China's steel exports decline 10% y-o-y in Jan-Apr'26 as demand weakens across key regions

...

- Southeast Asia, Middle East & Africa witness double-digit declines in exports

- Europe and CIS record growth, but volumes insufficient to offset overall decline

- China's export compliance measures from Jan'26 add pressure on exports

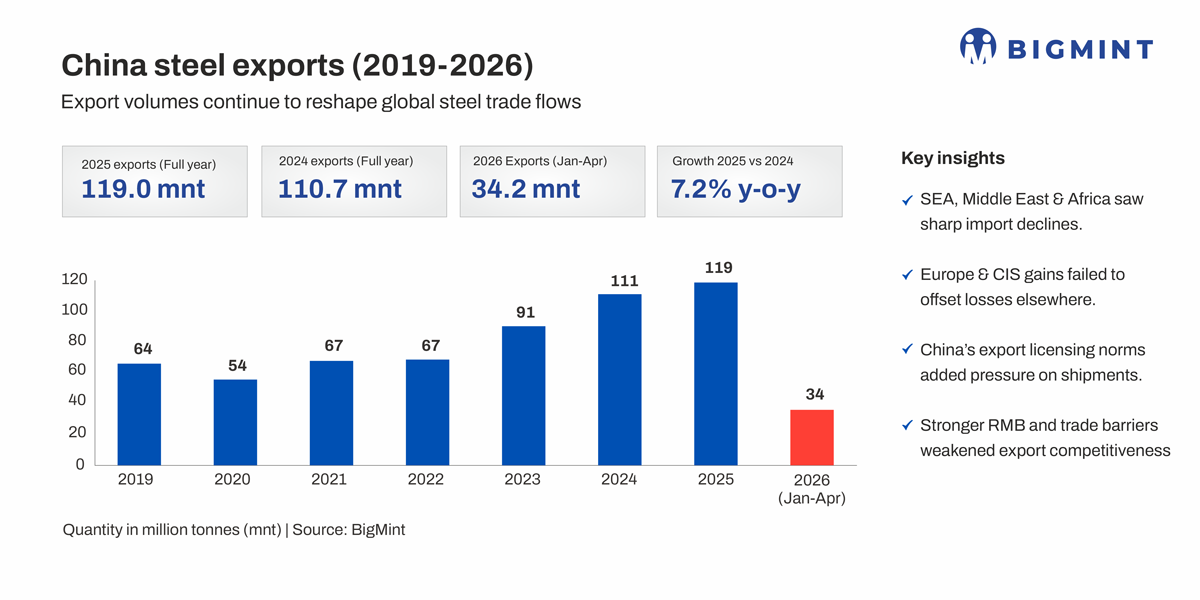

Morning Brief: China's steel exports declined 10% y-o-y to 34.2 million tonnes (mnt) in January-April 2026 from 37.9 mnt in the corresponding period last year, indicating that global demand conditions across key export markets remained under pressure despite continued reliance on exports by Chinese mills.

The decline was broad-based, with major export destinations including Southeast Asia, the Middle East & Africa, East Asia, and South Asia all recording contractions during the period. Given that these regions account for the majority of China's steel exports, the scale and spread of the slowdown suggest that weakening regional demand and rising trade barriers are increasingly limiting global absorption of Chinese steel rather than simply redirecting trade flows between markets.

Although Europe and the CIS recorded positive growth, the increase in shipments to these regions remained insufficient to offset the decline across China's core export destinations.

Export curbs, weak real estate demand add pressure on shipments

China's steel export volumes were also impacted by stricter export compliance measures implemented from January 2026. The latest measures, aimed at discouraging aggressive overseas shipments and improving domestic industry stability, increased compliance and transaction costs for exporters at a time when global trade conditions were already weakening.

