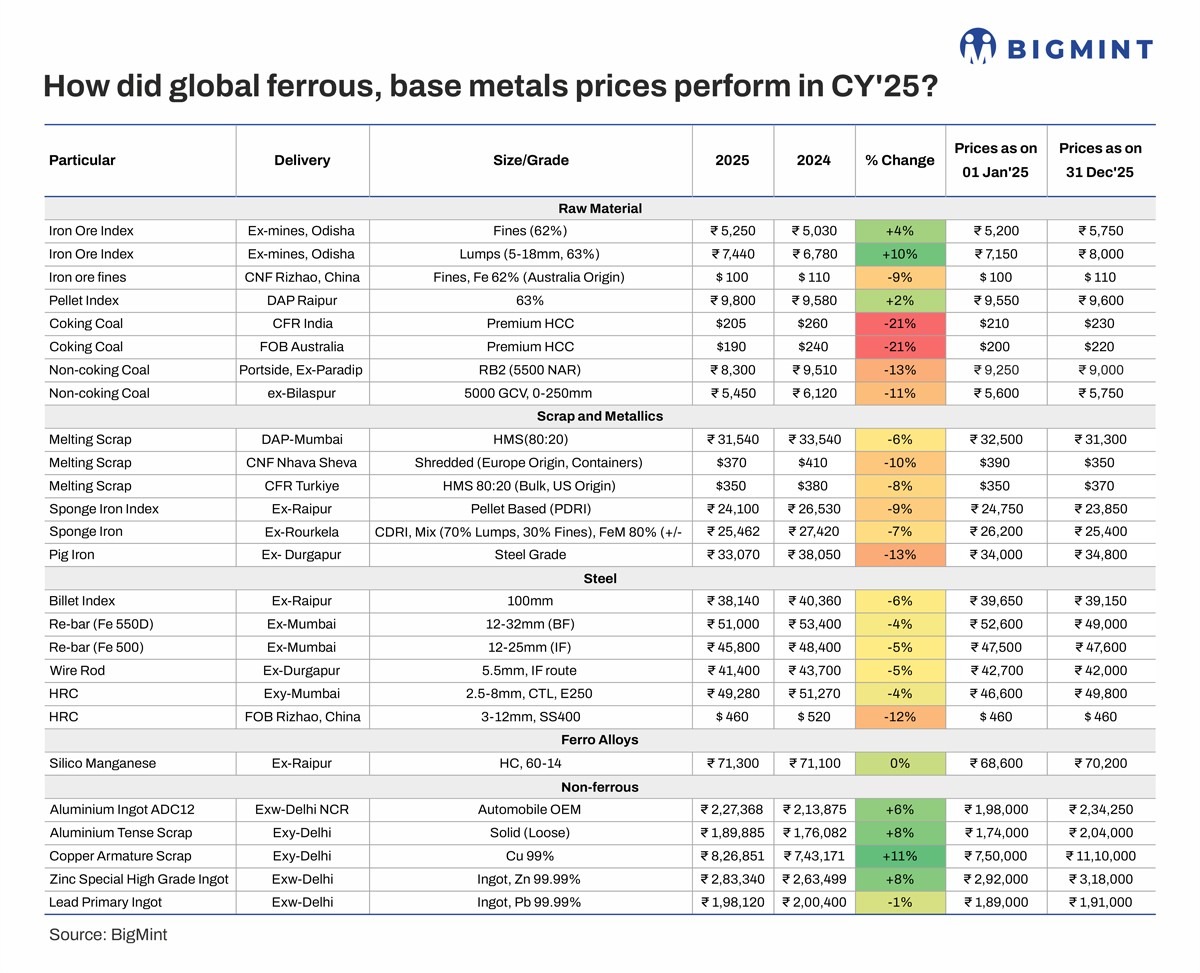

Indian ferrous prices weaken in CY'25; base metals trade higher

...

- Indian iron ore prices buck downtrend on production shortfalls

- Australian coking coal plunges 21% y-o-y as demand weakens

- Copper scrap up 11% y-o-y on supply disruptions

Morning Brief: Indian steel and raw material prices moved lower in CY'25 on a yearly average basis, pressured by a prolonged monsoon, which limited construction activity for a large part of the year. The resultant demand slump, coupled with weak global pricing, cautious buyer sentiment, and robust production growth (in comparison to consumption) pushed several commodities to five-year lows during CY'25. Notably, India's crude steel production increased 10% to 164 million tonnes (mnt), while consumption rose by a slower 8% to 160 mnt.

Iron ore was the only exception, with fines, lumps, and pellets moving higher. This was due to a severe supply shortage in H2CY'25, while rising crude steel production throughout the year ensured steady iron ore demand.

On the other hand, domestic base metals prices averaged higher y-o-y across all commodities except lead. Tight supply and LME gains supported a price uptick in domestic aluminium, copper, and zinc markets.

