India: Coated flat steel market softens amid sluggish demand; buyers await July mill price revision

...

- Coated steel prices fall across major markets

- High inventories curb fresh procurement activity

Indian coated flat steel prices declined by INR 100-1,000/t w-o-w during the assessment week, weighed down by sluggish buying activity and ample inventory availability across the supply chain. Demand from key consuming sectors remained subdued, with buyers continuing to restrict purchases to immediate requirements amid cautious market sentiment. Market participants largely refrained from fresh bookings as they awaited July mill price revisions, anticipating greater clarity on the pricing outlook. Consequently, tradeable prices softened across most regions during the week.

Price update

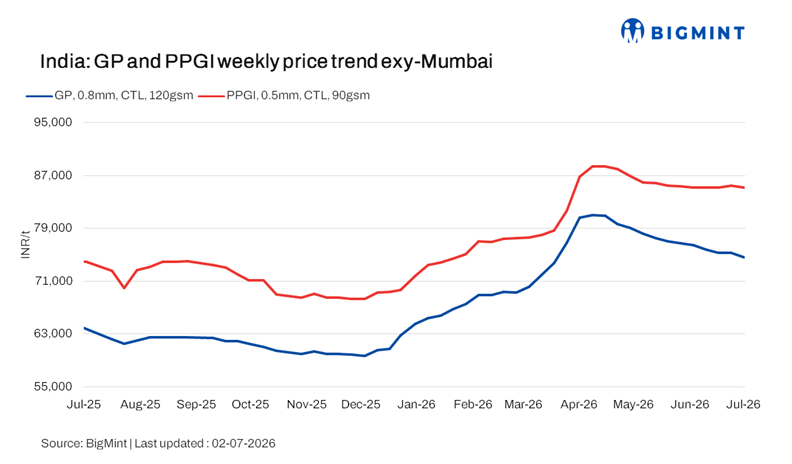

BigMint's benchmark assessment for Mumbai GP coil (0.8mm/CTL, 120 GSM, IS 277) declined by INR 700/t w-o-w to INR 74,600/t. The correction was driven by subdued buying activity, ample inventory availability across the supply chain, and cautious procurement by buyers awaiting July mill price revisions. Weak spot demand continued to weigh on tradeable prices.

BigMint's benchmark assessment for Mumbai PPGI (0.5mm/CTL, 90 GSM, IS 14246) decreased by INR 300/t w-o-w to INR 85,200/t. Prices came under pressure amid slow order inflows and limited spot buying, with buyers largely restricting purchases to immediate requirements while awaiting clarity on mill pricing for July.

BigMint's benchmark assessment for Mumbai BGL (0.5mm/CTL, 1220mm, AZ150) fell by INR 200/t w-o-w to INR 89,500/t. Competitive offers, cautious buyer sentiment, and muted booking activity continued to weigh on prices, while adequate material availability in the market further pressured transaction levels.

