Russia's crude steel output falls to 15-year low as domestic demand slump deepens

...

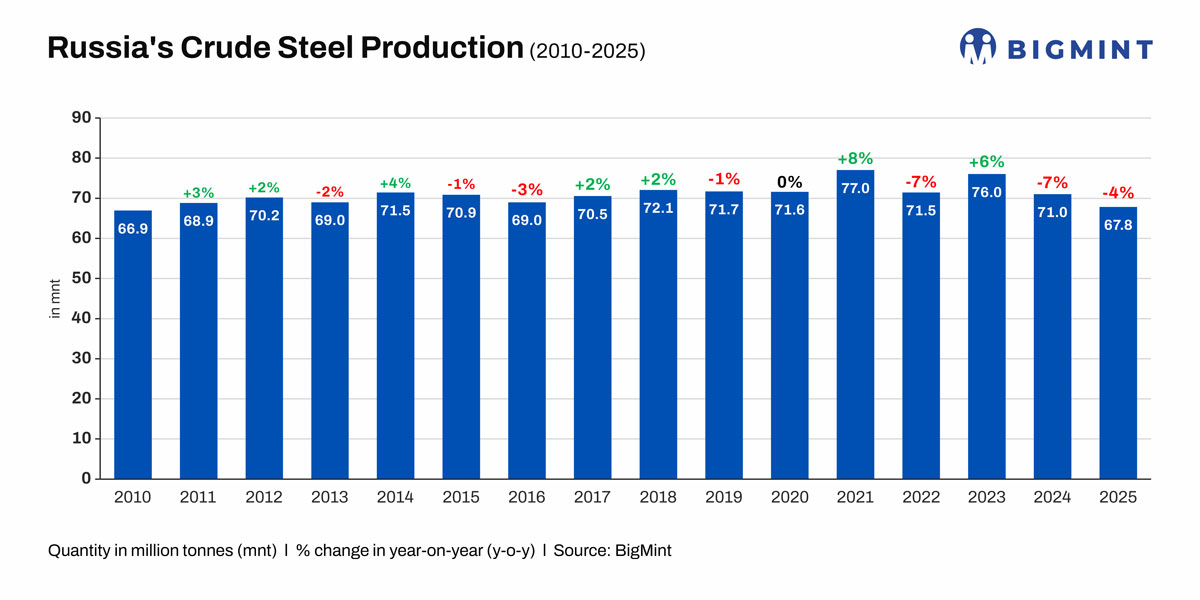

- Crude steel production falls to 67.8 mnt in 2025, the lowest since 2010

- Domestic steel consumption declines 14% in 2025 and a further 15% in Q1 2026

- High borrowing costs and sanctions continue to weigh on demand and profitability

Morning Brief: Russia's crude steel production fell to 67.8 million tonnes (mnt) in 2025, down 4% y-o-y from 71.0 mnt in 2024, according to BigMint data. The decline marks the country's lowest annual steel output in 15 years and extends a broader downturn that has persisted since production peaked at 77.0 mnt in 2021.

The latest decline suggests that Russia's steel industry is facing mounting pressure not only from sanctions and export restrictions but also from weakening domestic demand. While the sector managed a temporary recovery in 2023, when production rebounded to 76.0 mnt, output has since resumed its downward trajectory, indicating that earlier gains have proved difficult to sustain. Russia's post-sanctions recovery now appears to have run out of momentum, with the industry's brief rebound giving way to a renewed decline in both production and demand.

Domestic demand emerges as a key concern

Russia's steel sector has traditionally relied on demand from construction, machinery manufacturing, oil and gas, shipbuilding, agricultural equipment and railcar production. However, activity across several of these metal-intensive industries has weakened, reducing steel consumption and limiting production growth.

Industry reports indicate that domestic steel consumption fell by 14% in 2025 and declined by a further 15% y-o-y during Q1 2026. The deterioration comes despite continued support from defence-related manufacturing, highlighting the extent of weakness across the broader economy.

High borrowing costs have further compounded the challenges facing steelmakers. Elevated interest rates have weighed on construction activity and industrial investment, while increasing financing costs for producers already grappling with weaker demand.

Sanctions continue to reshape trade flows

The industry also continues to deal with the fallout from Western sanctions. Russian steelmakers lost access to several key export destinations following restrictions imposed by the European Union, the UK, the US, Canada and Japan. Although producers redirected shipments to Turkey, China and former Soviet states, export volumes have yet to fully recover to pre-sanctions levels.

Industry estimates suggest Russian steel exports fell from around 33.3 mnt in 2021 to 20.2 mnt in 2024, a decline of nearly 40%, highlighting the extent to which sanctions reshaped the country's steel trade flows. Exports recovered by around 20% in 2025 as producers expanded sales to alternative markets, although volumes remained below pre-sanctions levels.

A stronger rouble has also created additional headwinds for exporters. The appreciation of the Russian currency reduced the competitiveness of Russian steel in overseas markets and limited the benefits of higher export volumes for producers already facing sanctions-related trade restrictions.

The impact is increasingly visible in company financial performance. Several major steel producers reported lower revenue and profitability in 2025, prompting cost-cutting measures, lower capital expenditure and project delays. Some producers have also reduced capacity utilisation rates and scaled back investment plans as market conditions remain challenging.

Outlook

Russia's steel industry appears to have moved beyond the initial sanctions shock and into a more prolonged period of adjustment. The recovery seen in 2023 now appears temporary, with production falling in both 2024 and 2025 as domestic demand weakened and export opportunities remained constrained.

While exports have shown signs of recovery, the combination of weaker domestic demand, a stronger rouble and continued sanctions suggest that steelmakers may struggle to regain the production levels seen before 2022. Lower interest rates or a recovery in construction activity could provide support, but producers are likely to remain focused on cost controls and operational efficiency in the near term.

As a result, trends in domestic steel consumption, construction activity and export volumes will remain key indicators for assessing whether Russia's steel sector can stabilise after reaching its lowest production level in 15 years.