India's non-coking coal imports fall to 4-year low in Jan-May'26 even as power demand reaches record high

...

- Surge in renewables output helps offset coal demand from power sector

- Rising seaborne coal prices, freight costs erode import competitiveness

- CIL's pithead stocks remain elevated despite weaker production in Jan-May

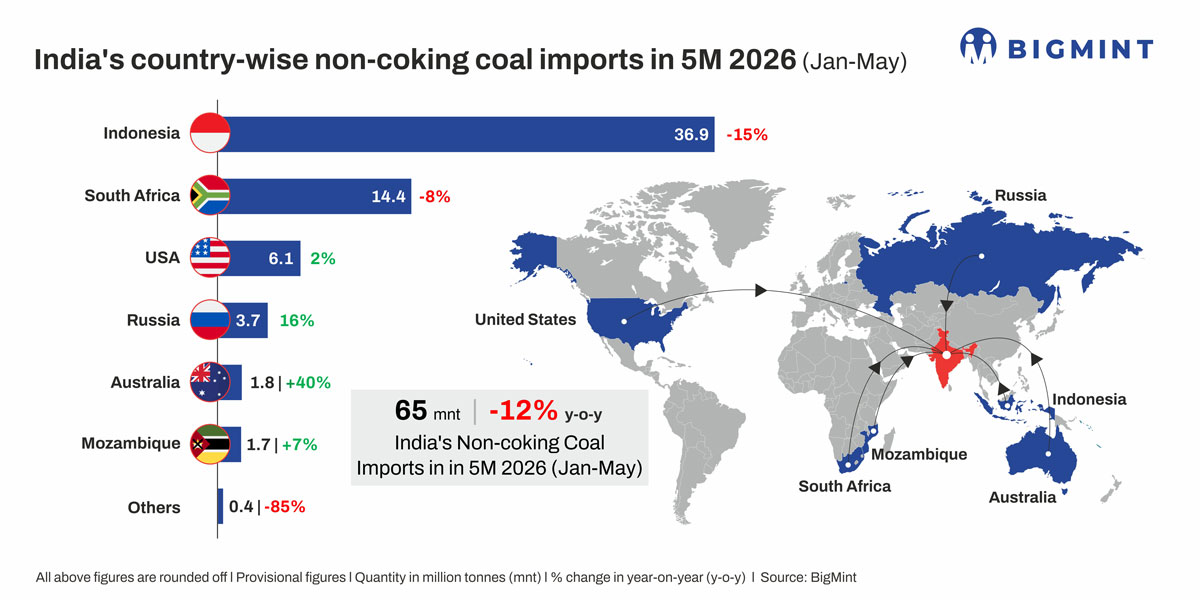

Morning Brief: India's non-coking coal imports fell 12% y-o-y to 65 million tonnes (mnt) during January-May 2026, marking the lowest volume for the period since 2022. The decline comes despite India's peak power demand reaching a record 270.82 GW on 21 May amid widespread heatwaves, highlighting a growing disconnect between electricity demand growth and thermal coal import requirements.

During previous periods of strong summer demand, utilities typically increased imports to supplement domestic supplies. In CY26, however, rising renewable generation helped meet the increase in power demand, while ample domestic coal supply and unfavourable import economics and elevated freight costs further weakened the attractiveness of imported cargoes.

The downtrend deepened during April-May, when imports fell 18% y-o-y, following the outbreak of the US-Iran conflict in March.