Raw material prices

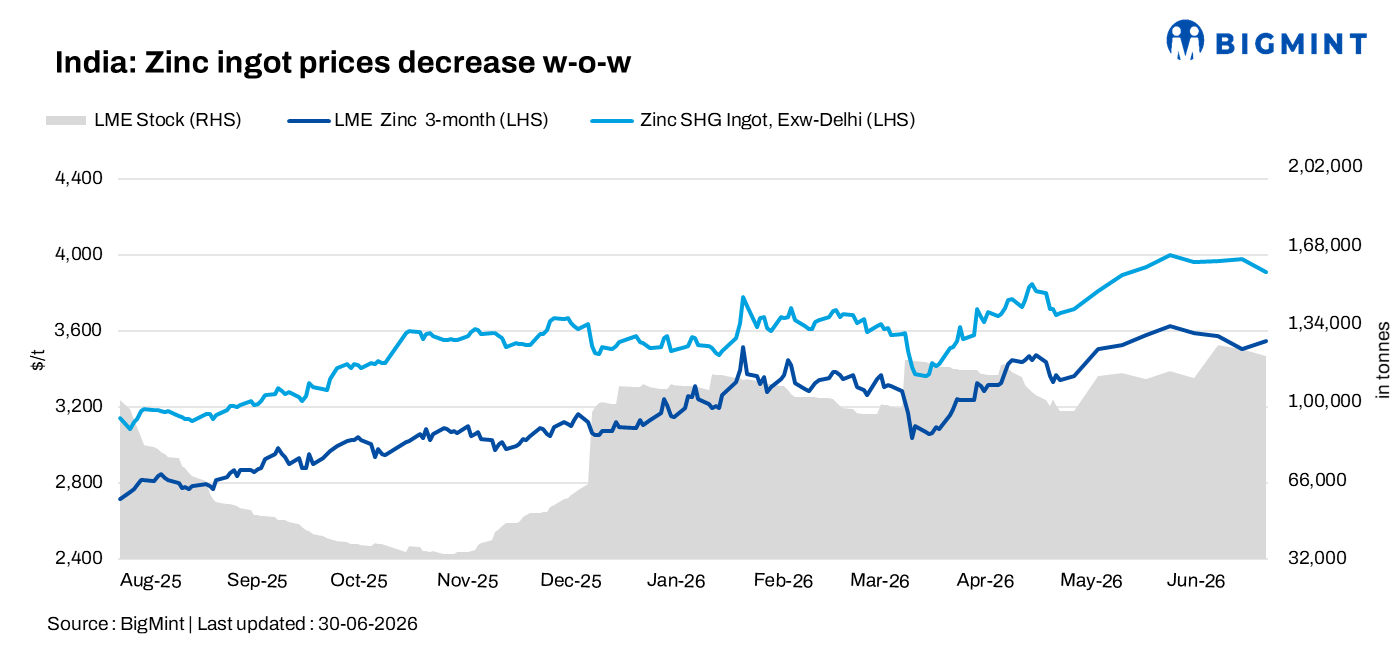

India's zinc ingot (99.995%) prices declined by INR 4,000/t w-o-w to INR 370,000/t ex-Delhi on 30 June 2026, according to BigMint's assessment. The correction largely reflected Hindustan Zinc Ltd's (HZL) sharp reduction in benchmark prices, which weighed on domestic sentiment despite continued tightness in imported material availability. Downstream demand from galvanisers and alloy manufacturers remained largely need-based, with buyers refraining from building inventories amid the ongoing monsoon season and adequate spot availability.

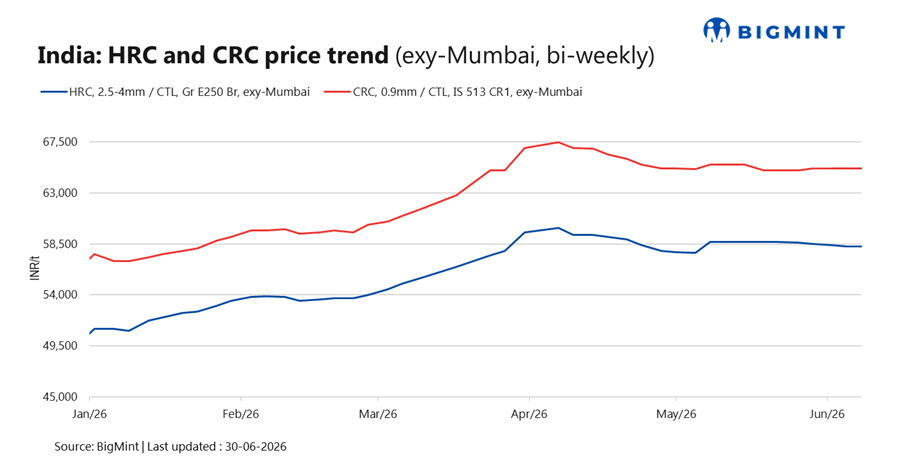

Meanwhile, BigMint's bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) in Mumbai remained stable w-o-w at INR 58,200/t ($615/t) as of 30 June 2026, reflecting balanced market conditions despite subdued spot buying.

Likewise, the benchmark assessment for CRC (IS513, Grade O, 0.9 mm/CTL) held steady at INR 65,200/t ($689/t). All assessments are ex-Mumbai and exclusive of 18% GST.

Market updates

The Indian coated flat steel market remained under pressure during the assessment period, with prices continuing to trend lower amid persistently weak demand. Trading activity across coated products remained subdued, with buyers limiting procurement to immediate requirements.

Market participants informed BigMint that they have largely deferred fresh bookings as they await July mill price revisions, expecting greater clarity on the near-term pricing direction. Sources indicated that distributors and stockists are carrying adequate to high inventory levels, reducing the need for additional procurement.

Supply availability remained comfortable across all coated flat steel products, with market participants reporting no supply-side constraints. However, material movement continued to be slow due to weak downstream demand, resulting in limited spot transactions and increasing competitive pressure on market offers.

Overall, market sentiment remained cautious, with buyers continuing to adopt a wait-and-watch approach while monitoring mill pricing decisions and demand recovery.

Outlook

The coated flat steel market is expected to remain under pressure in the near term as weak downstream consumption and elevated inventories continue to limit buying interest. The upcoming July mill price revisions will be a key trigger for market direction, with participants closely watching whether producers adjust prices to align with prevailing spot market conditions. Unless procurement activity improves following the price revisions or demand recovers after the monsoon season, spot prices are likely to remain range-bound to weak, with distributors expected to maintain cautious inventory positions and continue need-based purchasing.