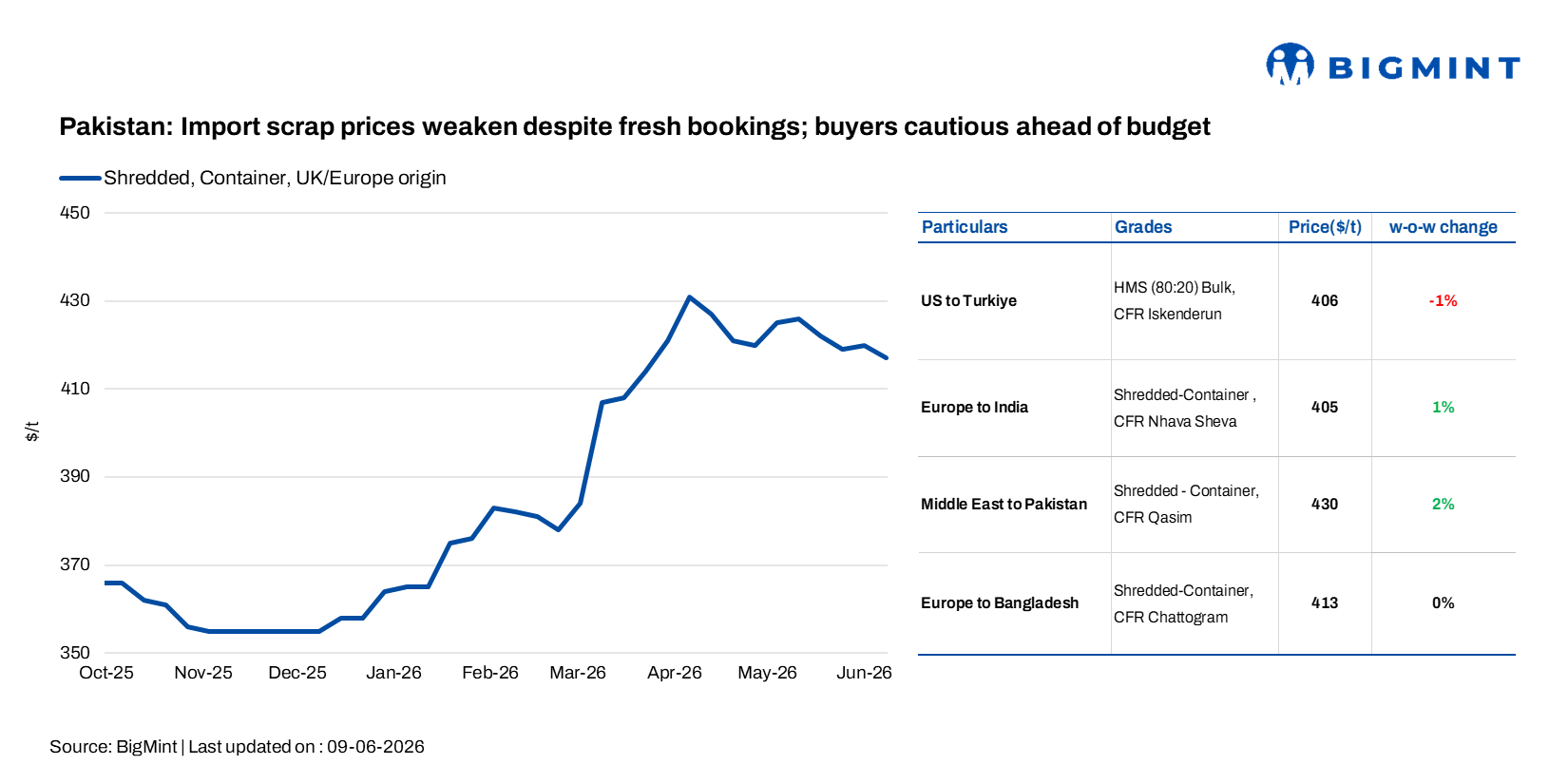

Pakistan: Import scrap prices weaken despite fresh bookings; buyers cautious ahead of budget

...

- Billet and rebar prices soften amid subdued demand

- Trading activity expected to improve after holidays

Pakistan's imported ferrous scrap market remained under pressure in the assessment week ended 9 June 2026 as buyers maintained a cautious stance ahead of the federal budget, despite several containerised scrap transactions being concluded.

