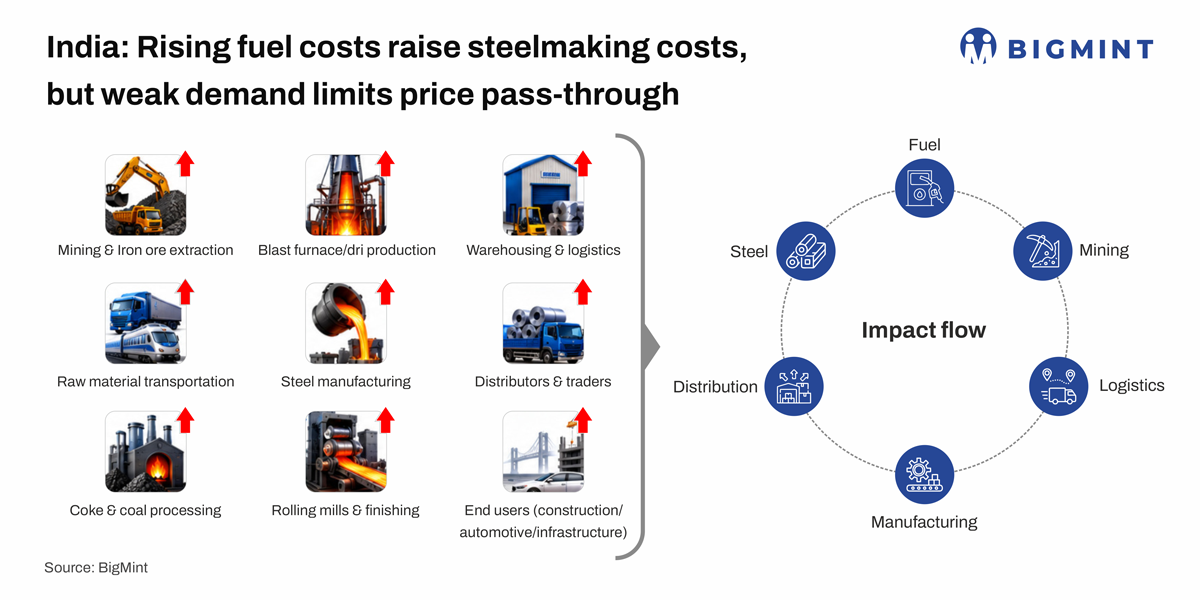

India: Rising fuel costs raise steelmaking costs, but weak demand limits price pass-through

...

- Cost pressures intensify from mine to mill

- Margins shrink as costs climb value chain

Rising fuel and energy costs have emerged as an increasingly important factor shaping India's steel market, influencing costs across mining, raw material transportation, metallic production, steelmaking, and finished steel distribution. The impact extends beyond production, affecting both inbound logistics, such as the movement of iron ore, coal, pellets, scrap, and other raw materials to steel plants and outbound logistics involving the transportation of finished steel to distributors, project sites, and export destinations.

