India's crude steel production growth expected to slow in FY'27 but consumption may recover faster y-o-y

...

- Steel demand from infrastructure, construction to accelerate in FY'27

- Rising energy cost, weak monsoon pose risks to manufacturing growth

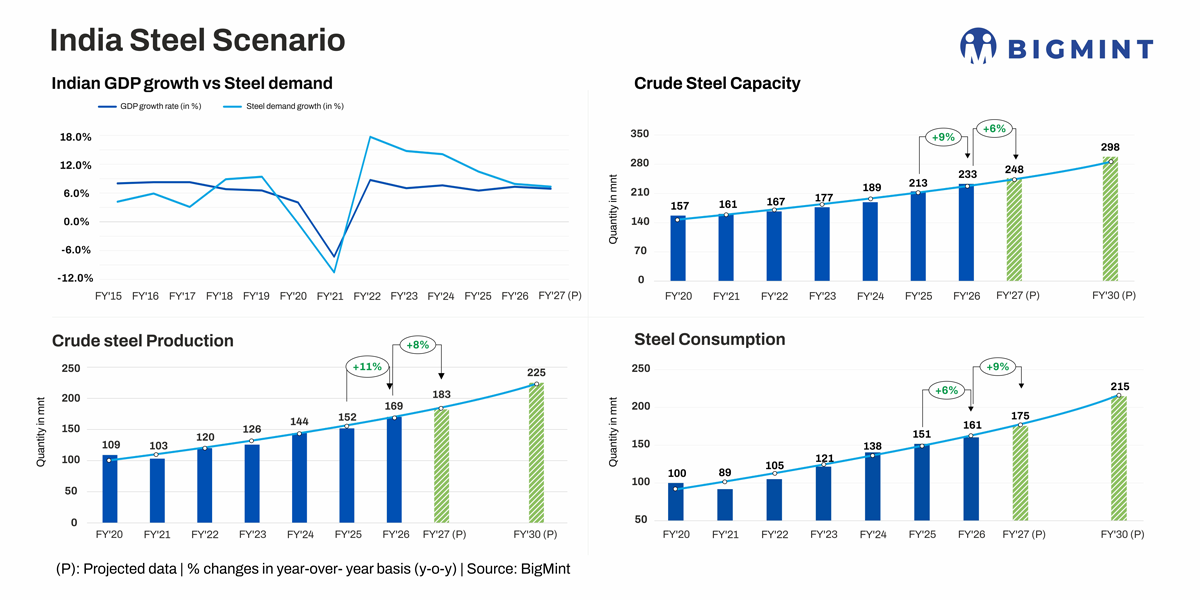

Data Deep Dive:India's crude steel production is set to rise 8% y-o-y to 183 million tonnes (mnt) in FY'27 from 169 mnt in FY'26, according to BigMint's projection. While output growth remains robust by global standards, it marks a moderation from the 11% increase recorded in FY'26 as capacity additions slow and economic growth softens, driven by macroeconomic headwinds and the US-Iran war. The Reserve Bank of India (RBI) has projected gross domestic product (GDP) growth of 6.9% in FY'27 compared with 7.6% in FY'26.

Despite the softer macroeconomic backdrop, BigMint expects steel demand to recover in FY'27, with consumption projected to increase by 9% y-o-y to 175 mnt, faster than FY'26's 6% y-o-y. The recovery is expected to be supported by improved project execution, continued public sector investment, and resilient demand from construction-related sectors.

Historically, steel demand in India has grown faster than GDP, reflecting the country's investment-led development model, where infrastructure construction and manufacturing expansion are more steel-intensive than the broader, services-driven economy. This relationship weakened in FY'26 as a prolonged monsoon and slower execution of capital expenditure projects weighed on steel consumption growth. However, FY'27 is set to see a return to this trend as infrastructure spending translates into stronger steel consumption.

Production growth to slow along with capacity expansion

BigMint expects slower capacity additions in FY'27 to temper India's crude steel production. Installed crude steelmaking capacity increased by 13% y-o-y in FY'25 and 9% in FY'26, taking total capacity to 233 mnt. However, we see capacity growth moderating sharply to around 6% y-o-y to 248 mnt in FY'27.

The Indian steel industry has faced sustained margin pressure over the past two years as steel prices across most product categories declined steadily, reaching five-year lows in Q3FY'26. Against this backdrop, the moderation in capacity expansion plans may reflect a more cautious approach among steelmakers.

However, Indian steel prices rebounded sharply in Q4FY'26, supported by accelerated infrastructure spending toward the fiscal year-end and supply-side concerns stemming from the Middle East conflict. Although raw material costs also increased during the period, the rise in finished steel prices outpaced input cost inflation, leading to an improvement in margins. The recovery in profitability is expected to support production growth and encourage higher capacity utilisation in FY'27.