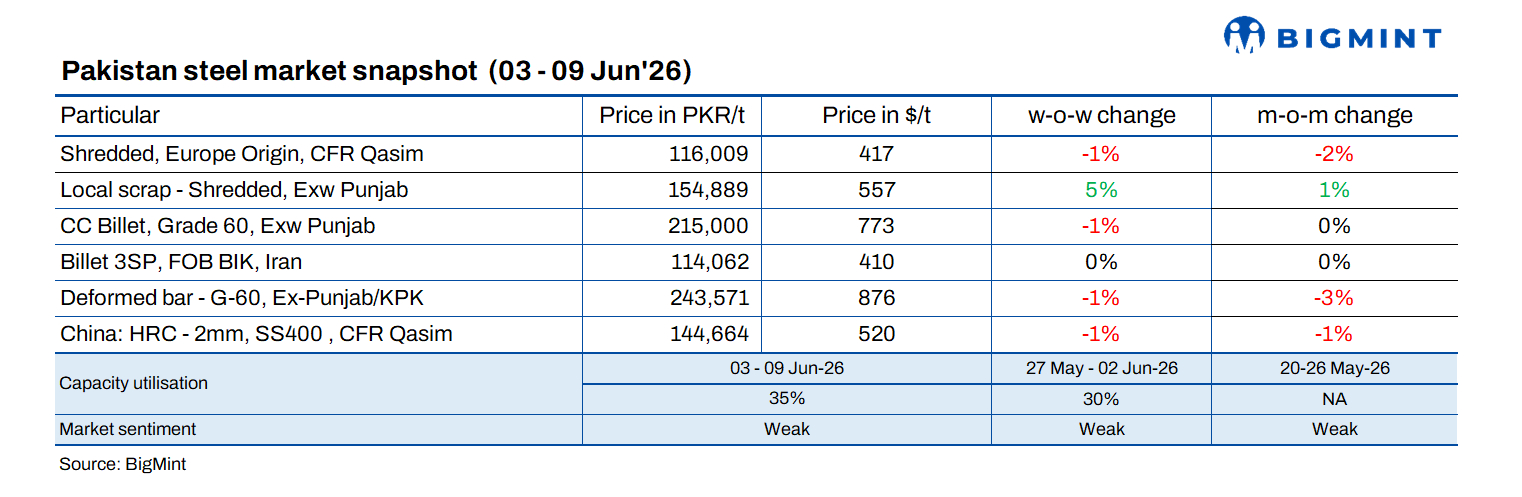

Trading activity in the domestic market remained limited, with mills operating at reduced utilisation rates and procurement largely restricted to immediate requirements. BigMint assessed Europe-origin shredded scrap at around $417/t CFR Qasim, inching down by around $3/t w-o-w.

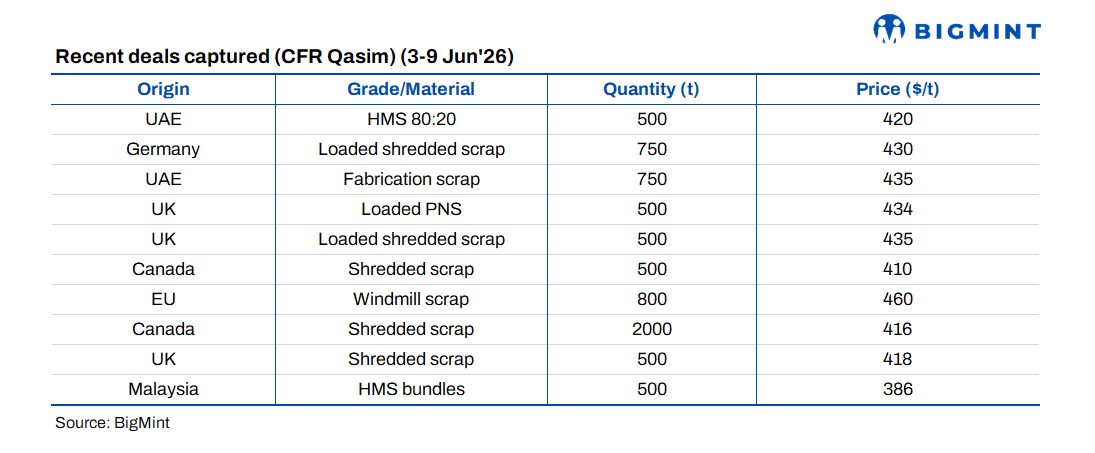

Imported shredded scrap offers from the UK and Europe were heard at $420-425/t CFR Port Qasim, and bids were down by around $5-6/t and stood at $412-415/t from previous indications. While offer levels remained relatively firm, concluded deals showed continued buyer resistance and negotiations at lower levels.

As per a local importer source, buyers remained active only for attractively priced cargoes, while higher-priced offers continued to face resistance. The source added that several transactions were concluded after extended negotiations as buyers sought discounts amid weak finished steel demand.

Domestic steel prices trend down

As per a Karachi-based steel mill source, finished steel demand remained sluggish, with buyers restricting purchases to immediate requirements amid uncertainty surrounding upcoming fiscal measures. Despite relatively stable raw material costs, including local scrap at PKR 155,000-160,000/t ($557-575/t), lower-quality scrap at PKR 144,000/t ($518/t), Bala at PKR 200,000-205,000/t ($719-737/t), and domestic billet at PKR 215,000-216,000/t ($773-776/t), mills largely maintained Grade 60 rebar prices at PKR 238,000-245,000/t ($856-881/t).

Sales and utilisation remain under pressure

Industry participants indicated that company sales were operating at around 40% of normal levels, while capacity utilisation remained at 35-40%, underscoring the weak demand environment and limited production activity across the market.

As per a Peshawar-based trader, market activity remained largely muted during the holiday period, with most buyers staying on the sidelines and only entering the market to meet immediate requirements. The trader said that very few spot deals were concluded, as participants preferred to wait for clearer market direction before committing to fresh purchases.

Outlook

Market participants expect buying interest in imported scrap to improve as businesses resume operations following the holiday period. However, uncertainty surrounding the upcoming federal budget and continued weakness in finished steel demand are expected to keep procurement largely need-based.

As per a Karachi-based steel mill source, inquiries have started to increase as customers return to the market, but buyers remain reluctant to build inventories. The source noted that most participants are waiting for greater clarity on fiscal measures and their potential impact on construction activity before taking larger positions.

Market sentiment remains cautious, with traders closely monitoring international scrap price movements and developments in the domestic steel sector. While trading activity is expected to improve, any significant increase in import bookings will depend on stronger steel offtake and improved confidence among end-users.