Meanwhile, key factors that influenced global pricing last year included (1) mounting steel exports from China due to the protracted property sector crisis (though India was relatively insulated due to the 12% safeguard duty on flat steel imports); (2) a complex geopolitical environmental due to the US's imposition of multiple tariffs; and (3) reduced crude steel production in China, expected to reach a six-year low.

Ferrous

Iron ore

Fines: A shortage in high-grade iron ore fines allowed prices to rise by 4% y-o-y in CY'25 even as downstream segments such as sponge iron and finished steel weakened. India's iron ore production increased by a mere 4% to 294 mnt despite a 10% rise in crude steel production. The non-operationalisation of auctioned mines was a key factor limiting production growth in iron ore.

Lumps: The share of lumps in India's iron ore production fell to 27% in CY'25 from 30% in CY'24, again indicating limited availability, as overall iron ore production increased. This, along with rapid sponge iron CDRI production, contributed to a sharp 10% growth in lumps prices.

Pellets: BigMint's pellet index, PELLEX, increased as well, though by a lower 2%. While rising iron ore prices lifted pellet production costs, weak sponge iron billet, and rebar pricing capped gains.

Chinese iron ore fines: Notably, the rise in Indian iron ore prices contrasts with a 9% drop in global benchmark prices of iron ore imported into China. Reduced crude steel production, weak steel mill margins, subdued domestic demand, and apprehensions regarding US-China trade tensions pushed Chinese buyers to negotiate lower prices. The operationalisation of Guinea's Simandou mines are expected to keep supply loose in CY'26, leading to continued bearishness.

Coal

Coking coal: India's imported coking coal prices fell a massive 21% y-o-y, tracking a drop of the same magnitude in benchmark Australian FOB prices. Key factors weighing on global coking coal prices were overproduction in China, especially in the first half of the year; the decrease in production enthusiasm among Chinese steelmakers; and the weak steel market in India, which made mills resistant to accepting elevated offers.

South African non-coking coal: Indian portside prices of South African RB2 non-coking coal fell by 13% y-o-y, as demand weakened. Indian sponge iron producers shifted to more affordable domestic alternatives to manage costs amid weak steel pricing. Ample portside stocks and domestic coal supply also moderated demand.

Domestic thermal coal: Indian thermal coal (5000 GCV) prices fell 11% y-o-y, as supply remained comfortable, limiting restocking urgency. Additionally, an extended monsoon meant cooler weather and lower power consumption. CIL's coal production fell by 2% y-o-y to 767 mnt, while offtake also declined 2%, both likely driven by subdued demand, adequate coal stocks at power plants, stagnant electricity demand, increased operational efficiency at thermal units, selective capacity utilisation, and logistical hurdles.

Ferro alloys

Silico manganese: Indian prices of high-carbon silico manganese (60-14) were stable y-o-y. While lower steel prices exerted downward pressure, manganese ore prices remained firm y-o-y, providing cost support. To illustrate, MOIL's prices increased by 2% y-o-y to an average of INR 15,560/t. Additionally, although prices of imported ore fell y-o-y, they inched higher m-o-m since July.

Scrap and metallics

Domestic melting scrap: Indian melting scrap (HMS 80:20) prices fell 6%, again due to subdued finished steel offtake during the prolonged monsoon, which forced mills to reduce their capacity utilisation. Mills also turned to sponge iron, a cheaper alternative, to mitigate cost pressures. Notably, domestic scrap prices fell to nearly a five-year low in November. Additionally, in CY'25, domestic scrap generation increased by 8% to 32 mnt, suggesting strong supply growth.

Imported scrap: With Indian domestic scrap being more competitive and alternatives such as sponge iron sufficiently available, the need to import scrap reduced, especially given the fall in finished steel prices. Therefore, imported European shredded prices into India fell 10% y-o-y. India's scrap imports edged up by a minor 2% y-o-y to 9.8 mnt. The price gap between imports and domestic material was said to be around INR 1,500-2,000/tonne (t) in the latter half of the year.

Turkish imported scrap: Turkish US-origin HMS 80:20 slipped by 8% y-o-y, with consistently weak rebar demand and thin profit margins keeping mills cautious on raw material procurement. High freight costs during H2 and the availability of competitively priced Chinese billets also dampened demand, leading mills to maintaining lean scrap inventories.

Sponge iron: BigMint's sponge iron (PDRI) index, ex-Raipur, slid 9% y-o-y. CDRI mix prices, ex-Rourkela, fell by a lower 7% y-o-y. Sponge iron consumption softened, rolling mills and re-rollers faced weak finished steel demand due to a slowdown in construction and infrastructure activity, which was compounded by monsoon-driven disruptions and limited liquidity among secondary mills. Export opportunities also slowed due to low overseas inquiries and freight challenges, leaving producers largely dependent on the domestic market. Consequently, rising inventories and tepid demand pushed sponge iron prices to five-year lows in November. Lower thermal coal prices also eroded cost support.