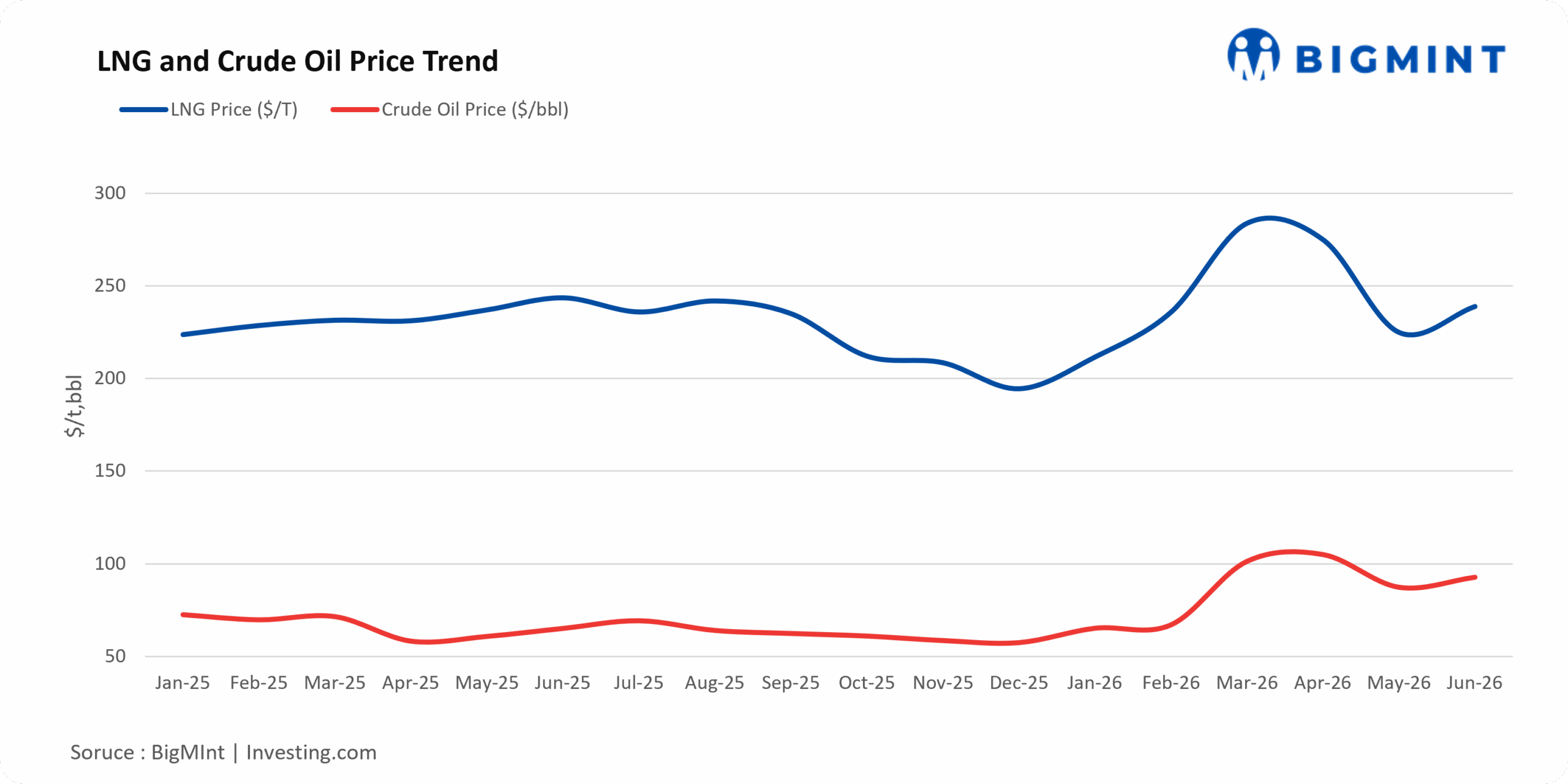

Global energy prices have witnessed a notable uptrend since the beginning of 2025, increasing cost pressures across commodity supply chains. International crude oil prices rose by nearly 28%, from $72.53/bbl in Jan'25 to $92.79/bbl in Jun'26, while touching a high of $105.07/bbl in Apr'26. Similarly, LNG prices increased by around 7%, from $223.65/t in Jan'25 to $238.82/t in Jun'26, after reaching a peak of $283.76/t in Mar'26.

Looking specifically at the period following the escalation of Middle East tensions, crude oil prices increased from approximately $70-75/bbl at the end of Feb'26 to a peak of $105.07/bbl in Apr'26 before settling at around $90-95/bbl by the end of May'26. LNG prices also strengthened during the same period, rising from around $224/t in late Feb'26 to a peak of $283.76/t in Mar'26 and remaining elevated through May'26. The sharp increase reflected heightened concerns over potential supply disruptions, increased geopolitical risk premiums, and higher freight and insurance costs across global energy trade routes.

The sustained rise in energy costs is becoming increasingly relevant for India's steel sector, where fuel and logistics play a critical role in determining production economics. Higher crude oil prices directly influence diesel and bunker fuel costs, pushing up road freight, rail transportation, coastal shipping, and imported raw material logistics. Meanwhile, elevated LNG prices increase operating costs for gas-based DRI plants and other energy-intensive industrial processes.

As a result, the impact extends across the steel value chain from iron ore and coal transportation to pellet production, sponge iron manufacturing, steelmaking, and finished steel distribution. Rising freight and energy expenses can inflate the delivered cost of key raw materials and finished products, squeezing margins for market participants.

With global crude oil and LNG prices remaining well above the levels seen at the start of 2025, fuel-linked costs are emerging as a key variable for the steel industry. The continued elevation in energy prices could reshape production economics, logistics costs, and competitiveness across the steel value chain in the coming months.

Cost pressure begins at the raw material stage

The impact of higher fuel prices first became visible in mining and scrap processing activities.

Market participants estimate mining costs increased to around INR 450/t from nearly INR 350/t after industrial fuel prices rose from INR 88/litre to INR 110/ltr by approximately 25% in March. At the same time, the INR 8/litre increase in diesel prices raised iron ore transportation costs, increasing delivered ore costs for pellet plants and steelmakers.

In the scrap segment, LPG prices increased by around 15-20%, while oxygen prices rose by nearly 10%. According to market participants, scrap processing costs increased by around INR 200-300/t in the mid of March, prompting some processors to reduce operating rates and revise offer prices upward.

