South African coal exports inch up in May'26 despite lower shipments to India

...

- Exports to India drop ~5% m-o-m

- Higher RBCT stocks support export flows

South Africa's non-coking coal exports rebounded in May'26, increasing by 19% m-o-m to 5.97 mnt from 5.02 mnt in April. However, exports remained 2.9% lower y-o-y compared with 6.15 mnt in May'25.

The recovery was supported by improved export availability, stronger RBCT stock levels and increased shipments to diversified destinations, including China, South Korea, Guinea and several European markets. Elevated inventories at Richards Bay Coal Terminal (RBCT) also helped exporters manage logistical disruptions more effectively and maintain cargo flows despite rail performance concerns.

Export offers remained well supported during May despite mixed buying sentiment. Market participants indicated that the API 4 index remained firm at around $120-122/t, providing a strong benchmark for South African exporters. FOB RB2 (5,500 NAR) offers were heard at $96-98/t, while RB3 (4,800 NAR) cargoes were around $76-78/t FOB. Higher-calorific RB1 (6,000 NAR) material was generally offered at around API 4 minus $4-5/t.

In addition, freight rates from RBCT to India remained elevated at $21-22/t, keeping landed costs high and supporting seller offers despite weak import demand from Indian buyers.

India's imports fall on declining sponge prices, shift to domestic coal

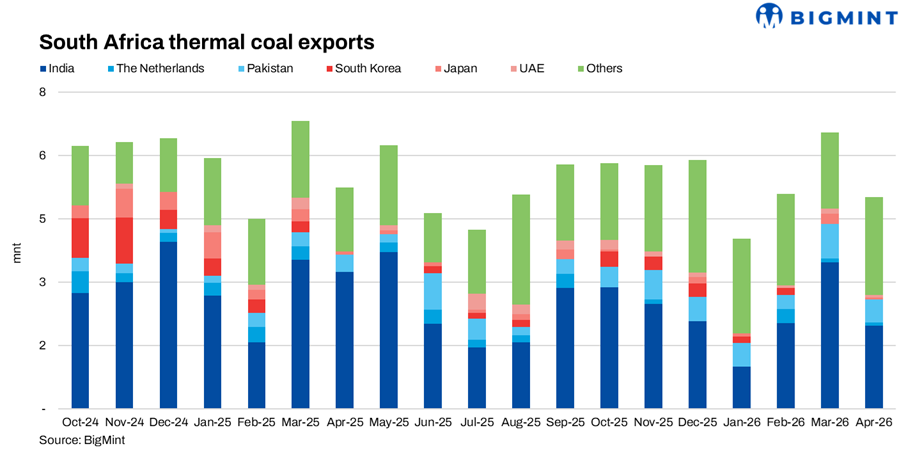

India remained the largest destination for South African non-coking coal in May, importing 2.22 mnt. However, volumes declined 3.5% m-o-m from 2.30 mnt in April and were significantly lower by 41.3% y-o-y compared with 3.78 mnt in May'25.

Indian buying interest remained weak throughout May. Market participants largely preferred domestic coal amid comfortable availability, regular CIL auctions and lower procurement costs. Imported South African coal continued facing resistance as weak sponge iron margins, subdued steel demand and elevated landed costs limited buying appetite. Procurement largely remained requirement-based, with very few bulk bookings reported across major consuming regions.

As per BigMint's assessment, ex-Paradip RB2 (5,500 NAR) remained around INR 11,350-11,500/t during May, while RB3 (4,800 NAR) was heard around INR 9,850-9,900/t. Firm FOB levels, elevated freight rates and a weaker rupee kept landed costs high, discouraging buyers from returning aggressively to the import market.

Demand-side indicators in India remained weak during May. As per BigMint's assessment, PDRI DAP-Durgapur prices declined to INR 24,852/t in May from INR 27,474/t in April, reflecting weaker sponge iron market conditions and cautious steel-sector buying. At the same time, domestic 5,000 GCV coal prices, ex-Bilaspur, declined to INR 5,806/t in May from INR 6,550/t in April, improving the competitiveness of domestic coal against imported pet coke.

Meanwhile, India's sponge iron production fell to 5.11 mnt in April from 5.36 mnt in May 2025, highlighting softer industrial fuel demand. Lower domestic coal prices, weak downstream steel sentiment and the approaching monsoon season encouraged buyers to maintain a cautious procurement approach and avoid aggressive imported pet coke purchases.

Higher RBCT inventories support exports

RBCT inventories stood near 4 mnt in May, up 3.6% m-o-m and around 18% above the long-term May average. The stronger stock position provided exporters with a larger operational buffer and reduced the impact of rail disruptions on export flows.

Unlike previous periods when logistics constraints restricted shipments, higher port inventories allowed producers greater flexibility in meeting contractual commitments and maintaining cargo availability. This was one of the key reasons overall South African exports improved during May despite weaker demand from India.

Other markets drive growth

While India imported less coal, other destinations helped offset the decline. China imported 0.34 mnt in May after recording negligible imports in April. South Korea received 0.18 mnt, while Guinea imported 0.19 mnt. UAE imports increased to 0.17 mnt from 0.11 mnt in April.

Meanwhile, Pakistan's imports fell sharply to 0.39 mnt from 0.86 mnt, while imports into Israel declined to 0.17 mnt from 0.24 mnt. Around 1.69 mnt of cargoes remained classified under unspecified destinations, indicating material still in transit or awaiting final discharge confirmation.

Outlook

South African coal exports may remain supported by healthy RBCT inventories and stable export availability. However, demand from India is likely to remain subdued in the near term as domestic coal continues to offer better economics and sponge iron demand remains weak. Unless downstream steel activity improves meaningfully, Indian buyers are expected to maintain cautious, need-based procurement strategies despite firm global coal fundamentals.