LME: Lead prices decline 2.8% w-o-w as cautious sentiment offsets lower inventories

...

- LME lead extends weekly losses despite continued decline in exchange inventories

- Gradual inventory drawdown fails to revive buying interest

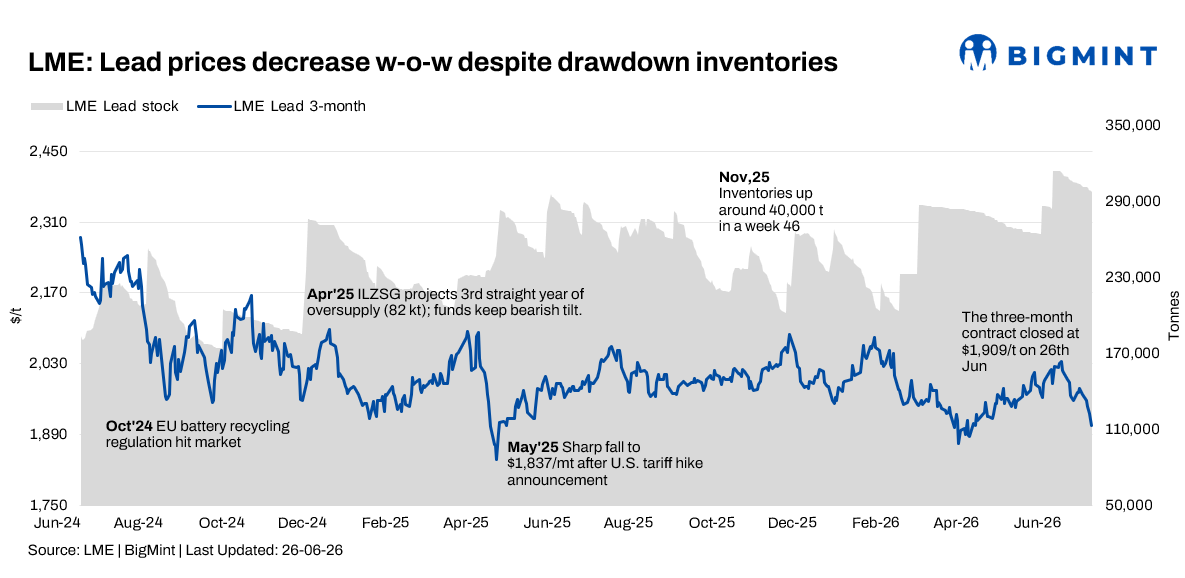

London Metal Exchange (LME) lead prices declined during the week ended 26 June 2026, as cautious sentiment across the base metals complex continued to weigh on investor confidence despite another week of falling exchange inventories. While warehouse stocks registered consistent outflows, the inventory decline was insufficient to trigger fresh buying, with participants remaining focused on uncertain macroeconomic conditions and subdued downstream demand. As a result, lead prices posted a second consecutive week of losses.

On a w-o-w basis, LME lead cash settlement prices declined by 2.8% to $1,880/t on 26 June from $1,935/t on 19 June. Although the persistent reduction in inventories highlighted stable physical offtake, cautious market sentiment continued to dominate price direction throughout the reporting week.

Price trends

LME lead cash settlement prices opened the week at $1,928.5/t on 22 June before extending losses over the following sessions.

Prices eased to $1,910/t on 23 June, followed by $1,896/t on 24 June as sellers remained active across the base metals complex. The market remained under pressure on 25 June, with prices edging down to $1,894/t, before declining further to $1,880/t on 26 June, the lowest level of the week.

The three-month contract mirrored movements in the cash market. Prices slipped from $1,957/t on 22 June to $1,945/t on 23 June, before falling to $1,931/t on 24 June, $1,920/t on 25 June, and $1,909/t at the close of trading on 26 June.

The gradual correction across both contracts reflected sustained investor caution rather than any abrupt deterioration in physical supply-demand fundamentals.

Inventory analysis

LME lead inventories continued their downward trajectory throughout the reporting week, indicating ongoing warehouse outflows.

Stocks eased marginally from 301,950 t on 19 June to 301,850 t on 22 June, before declining to 300,650 t on 23 June. Inventories fell further to 299,650 t on 24 June, 298,525 t on 25 June, and 297,450 t on 26 June.

Overall, LME lead inventories declined by 4,500 t w-o-w. While the steady reduction in visible stocks reflected healthy physical consumption, the pace of inventory withdrawals was not sufficient to outweigh cautious investor positioning and weaker sentiment across industrial metals.

Market updates

Market sentiment remained cautious during the reporting week despite supportive inventory fundamentals. Participants largely maintained hand-to-mouth procurement strategies, with limited evidence of aggressive restocking. Broader uncertainty surrounding global manufacturing activity and demand prospects continued to keep speculative buying subdued.

The continued decline in LME inventories nevertheless suggests that underlying physical demand remains relatively stable, particularly from the battery manufacturing sector. However, the disconnect between physical fundamentals and financial market sentiment resulted in prices remaining under pressure throughout the week.