Factors influencing India's non-coking coal imports

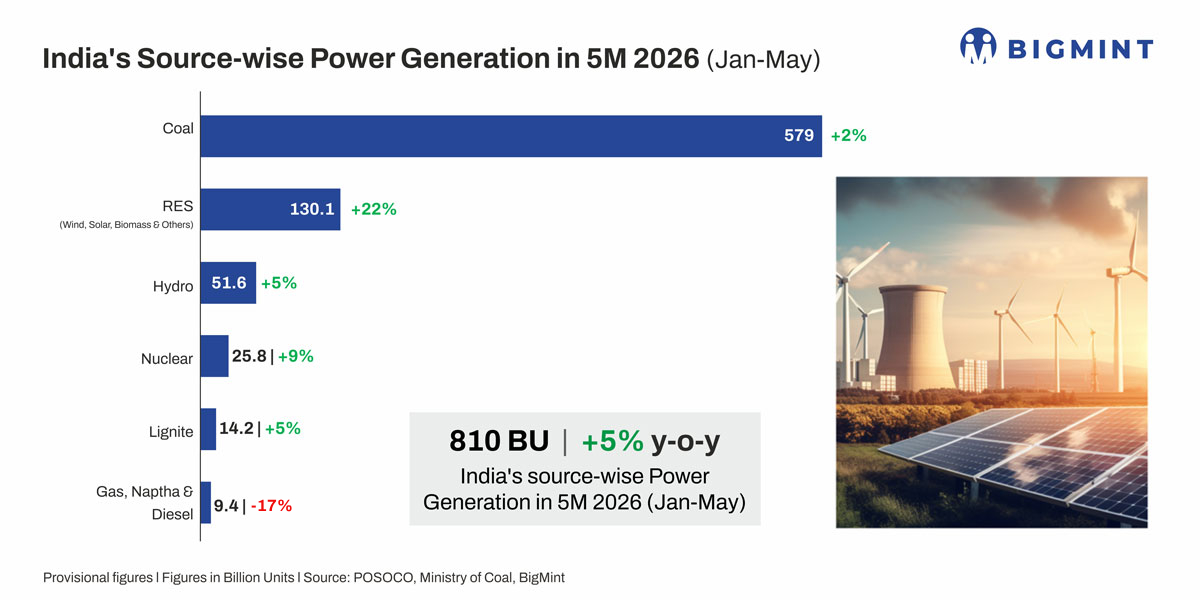

Renewables absorb power demand growth: India's electricity consumption increased 4% y-o-y to 742 billion units (BU) during January-May 2026 as above-normal temperatures boosted cooling demand across the country.

However, while total power generation rose 5% y-o-y to 810 BU over the same period, coal-fired output increased by a mere 2% y-o-y to 579 BU. In comparison, renewable generation grew at a much faster pace of 22% y-o-y to 130 BU. Of the additional 37.5 BU generated during January-May, renewables contributed around 23 BU, accounting for 62% of incremental generation.

Coal-based generation, meanwhile, increased by only 11.2 BU, or around 30% of incremental output. This significantly reduced the need for additional coal consumption and, by extension, import demand despite record electricity consumption.