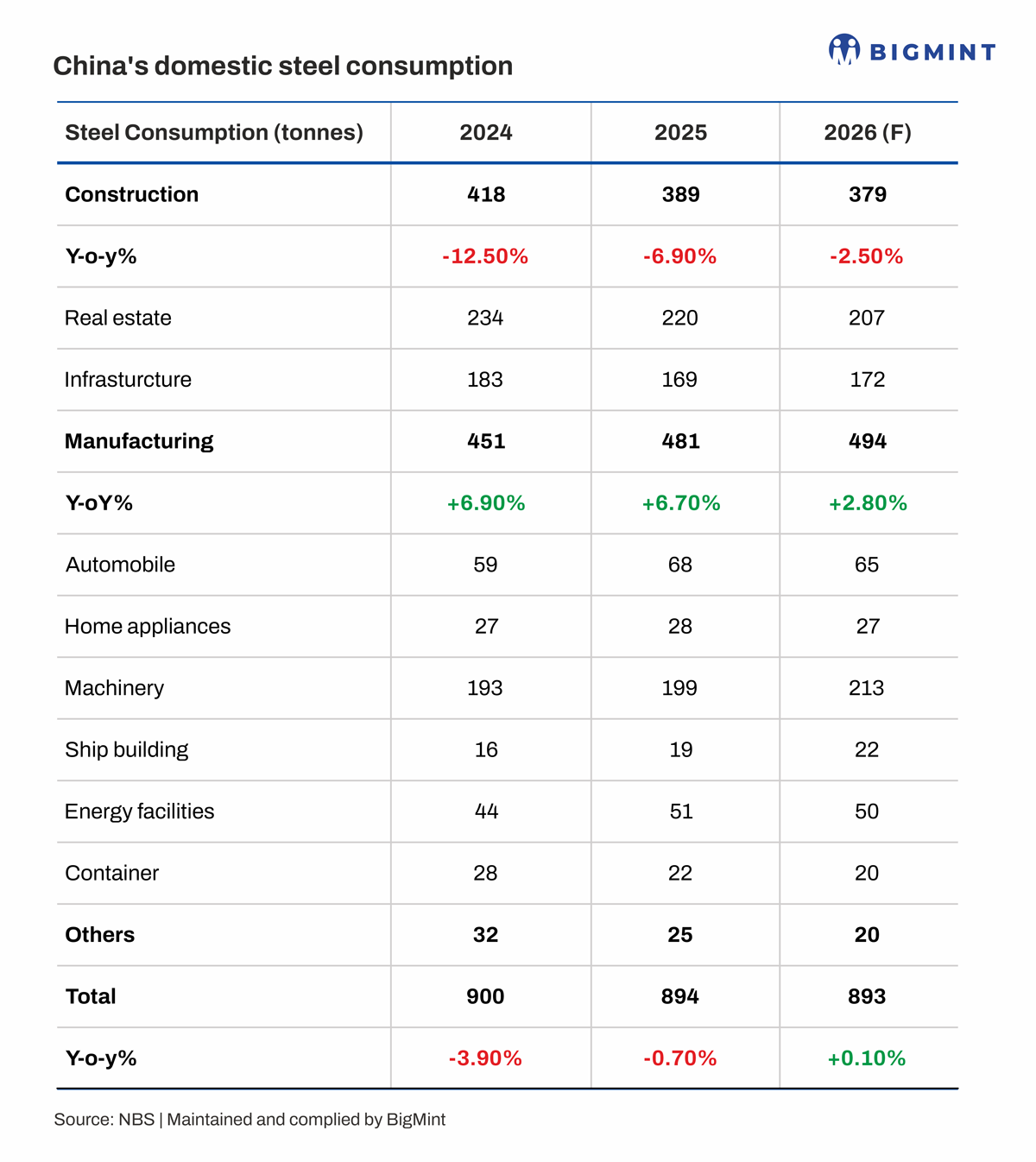

At the same time, China's domestic steel demand remained structurally weak, particularly across the construction and property sectors, which have traditionally been among the country's largest steel-consuming segments. Real estate indicators such as new construction starts, under-construction area, and housing completions have all weakened significantly since 2023, while infrastructure investment growth has also moderated amid lower local government spending and shifting policy priorities.

Although manufacturing-linked demand from automobiles, shipbuilding, machinery, and energy equipment remained comparatively more stable, it was insufficient to fully offset the broader contraction in construction-led steel demand. Consequently, Chinese mills continued relying heavily on exports to absorb surplus volumes even as overseas demand conditions softened.

Rising trade barriers increasingly constrain Chinese steel flows

Chinese steel exports are also facing mounting pressure from rising anti-dumping measures and import restrictions across major consuming regions. Multiple countries including Brazil, Vietnam, Indonesia, South Korea, Pakistan, Mexico, and Canada have either imposed or expanded anti-dumping duties, safeguard measures, or quota restrictions on Chinese steel products in recent months.

Traditional export destinations such as Vietnam, South Korea, and Brazil have also shown weakening import trends amid rising anti-dumping measures, domestic industry protection policies, and softer downstream steel demand, limiting China's ability to redirect surplus steel into alternative overseas markets. In Europe, tighter safeguard quotas and higher off-quota tariffs are expected to further restrict Chinese steel flows during the second half of 2026.

