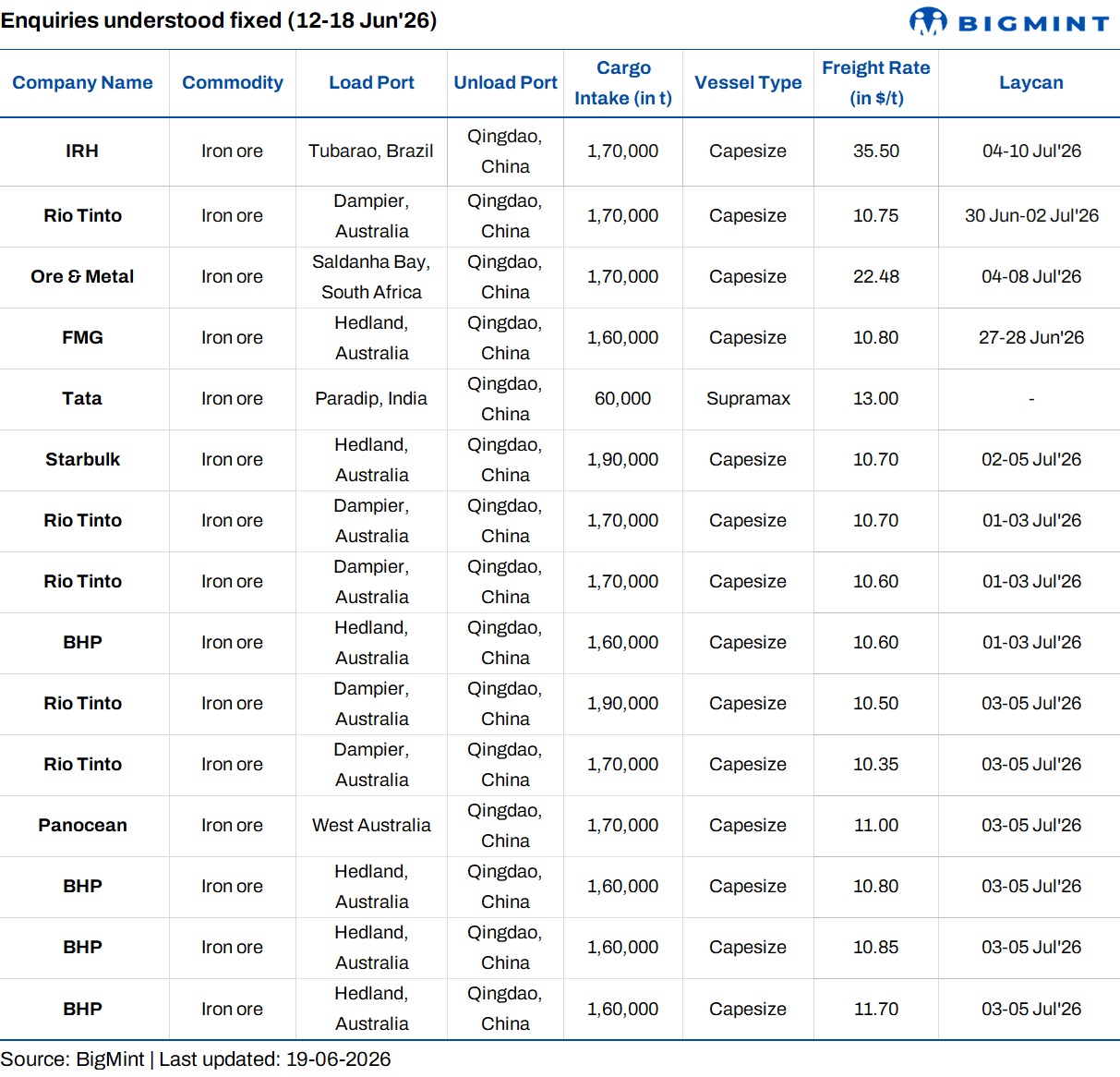

Route-wise update

Why are dry bulk iron ore freights under pressure?

- Baltic Dry Index (BDI) decreases: The BDI decreased by 3% (76 points) to 2,653 on 18 June against 12 June, pressured by weaker Capesize sentiment. The Capesize index dropped significantly by 6% (263 points) to 3,877 amid softer iron ore demand, while the Supramax index rose by 4% (72 points) to 1,705, supported by steady minor bulk cargo activity. Notably, China observes the three-day Dragon Boat Festival holiday from 19-21 June 2026.

- Bunker prices decrease w-o-w: Bunker prices fell by $46/tonne (t) w-o-w to $667/t as of 19 June, reflecting softer crude oil prices and easing fuel cost pressures amid subdued shipping activity and cautious market sentiment.

- Brent crude futures down w-o-w: Brent crude oil (August 2026 contract) was assessed at $79.9/barrel (bbl) on 19 June, down $7.21/bbl w-o-w, reflecting easing geopolitical risk premiums and softer demand expectations, which weighed on overall energy market sentiment.

- DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) fell by RMB 17/t w-o-w to RMB 747/t ($110/t) on 19 June, reflecting cautious market sentiment amid weak steel demand, softer buying interest, and concerns over elevated iron ore supply.

Outlook

Dry bulk iron ore freight rates are expected to remain under pressure in the near term, as weak market momentum, cautious chartering sentiment, and recent declines in key market indicators continue to outweigh underlying cargo demand, while the Dragon Boat Festival holiday in China is likely to keep trading activity subdued and limit prospects for a near-term recovery.