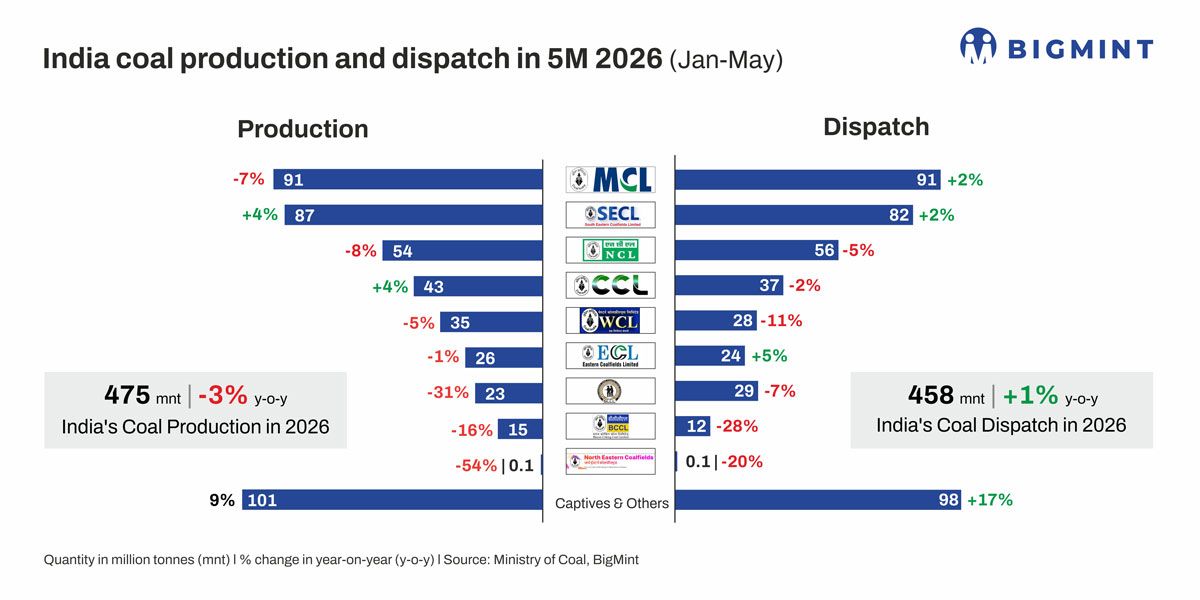

Domestic coal supply remains strong: Strong domestic supply and inventories enabled most consumers to avoid imports. Although Coal India's production declined 3% y-o-y to 351 mnt during January-May, dispatches remained largely unchanged y-o-y at 330 mnt against 331 mnt a year earlier. Notably, dispatches rose 4% y-o-y in May to 68 mnt despite an 11% drop in production, helping utilities manage fuel requirements during the peak summer season.

In a recent interview, Chairman and Managing Director B. Sairam said that Coal India began FY'27 with pithead inventories of around 130 mnt, equivalent to roughly 17% of its FY'26 production of 768 mnt. The company has since reduced stockpiles to around 112 mnt and aims to gradually reduce inventories further to a more optimal level of about 70 mnt or 10% of its annual output.

Coal inventories at power plants declined from 59.3 mnt in March to 49.2 mnt in May. However, the drawdown largely reflected stronger consumption rather than supply stress. Utilities remained comfortable operating with lower inventory levels as domestic dispatches continued uninterrupted.

Portside non-coking coal stocks also remained approximately 5% higher y-o-y at roughly 14 mnt during March-May 2026 against 13.3 mnt in the year-ago period.

Import economics remain unfavourable: The decline in imports was further reinforced by rising seaborne coal prices and freight costs.

South African RB3 (4800 NAR) coal averaged $92/t CNF Gangavaram during January-May, up 24% from $74/t a year earlier. Indonesian 4200 GAR coal averaged $71/t CNF Kandla, increasing 11% y-o-y compared with $64.2/t during the corresponding period of CY'25.

The increase in delivered costs reflected both higher FOB coal prices and rising freight expenses. Additional shipping costs linked to disruptions in Middle Eastern trade routes following the US-Iran conflict contributed to the increase.

Portside prices also climbed up sharply. For example, South African RB2 (5500 NAR) crossed INR 11,000/t in March at Paradip, while throughout C'25, prices had ranged between INR 8,000-9,000/t. This pushed buyers such as sponge iron producers to increasingly source domestic coal rather than imports. Imports from South Africa declined 8% y-o-y to 14 mnt during January-May despite a 7% uptick in sponge iron production in India.

Indonesian imports fall sharply amid supply tightening: Imports from Indonesia, India's largest non-coking coal supplier, declined 15% y-o-y during January-May. This coincided with tightening Indonesian export availability. Indonesian non-coking coal exports fell 7% y-o-y to 108 mnt during January-April amid uncertainty surrounding mining work plans, production approvals, and domestic market obligation requirements.

With domestic coal readily available and import prices rising, Indian buyers showed limited willingness to absorb higher Indonesian costs. As a result, Indonesian shipments to India fell 31% y-o-y in May.

US coal supported by cement sector demand: US thermal coal imports bucked the broader trend, rising 2% y-o-y to 6 mnt during January-May. The increase was driven primarily by cement manufacturers seeking alternatives to expensive petcoke. High-calorific-value Northern Appalachian (NAPP) coal remained cost-competitive for cement production despite weakness across the wider import market.

Outlook

BigMint expects India's non-coking coal imports to remain under pressure through the remainder of CY'26 despite continued growth in electricity demand and sponge iron and cement production. Even if electricity demand continues to grow at 6-8% annually, import demand may struggle to return to the levels seen in CY'23 and CY'24 given that renewable generation is increasing, domestic coal supply remains ample, and import costs are still elevated.

The re-opening of Strait of Homuz and lower crude oil prices may reduce freight costs but tight Indonesian supply and uncertainty regarding export regulations will continue to keep prices elevated. Weak sponge iron pricing during the monsoon months may also limit producers' appetite for higher-priced South African imports.

Additionally, with petcoke prices softening, US thermal coal seems to be losing its competitiveness. Therefore, shipments from the US may also slow down.

Overall, stable domestic dispatches, rising renewables penetration, and elevated seaborne coal costs are expected to continue limiting import requirements over the coming quarter.