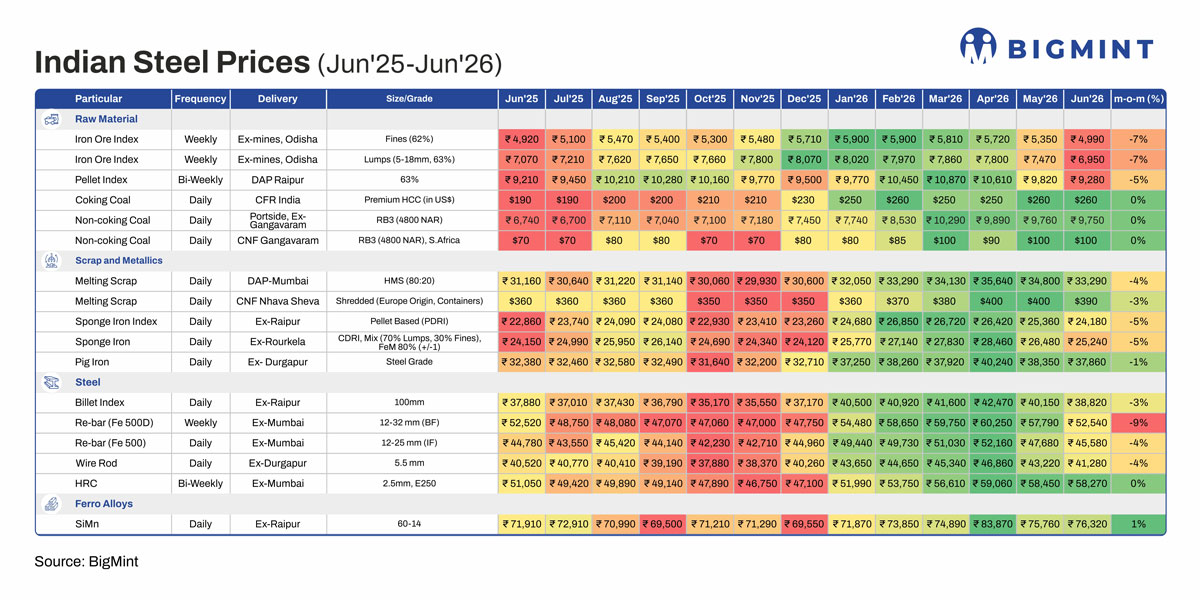

Indian steel and raw material prices extend correction in Jun'26 as demand weakens further

...

- Long steel prices fall sharply on weak construction demand and inventory build-up

- Iron ore, pellets and manganese ore soften while coking coal remains firm

- Manufacturing activity continues to support HRC despite moderating growth

Morning Brief: Domestic steel prices extended their correction in June as weakening construction demand outweighed easing raw material costs across the steel value chain. Rising inventories, thinner order books and slower project execution entering the monsoon quarter weighed on long steel products, while manufacturing activity and export-oriented downstream sectors continued to provide relatively better support to flat steel demand. HRC remained broadly stable despite elevated import arrivals, whereas blast furnace (BF)-route rebar corrected sharply amid weaker bookings and inventory build-up. Improving logistics and lower freight costs offered limited support as domestic demand remained the dominant driver of market sentiment.

Price movements across the steel value chain

Iron ore & pellets: BigMint's Odisha iron ore fines and lump ore indices declined 7% m-o-m each in June, while pellet prices fell 5%. OMC's latest auction saw fines bids remain broadly stable, while lump ore bids softened by around INR 150/t. NMDC had earlier raised prices following stronger global prices in May, but easing domestic steel demand weighed on ore and pellet markets during June.

Coking & non-coking coal: Premium hard coking coal prices remained unchanged during June, while domestic portside and imported non-coking coal prices were largely stable, leaving coal as the only major raw material that did not participate in the broader correction.

Melting scrap: Domestic melting scrap prices declined 4% m-o-m, while imported shredded scrap fell 3% as lower procurement by secondary steelmakers and softer freight costs weighed on buying interest.

Sponge iron, pig iron & billet: Sponge iron prices fell 5% m-o-m, reflecting lower billet production and weaker procurement by induction furnace mills. Billet prices declined 3% as slower finished steel demand reduced buying by re-rollers. Pig iron proved comparatively resilient, easing just 1%, supported by stronger export demand.

Rebar: Long steel remained the weakest-performing segment during June. BF-route rebar prices declined 9% m-o-m, while IF-route rebar fell 4%. BF mills reduced list prices by INR 1,000-4,000/t from early May levels as inventories at primary mills increased around 35% month-on-month amid weak fresh bookings. Industry sources said most project-linked orders had already been executed, leaving mills with thinner order books and lower backlog visibility entering the monsoon quarter.

HRC: HRC prices remained broadly stable despite May bulk import arrivals reaching around 423,925 t, up 22% m-o-m and 52% y-o-y. Market participants indicated that a significant share of these imports was consumed under the Advance Authorisation Scheme by domestic pipe and tube manufacturers before being exported as finished products, limiting pressure on domestic prices. Manufacturing activity also remained in expansion territory despite moderating from May, with the HSBC India Manufacturing PMI at 54.2, continuing to support downstream flat steel demand.

Silico manganese: Domestic silico manganese prices rose 1% m-o-m after sharp corrections in previous months. Meanwhile, weaker overseas demand prompted major miners to reduce July manganese ore offers, while MOIL lowered domestic manganese ore prices from 1 June, improving the raw material outlook for ferro alloy producers.

Outlook

Seasonally weaker construction activity is expected to keep long steel prices under pressure through the monsoon quarter, while manufacturing demand should continue providing relatively better support to flat steel. Weak domestic demand has already encouraged higher billet and pig iron exports, although tighter EU safeguard quotas may limit opportunities in Europe, increasing the importance of alternative markets such as the Middle East. Meanwhile, lower iron ore and manganese ore prices have eased some input costs, but the 40 paise/unit increase in industrial electricity tariffs in Chhattisgarh from 1 July is expected to raise billet production costs by around INR 300-400/t and increase costs for ferro alloy producers. Demand conditions are therefore expected to remain the principal driver of domestic steel prices in the near term.