India's iron ore and pellet imports rise 50% y-o-y in Jan-May'26 - BigMint data

...

- Iron ore and pellet imports reach around 4.8 mnt in 5M CY'26

- Lump imports surge as Iran disruption affects pellet shipments

- Iron ore imports edge up despite growth in domestic production

Morning Brief:India's imports of iron ore and pellets reached around 4.8 million tonnes (mnt) in January-May 2026, an increase of nearly 50% y-o-y compared with 3.2 mnt in the year-ago period, as domestic major steel producers ramped up shipments from Brazil, South Africa and the Middle East amid surging steel production.

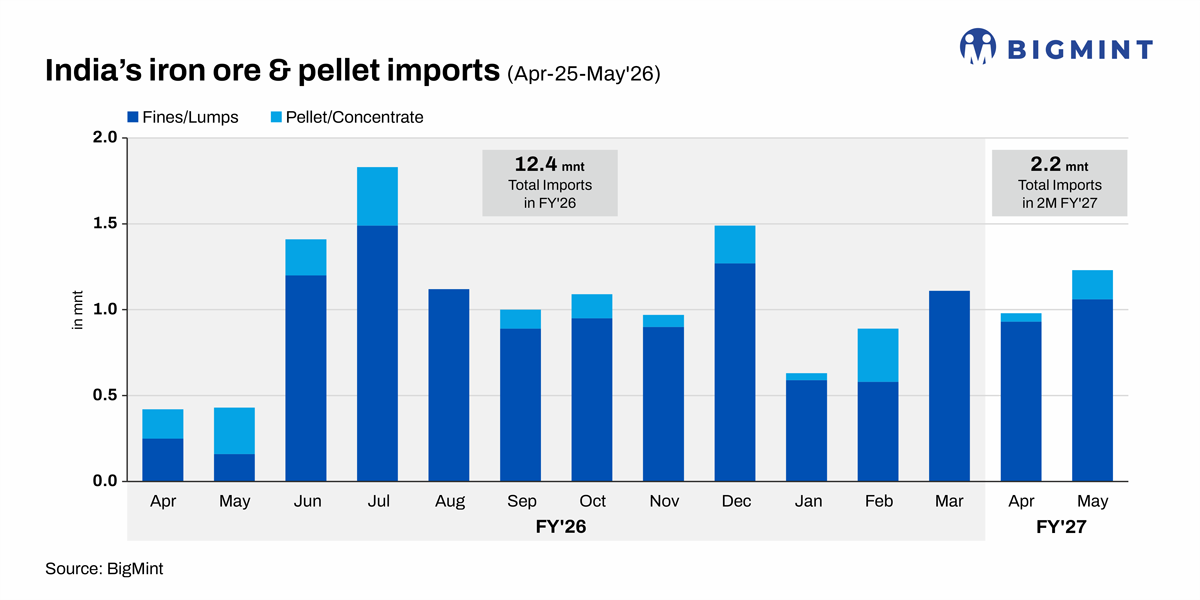

In May, imports were recorded at 1.24mnt as against 0.98 mnt in April of which 1.06 mntwas iron ore fines and lumps and remaining 0.17 mnt were pellets. Although BigMint recorded pellet shipments discharged at Kandla port from Porto do Au, Brazil, the cargoes were reportedly intended for reloading and subsequent shipment to Bahrain after the easing of geopolitical tensions in the region, as per sources. Therefore, the cargoes were not meant for consumption by Indian plants.

