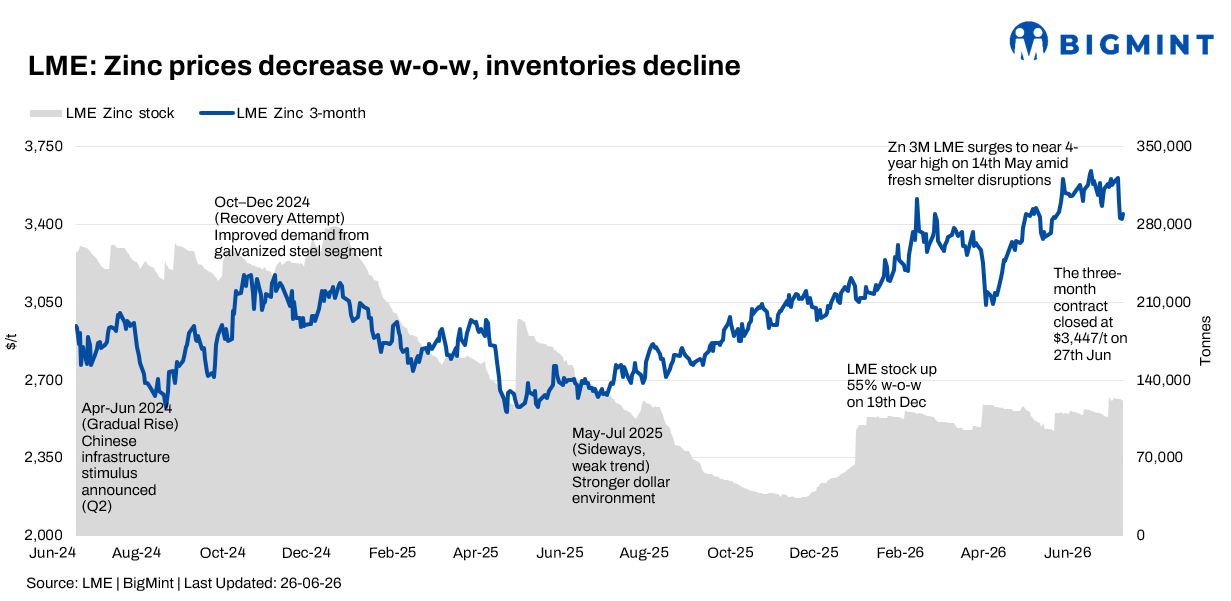

LME zinc declines w-o-w despite lower inventories

...

- LME zinc falls 3.5% w-o-w despite continued inventory drawdown

- Prices rebound on Friday after sharp mid-week correction

London Metal Exchange (LME) zinc prices declined during the week ended 26 June 2026, as broad-based weakness across the base metals complex and cautious sentiment surrounding Chinese industrial demand outweighed the supportive impact of declining exchange inventories. Although warehouse stocks continued to fall throughout the week, profit-booking after recent gains and subdued buying interest kept prices under pressure. However, bargain buying emerged towards the week-end, allowing prices to recover from their weekly lows.

On a w-o-w basis, LME zinc cash settlement prices fell 3.5% to $3,460/t on 26 June from $3,584.5/t on 19 June. Despite the weekly decline, zinc continued to trade above the key $3,400/t level, indicating that underlying physical demand and tighter exchange inventories continued to provide support.

Price trends

LME zinc cash settlement prices opened the week at $3,612.5/t on 22 June, the highest level of the reporting period, supported by positive carryover sentiment from the previous week.

Thereafter, prices corrected sharply to $3,503/t on 23 June and further to $3,437/t on 24 June, as investors booked profits amid weaker sentiment across industrial metals. The decline moderated on 25 June, with prices easing marginally to $3,432/t before recovering to $3,460/t on 26 June as buyers returned at lower levels.

The three-month contract broadly tracked the cash market, slipping from $3,612/t on 22 June to $3,500/t on 23 June, before easing to $3,428/t on 24 June and $3,425/t on 25 June. The contract rebounded to $3,447/t by 26 June, reflecting improved buying interest towards the close of the week.

The narrow cash-to-three-month spread continued to suggest balanced near-term market fundamentals despite increased price volatility.

Inventory analysis

LME zinc inventories continued to decline throughout the reporting week, offering underlying support to market fundamentals.

Stocks eased from 123,775 t on 19 June to 123,450 t on 22 June, before falling further to 123,150 t on 23 June and 122,825 t on 24 June. Inventories declined to 122,400 t on 25 June and further to 121,300 t on 26 June.

Overall, exchange inventories fell by 2,475 t w-o-w, reflecting sustained warehouse outflows. While the continued decline highlighted healthy physical offtake, it was insufficient to offset broader risk-off sentiment in the financial markets.

Market updates

Market sentiment remained cautious during the week as investors focused on weaker macroeconomic signals and uncertainty surrounding China's industrial demand outlook. The sharp correction in prices during the middle of the week largely reflected profit-booking following the previous week's gains rather than any significant deterioration in physical market fundamentals.

Meanwhile, steady consumption from the galvanising sector and continued inventory withdrawals suggested that underlying demand remained resilient. The recovery in prices on Friday indicated renewed buying interest at lower levels, helping zinc finish the week above the important $3,450/t mark despite the overall weekly decline.

Outlook

BigMint expects LME zinc prices to remain broadly rangebound in the coming week, with lower exchange inventories likely to provide downside support while cautious macroeconomic sentiment continues to cap upside.

Immediate support is expected around $3,400-3,430/t, while resistance is seen in the $3,500-3,560/t range. Market participants will closely monitor Chinese demand indicators, LME inventory movements, and broader trends across the base metals complex for further price direction.