Capacity utilisation has improved steadily over the past two years and is estimated to increase to 75% in FY'27, close to FY'24's peak level of 76%.

Scrap usage to accelerate

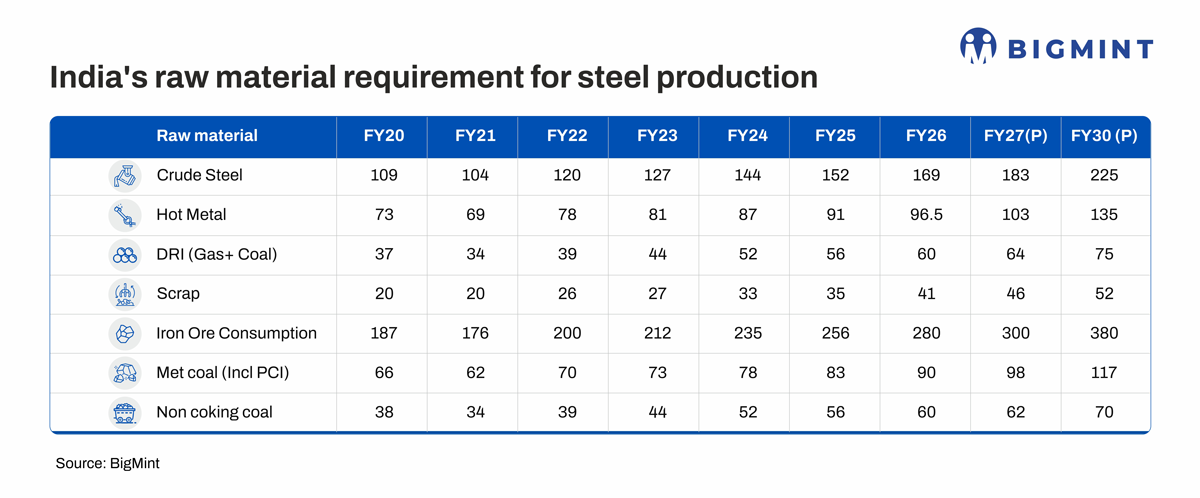

BigMintexpects scraptoaccount for a larger share of incremental steel production, while growth in direct reduced iron (DRI) moderates.

Scrap is projected to remain the fastest-growing metallic, with consumption rising 12% y-o-y to 46 mnt in FY'27 following a 17% increase in FY'26. Growing scrap generation and increasing emphasis on decarbonisation will continue to support the uptrend.

We see hot metal consumption rising 7% y-o-y to 103 mnt in FY'27, accelerating slightly from 6% growth in FY'26, reflecting continued capacity additions by integrated steelmakers.

In contrast, DRI consumption is projected to riseat a slower pace of 7% y-o-y to 64 mntin FY'27, compared with 8% growth in FY'26. However, it remainsthe second-largest metallic feedstock due to its cost competitiveness relativeto scrap and its widespread use in the secondary steel sector.

Demand recovery expected after FY'26 slowdown

India's steel demand growth has gradually moderated since FY'22. After recording double-digit growth through much of FY'22-FY'25, steel consumption grew 6% in FY'26. However, FY'27 is set to mark a recovery with 9% growth.

The government's INR 12.2 lakh crore capital expenditure allocation will remain critical in sustaining steel demand. Public sector spending is expected to offset a softer private investment environment, as manufacturers contend with uncertainties arising from the Middle East conflict, elevated energy costs, inflationary pressures, supply chain disruptions, and trade-related risks. Rural demand also faces uncertainty due to concerns over monsoon performance, increasing the importance of government-led investment in sustaining steel consumption growth.

We believe an acceleration in infrastructure activity will emerge as the primary driver of steel demand growth in FY'27, balancing out the impact of softer manufacturing sector expansion.

