India: SECL to auction nearly 500,000 t of non-coking coal in Jun'26

...

- Kusmunda, Saraipalli lead among suppliers

- Road mode dominates offered volumes

South Eastern Coalfields Limited (SECL) is scheduled to conduct an e-auction of around 0.49 million tonnes (mnt) of non-coking coal on 9 June 2026 under the Single Window Mode Agnostic (SWMA) e-auction scheme. The auction basket comprises multiple road- and rail-linked lots across key mining regions, offering coal grades ranging from G5 to G13.

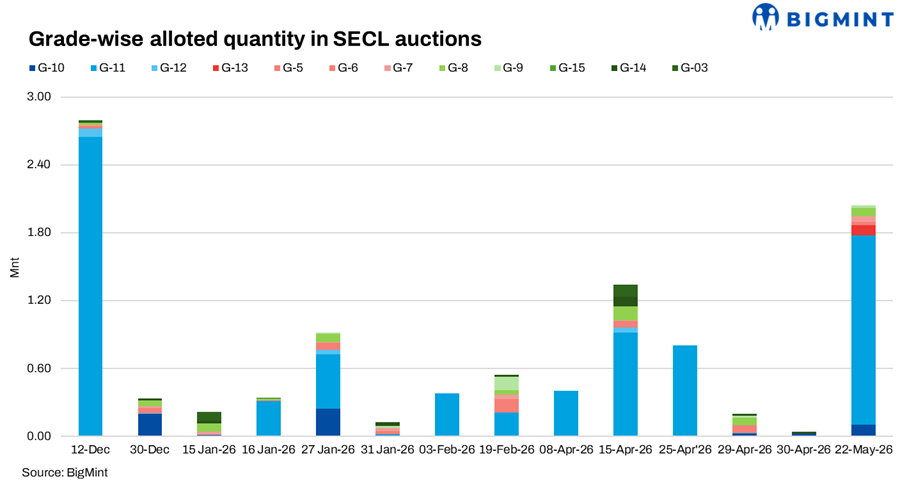

The upcoming auction follows strong participation in SECL's previous non-coking coal e-auction held on 22 May 2026, where around 2.04 mnt was allocated against an offered quantity of 2.17 mnt. Demand remained firm across key grades, particularly G11 coal, which accounted for around 1.67 mnt of total allocations. The grade achieved an average winning price of INR 1,612/t against the notified price of INR 1,184/t, resulting in a premium of nearly 36%, indicating healthy buying interest for domestic coal.

Kusmunda dominates auction volumes

Kusmunda OC will be the largest contributor in the upcoming auction, offering 204,000 t of G11-grade coal. Of the total quantity, 200,000 t will be available through the road mode, while the remaining 4,000 t will be offered through the Gevra Road railway siding. The mine accounts for more than 40% of the total quantity on offer.

Saraipalli emerges as key supplier

Saraipalli OC will be the second-largest supplier, with a cumulative 150,000 t on offer. The mine will auction 100,000 t of G13-grade coal and 50,000 t of G10-grade coal, with the entire quantity available through road dispatches.

Mid-sized offerings from Sharda, Rajgamar, Amera

The Sharda cluster will offer 30,000 t of G6-grade coal, comprising 26,000 t through road mode and 4,000 t through Burhar railway siding. Rajgamar UG will make available 30,000 t of G5-grade coal through road dispatches, while Amera OC will offer another 30,000 t of G6-grade coal through road mode.

Meanwhile, the Vijay West cluster will contribute 24,000 t of G7-grade coal, including 20,000 t through road mode and 4,000 t through Duman Hill siding.

Smaller lots add grade diversity

The Amadand cluster will be offering 9,000 t of G10-grade coal through a combination of road and rail modes. Similarly, the NCPH cluster will make available 9,000 t of G6-grade coal, while Dhelwadih UG will offer 5,000 t of G8-grade coal through road mode.

The auction basket provides a diverse mix of grades, catering to sponge iron units, captive power producers and other industrial consumers.

Road mode remains the preferred dispatch route

Road-linked quantities account for the majority of the auction volumes, reflecting the strong presence of regional consumers. Rail-linked lots will be available through Gevra Road, Burhar, Duman Hill, Govinda and NCPH sidings, offering logistical flexibility for buyers located farther from the mines.

Domestic coal remains competitive

The upcoming auction comes at a time when domestic coal continues to exert pressure on imported cargoes. BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t as on 2nd June. Improved grade availability and regular auction volumes have continued to support domestic supply, encouraging consumers to prioritise domestic procurement over imported alternatives.

Market participants noted that recent SECL auctions witnessed largely flat bidding sentiment, with some quantities remaining unsold amid cautious buying interest. In contrast, recent NCL auctions attracted relatively stronger premiums, reflecting selective demand for certain grades and locations. Washed coal offers were heard around INR 5,500/t ex-plant, although overall demand remained limited.

Overall, the 9 June auction is expected to provide fresh insights into domestic coal demand and buyer appetite ahead of the monsoon season. Market participants will closely monitor bidding intensity and premium trends, particularly for higher-grade G5-G7 coal. Demand for lower-grade G10-G13 material is likely to remain supported by cost-conscious consumers across the sponge iron, power and manufacturing sectors, while comfortable domestic availability may continue to cap aggressive bidding.