Pig iron: Steel-grade pig iron prices fell a steep 13% y-o-y due to a persistent gap between supply and demand. During April-September H1FY'26, for example, while production was stable y-o-y, consumption fell by 3% y-o-y. Again, weak finished steel offtake led to the decrease in pig iron consumption, mirroring conditions seen in other segments of the steel value chain.

Steel

Billets: BigMint's billet index, tracking ex-Raipur prices, fell 6% y-o-y in CY'25. Prices hit nearly a five-year low in October, with re-rollers scaling down material intake due to muted finished steel sales.

Rebars: Weak construction and infrastructure momentum in India, especially during the monsoon, pulled down BF rebar prices by 4% y-o-y in CY'25, while the IF variant was hit harder, with a 5% fall in prices. Both traded at a five-year low by November. While the first quarter witnessed buoyant sales, trade activity moderated as the year progressed. Stocks accumulated at yards, with average IF rebar inventory holding periods at 12-15 days, forcing mills to offer deep discounts to liquidate material. A much-expected price uptick around the festive period failed to materialise, and overall, market participants cited tight liquidity and uncertainty around price direction as key factors curtailing demand.

HRC: Indian hot-rolled coil (HRC) prices fell 4% y-o-y, as demand in the trade channel remained insufficient. While HRC production is estimated to have increased by 9.5% to 59 mnt, consumption rose by softer 5.4% to 58.4 mnt.

Chinese HRC export offers: CY'25 brought on a 12% drop in Chinese HRC export offers, FOB Rizhao. With a barrage of trade safeguard measures, such as anti-dumping duties, being imposed on Chinese flat steel exports, naturally, demand shrank for Chinese HRCs. Additionally, domestic demand weakened due to subdued manufacturing activity and the continuing real estate crisis. Consequently, HRC exports had to reduce offers significantly to attract more and more buyers.

Non-ferrous

Aluminium ADC12 ingots: Indian ADC12 aluminium alloy ingot prices (automobile OEM-grade) climbed higher by 6% y-o-y in CY'25. Limited supply, as well as firm prices, of domestic and imported scrap pushed up production costs for secondary alloy producers.

Additionally, ADC12 imports remained limited (falling by 51% y-o-y in 10MCY'25), partly due to BIS-related compliance issues, keeping the domestic market dependent on local material. From September, ingot demand from the automotive sector improved, backed by higher OEM production schedules, festive-season buying, and a GST-led sentiment boost.

Aluminium tense scrap: Tight supply and strong downstream demand pushed up aluminium tense scrap prices, exy-Delhi, by 8% y-o-y. India's reduced scrap imports from the US following the tariff imposition forced buyers to rely more on the domestic market, creating persistent supply constraints.

Mid-year, rising demand for ADC12 alloy from the automotive and die-casting sectors further supported prices. Moreover, towards the year-end, imported scrap prices rose in line with higher LME aluminium prices amid global supply concerns, while imports slowed due to exchange-rate pressures and holiday-related disruptions. LME aluminium prices were up 8% y-o-y, averaging $2,640/t in CY'25.

Copper armature scrap: An 8% rise in LME three-month futures (to a yearly average of $9,970/t) fuelled a robust 11% hike in Indian copper armature prices. Global copper prices surged to multi-year highs throughout CY'25, as shutdowns at key mines in H2 raised concerns of a supply deficit, while the US import tariffs also prompted rapid destocking during May-July. Additionally, India's Quality Control Order (QCO) on copper cathodes implemented in 2025 sharply reduced cathode inflows (down 14% y-o-y in 10MCY'25), which prompted increased reliance on scrap.

Zinc ingots: Indian zinc special high-grade (SHG) ingots averaged 8% higher y-o-y. This was driven by persistent tightness in ex-China inventories, mine concentrate constraints, and rising galvanising/infrastructure demand in India, which offset mid-year LME stock rebuilds and supported consistent premiums for high-grade ingots. LME zinc edged up by 1% y-o-y, averaging $2,850/t.

Lead ingots: Domestic lead primary ingots were down 1% y-o-y, being the only base metal commodity to record a decline. Prices faced pressure due to ample global refined surpluses, rising SHFE stocks, and softer conventional battery growth due to a shift to EVs. Lead prices on the LME also fell by 6% y-o-y to $1,990/t.

Outlook

The first quarter of the calendar year generally remains robust for the Indian steel market, as well as the whole economy. Conducive weather allows uninterrupted construction activity, while manufacturing activity accelerates too. With CY'25's GST boost and RBI's repo rate cuts, consumer demand is set to rise, boosting both steel and base metals activity. However, it is uncertain whether this momentum will continue beyond the first quarter. Weak global pricing and Chinese overcapacity may weight on the Indian market in CY'26, leading to a y-o-y decline in prices again. Base metals prices, however, may remain supported due to supply tightness.