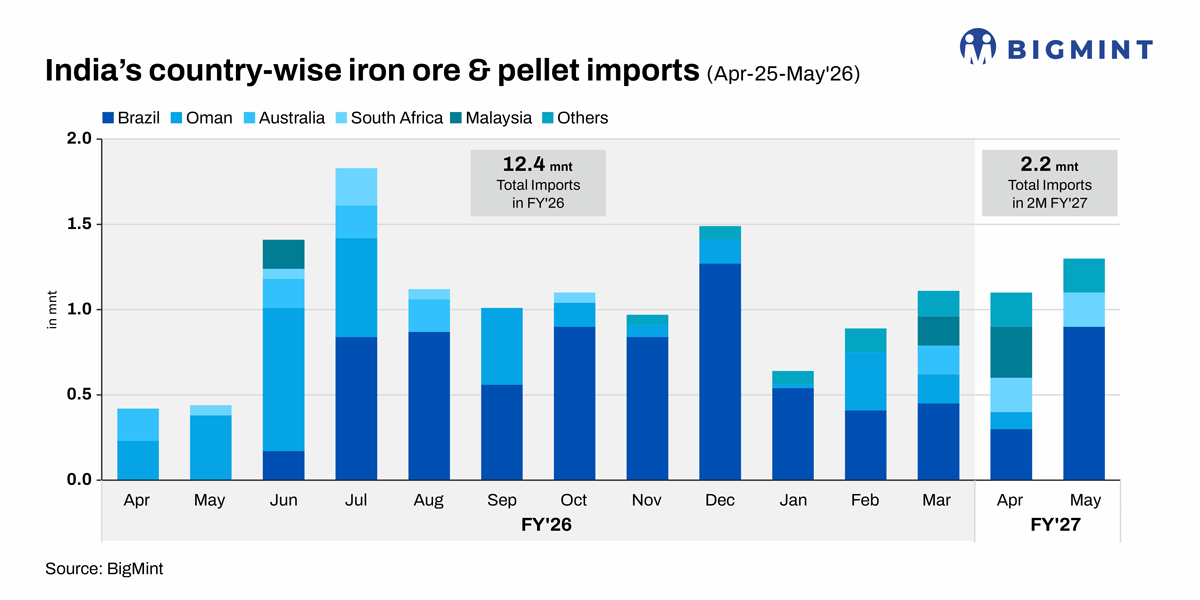

In May, the major importer was JSW Steel at 0.72 mnt while the largest supplier was Brazil at 0.72 mnt followed by South Africa at 0.18 mnt and Norway (0.16 mnt). JSW's crude steel output surged in May post restart of a BF at Dolvi and ramp-up of operations at JSW Vijaynagar Metallics Ltd. This called for higher imports of ore in May.

Iron ore imports in January-May were assessed at 4.28 mnt while pellet imports dropped sharply, to just over 400,000 t, amid the Middle East conflict and shipping disruptions.

JSW Group was the major buyer of imported ore accounting for 85% of total imports during the period. On the other hand, Brazil was the top exporter accounting for 56% of total shipments during January-May.

Iron ore imports rose to 12.35 mnt in FY'26, a seven-year high, driven by rising domestic steel demand, surging demand for high-grade and low-impurity ore, as well as supply constraints in key mining regions.

Factors driving iron ore imports in Jan-May'26

Surging demand for high-grade ore: BigMint data shows that domestic production of Fe +65% iron ore dwindled to 11% of total production in FY26 compared with 20% in FY'17. Iron ore imported from Brazil is largely high grade, Fe 64-65%, with very low silica content. Indian ore has generally a very high silica-alumina content. Thus, imported ore offers quality benefits at a time when the major steelmakers are aiming to optimise processes and attain energy efficiency benchmarks.

Favourable import economics: Pellet imports were disrupted due to the Middle East conflict and shipping bottlenecks through Oman. Meanwhile, the landed price of South African iron ore lump turned competitive compared to domestic pellets. For example, pellet prices were high along the west coast which led the western India-based sponge iron producers to opt for South African lumps (Fe 64-65%) which were cheaper by around INR 500/t against prevailing pellet prices at INR 12,200/t DAP, as per BigMint assessment.

Similarly, domestic sourcing costlier with the PSU miners such as NMDC raising prices by INR 450/t in April to INR 4,500/t for Fe 64% (excluding all taxes), which increased the overall landed cost for mills increasing the viability of imports.

Tight availability in Karnataka:About 0.7 mnt of Brazilian ore was imported at Krishnapatnam port by JSW during January-May. As per reports, multiple miners in Karnataka reported disturbance in logistics and dispatch-related issues, hindering domestic iron ore movement and affecting procurement in Karnataka and nearby regions.

For instance, dispatches and auction volumes of a leading PSU miner in the state were affected due to regulatory and other issues which greatly impacted availability. Limited availability of high-grade ore and absence of regular auctions by the major miners strengthened the premium on high-grade fines in Karnataka and raised the demand for imports.

Geopolitical risks, increased global supply: Domestic importers sought to book cargoes to stock up ore in apprehension of further hindrances in raw material procurement due to rising fuel and freight prices, as well as shipping disruptions due to the ongoing Iran conflict.

On the other hand, improved seaborne supply and softer Chinese demand enhanced cargo availability and pricing flexibility. Major global miners such as Vale are increasingly targeting India as the next growth market. Sustained downtrend in Chinese steel production may turn the attention more towards India in the coming years.

Outlook

India's iron ore mining capacity increased by over 10% in FY'26 to 521 mnt, as per BigMint data. Fresh ECs accorded this fiscal will expectedly lead to higher production. Moreover, regulations aimed at fast-tracking mine operationalisation are expected to deliver higher volumes.

However, these measures may not readily lead to lowering import volumes. In January-April, domestic iron ore production rose by 15% y-o-y; yet imports shot up sharply due to the lack of high-grade material in different regions, logistical bottlenecks and favourable import economics. Disruptions during the monsoon season and logistical problems usually lead to higher imports.

Therefore, high mining costs in the form of premiums and taxes, location and logistical advantages, as well as the demand for low-impurity ore at competitive prices will drive imports by producers such as JSW.