The tightening in domestic scrap availability was reflected in BigMint's HMS (80:20) Mandi Gobindgarh assessment, which increased by around INR 300/t to INR 35,500/t as on 20 March 2026.

Freight inflation raises cost of key steelmaking inputs

The rise in fuel prices has also pushed up international freight rates, increasing the landed cost of imported iron ore and coking coal.

Between February and June 2026, freight rates on major iron ore routes increased by 55-67%. Freight from Paradip to Qingdao rose by 57.7%, while the Port Hedland-Qingdao route increased by 67.4%.

A similar trend was witnessed in coking coal freight. Freight from Hay Point to Paradip increased by 49.3%, Richards Bay to Paradip by 49.6%, while East Kalimantan to Navlakhi recorded the sharpest increase of 89.8%.

The increase in ocean freight has raised raw material procurement costs for steelmakers, particularly coastal integrated mills dependent on imported coking coal and seaborne iron ore.

Metallic producers absorb rising costs

Higher mining, logistics and fuel expenses have gradually filtered through to pellet and sponge iron producers.

Market participants estimate pellet conversion costs at around INR 1,800-2,000/t for fuel-dependent operations. Sponge iron producers have also witnessed higher production costs due to rising fuel, transportation and raw material expenses.

The impact is particularly significant for gas-based sponge iron producers. According to industry consumption data, the steel and sponge iron sector consumed around 52 MMT of gas-based fuels in Apr'26, of which RLNG accounted for 51 MMT, representing nearly 98% of total consumption. The high dependence on RLNG exposes producers to fluctuations in gas and energy prices, making fuel costs a key component of sponge iron production economics.

However, weak steel demand has prevented producers from passing on these additional costs.

BigMint data shows Raipur sponge iron prices declined by around 8.7% between February and June 2026, falling to INR 24,520/t from INR 26,854/t despite rising operating costs. The decline suggests that producers have largely absorbed higher fuel, logistics and raw material costs through lower margins rather than through price increases.

Steelmakers face margin pressure

The disconnect between rising input costs and falling steel prices is most evident among secondary steelmakers.

Unlike integrated producers with captive resources, induction furnace-based steelmakers rely heavily on market-linked scrap, sponge iron, industrial gases and third-party logistics. Nearly every major input cost has moved higher over the last few months. Despite this, finished steel prices have weakened.

BigMint's benchmark BF-route rebar assessment declined to INR 55,000/t in Jun'26 from INR 60,250/t in Apr'26, while ex-Mumbai HRC eased to INR 58,350/t from INR 59,063/t during the same period. IF-route billet and rebar prices also recorded declines.

The trend indicates that steelmakers have so far been unable to recover higher production costs through finished steel prices due to subdued demand conditions.

Freight emerges as the key transmission channel

Market participants indicate that freight has become the primary channel through which fuel inflation is affecting steel prices.

Steel moves through multiple stages before reaching end-users, including transportation of iron ore, coal, pellets, sponge iron, billets and finished steel. Consequently, higher diesel and bunker fuel costs increase expenses at almost every stage of the value chain.

In addition, longer transit times and elevated ocean freight rates have increased inventory carrying costs and reduced export competitiveness, particularly in key destinations such as the Middle East.

Weak demand delays impact on steel prices

Historically, sustained increases in fuel and logistics costs eventually translate into higher steel prices. However, current market conditions have delayed this transmission.

Although costs have increased across mining, scrap processing, metallic production, freight and steelmaking, weak construction activity and cautious buying have prevented mills from implementing meaningful price increases.

As a result, much of the cost escalation has been absorbed across the value chain, compressing margins for miners, pellet producers, sponge iron manufacturers, secondary steelmakers and distributors.

Outlook

If geopolitical tensions continue

Continued conflict and supply chain disruptions could keep energy and freight costs elevated, maintaining upward pressure on raw material procurement, transportation, and steelmaking costs. Higher freight rates would further increase the landed cost of imported coking coal and other raw materials, while elevated fuel prices would continue to impact mining, scrap processing, sponge iron production, and steel distribution. With steel demand remaining subdued and mills facing limited ability to pass on higher costs, margin compression could intensify across the value chain. Secondary steelmakers, scrap processors, gas-based DRI producers, and distributors are likely to face the greatest pressure, making profitability increasingly challenging.

If geopolitical tensions ease

A de-escalation of conflicts and normalization of trade routes could help stabilize crude oil, LNG, and freight markets, reducing pressure on mining, scrap processing, metallic production, and steelmaking costs. Lower transportation and energy expenses would ease the cost of moving iron ore, coal, scrap, pellets, and finished steel, providing some relief to steelmakers and distributors. This could support margin recovery across the value chain, although a meaningful improvement in steel prices would still depend on a revival in domestic demand.