India: Stainless steel finished prices ease w-o-w on weak demand, softening nickel prices

...

- Weak nickel weighs on buying sentiment

- BIS exemption for certain products extended till Mar'27

India's stainless steel finished market remained subdued during the week ended 1 July 2026, with prices edging lower amid declining nickel futures, weak downstream demand, and cautious procurement activity. Market participants largely remained on the sidelines, anticipating further price corrections.

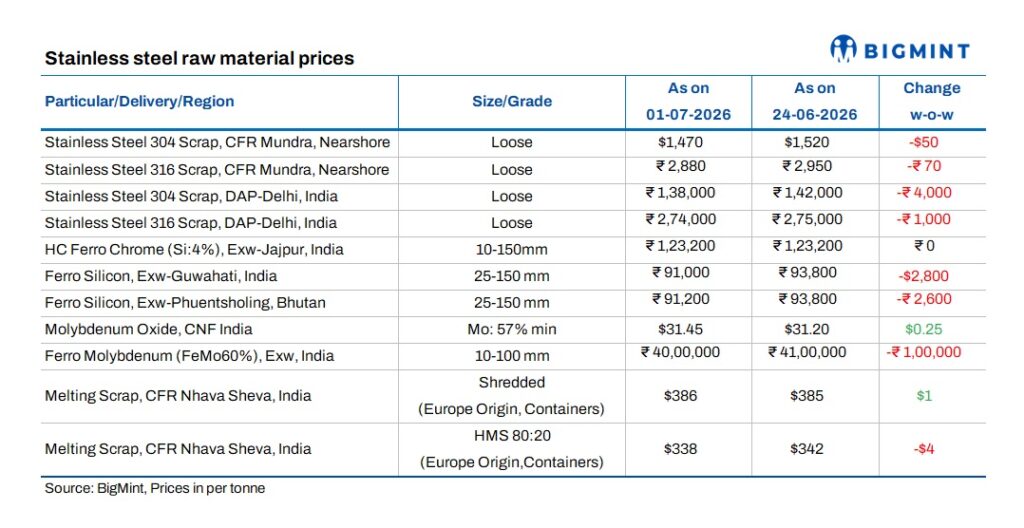

On the raw material front, mills maintained a cautious stance as falling nickel prices and sluggish finished steel demand limited fresh buying interest.

Finished flats market under pressure

India's finished flat market remained under pressure as buyers remained in a wait-and-watch mode.

A market participant said, "Buyers are delaying purchases as they expect prices to soften further. Nickel has weakened, other alloy prices have also corrected, and lower crude oil prices have added to the bearish sentiment."

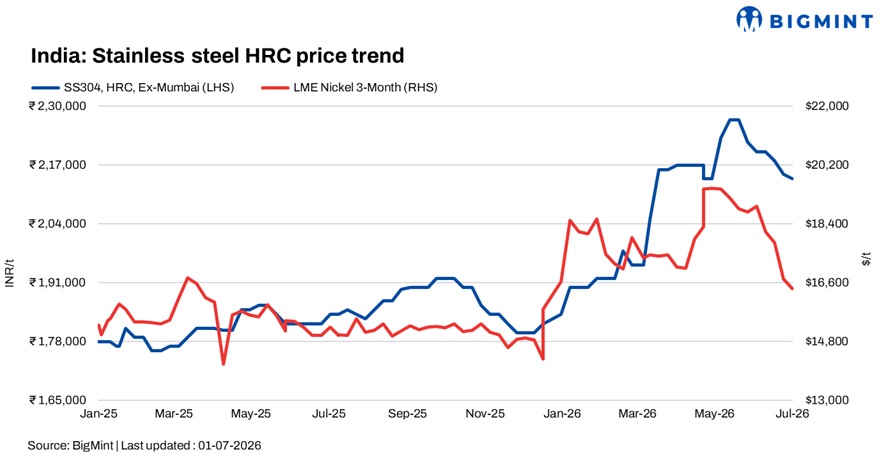

According to BigMint's assessment, 304-grade hot-rolled coil (HRC) prices declined by INR 1,000/t w-o-w to INR 214,000/t ex-Mumbai, while 316-grade HRC prices fell by INR 3,000/t to INR 395,000/t ex-Mumbai.

The Indian government has extended the exemption from mandatory Bureau of Indian Standards (BIS) certification for select stainless steel products until 31 March 2027, providing continued relief to manufacturers while retaining the compliance deadline for stainless steel hot-rolled products and billets.

Another trader noted that imported material currently remains costlier than domestic supplies. Indicative offers for Chinese 304 HRC were heard at $1,180-1,190/t, making domestically produced material more competitive. Across major stainless steel-producing regions, Indian prices continue to remain among the most competitive.

Long product prices continue to soften

BigMint's benchmark 304L black round bar prices declined by INR 2,000/t to INR 188,000/t ex-Mumbai. Meanwhile, 316L black round bar prices stood at INR 340,000/t ex-Mumbai, down by INR 5,000/t.

Export activity remained sluggish as geopolitical tensions continued to affect buying interest and trading confidence. Indicative export offers for 304 bright bars were heard at $2,350-2,400/t FOB India, while 316 bright bars were reported at $4,150-4,200/t FOB India.

Global market

Globally, European stainless steel producers, including Aperam, Acerinox, and Outokumpu, reduced July alloy surcharges for 304-grade stainless steel following the correction in nickel prices.

Meanwhile, Taiwanese producers Tang Eng Iron Works, Yieh United Steel Corporation (Yusco), and Walsin Lihwa maintained flat July prices, citing elevated inventories and sluggish downstream demand despite continued pressure from high production costs.

China's stainless steel market remained subdued this week, with both futures and spot prices under pressure amid weak seasonal demand, declining nickel prices, and cautious buying sentiment. While major mills maintained firm offers and ongoing maintenance shutdowns helped limit supply, sluggish downstream demand and aggressive destocking by traders continued to weigh on spot transactions.

Meanwhile, expectations that US interest rates will remain highand uncertainty surrounding Indonesia's nickel ore policy, kept market sentiment bearish. Steel mills also faced margin pressure as firm raw material costs, particularly for high-grade NPI, contrasted with softer finished stainless steel prices.

Raw material scenario

Outlook

India's stainless steel market is expected to remain under pressure in the near term as weak downstream demand, adequate inventories, and declining nickel prices continue to weigh on market sentiment. Buyers are likely to maintain a wait-and-watch approach, while any sustained recovery in prices will depend on improvements in end-user demand and stability in the nickel market.