Infrastructure, construction continue to anchor demand

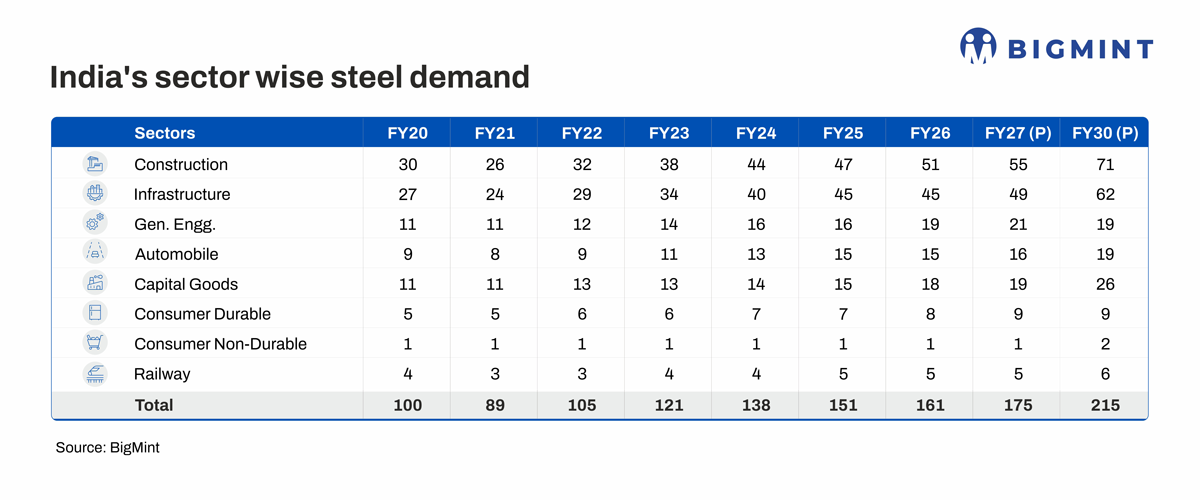

Our projections show that the construction and infrastructure sectors will account for 8 mnt of incremental steel demand in FY'27 compared to 4 mnt in FY'26.

Construction will add 4 mnt of steel demand, reflecting stable growth since FY'25 but moderation since FY'22-FY'24's annual additions of around 6 mnt. Major cement producers have guided for 7-8% demand growth in FY'27, supported by infrastructure spending and urban housing demand. Given the strong correlation between cement and steel consumption in construction projects, the outlook points to healthy growth in steel demand from the sector.

Infrastructure-linked steel demand is projected to increase by around 4 mnt in FY'27. While this marks a recovery from FY'26, when demand from the sector remained largely flat, the pace of growth remains below the annual additions of 5-6 mnt recorded during the post-pandemic phase of FY'22-25.

The key driver is likely to be improved project execution following a weak FY'26. While central government capex growth is budgeted at a lower 9% y-o-y compared with the 25-35% increases seen during FY'22-FY'24, spending remains elevated in absolute terms at INR 12.2 lakh crore. Moreover, a large pipeline of projects across railways, roads, urban infrastructure, power transmission, renewable energy, and housing remains under construction. For example, for the PM Awas Yojana, the housing target for FY'27 is three times greater than last year.

Manufacturing-led steel demand may slow down amid headwinds

Collectively, steel demand is set to increase by 5 mnt from manufacturing-linked sectors, including general engineering, capital goods, automobiles, consumer durables, and consumer non-durables. In FY'26, steel demand from manufacturing increased by 7 mnt.

The y-o-y slowdown is linked to the general engineering and capital goods sectors, where growth is set to moderate following two years of exceptionally strong expansion. However, the decline is expected to be offset by improving demand from the automobile sector, which saw a robust FY'26 due to the government's GST cuts.

Continued implementation of production-linked incentive (PLI) schemes, import substitution initiatives, supply chain diversification from China, and sustained public-sector capital expenditure are expected to support manufacturing activity. However, the growth is likely to remain concentrated in investment-linked sectors supported by government spending, including power, railways, defence, and infrastructure.

Rising petroleum and natural gas costs, supply chain disruptions, softer rural consumption, and global trade uncertainties are likely to limit broader manufacturing expansion.Similarly, inflationary pressures and the possibility of monetary policy tighteningalso pose risks.

Outlook

With steel demand projected to grow faster than GDP, India is likely to remain the world's fastest-growing major steel market. However, risks remain, especially given the expectations of weaker GDP growth.

While the domestic market is expected to absorb most of the incremental production, the industry's ability to sustain capacity expansion will increasingly depend on the pace of infrastructure development and investment-led growth. As is typical of emerging economies, government spending on transport, housing, power, and industrial infrastructure will remain the principal driver of steel consumption and a key enabler of future capacity additions.

Elevated energy prices, a rising import bill and a depreciating currency, fiscal pressures arising from geopolitical tensions, an uneven monsoon, and slower global trade could weigh on public capital expenditure and limit infrastructure execution. That apart, rising steel imports in the opening months of FY'27 and the prospect of weaker export opportunities, particularly amid tightening regulatory requirements in the EU, could reintroduce supply-side pressures later in the year.

If demand fails torecover, India could be headed for another year where production growth outpaces consumption. Consequently, steelmakers could face renewed pressure on margins.