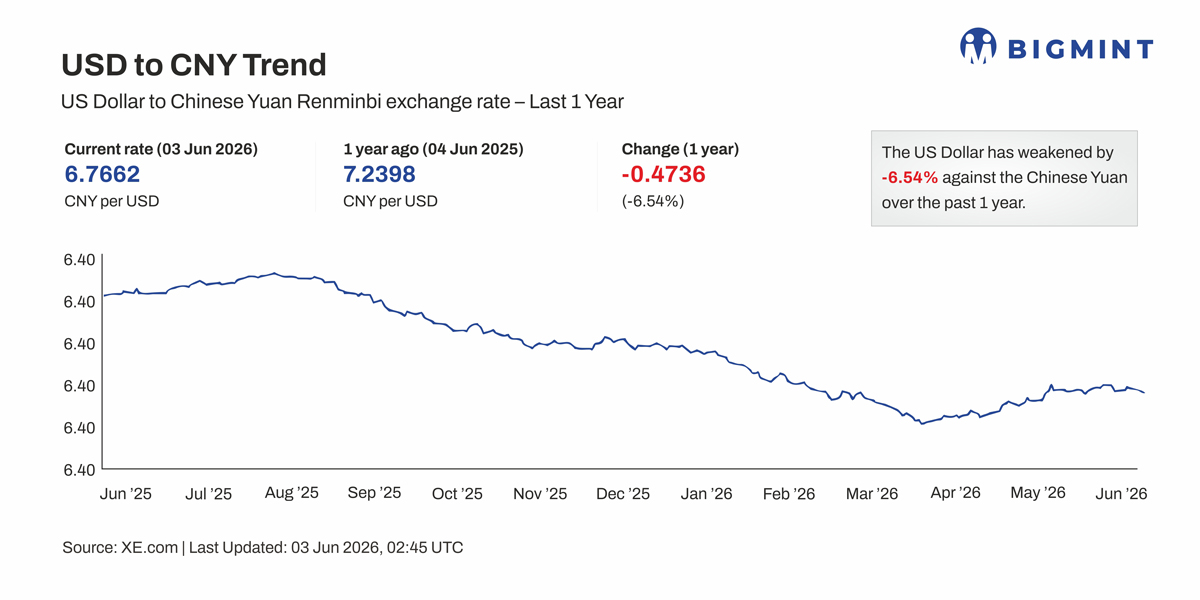

In parallel, appreciation pressure on the Chinese yuan (RMB) is also expected to reduce China's export pricing advantage in overseas markets. Together, rising trade barriers, weaker regional demand, and currency-related headwinds are increasingly constraining Chinese steel exports despite continued domestic oversupply conditions.

Southeast Asia and Middle East demand weakens

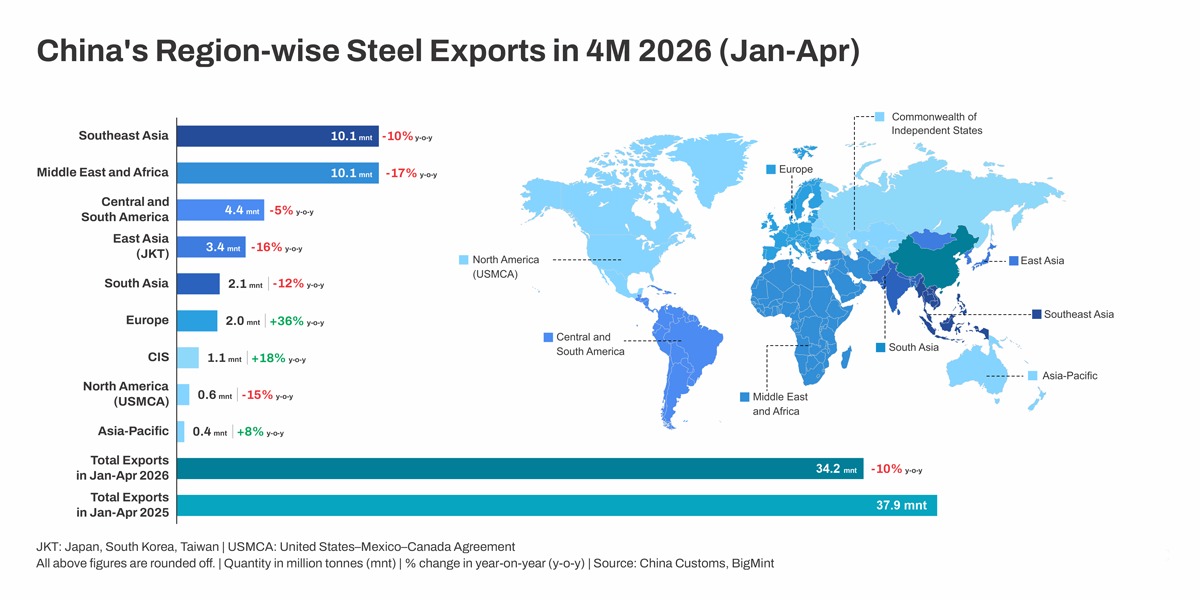

Southeast Asia remained China's largest export destination alongside the Middle East & Africa, with shipments to both regions standing at 10.1 mnt in Jan-Apr'26. However, exports to Southeast Asia declined 10% y-o-y, while shipments to the Middle East and Africa fell more sharply by 17%.

The decline in Southeast Asia is particularly significant as the region has remained one of the primary destinations for Chinese steel exports in recent years amid weakness in China's domestic property and construction sectors. The continued contraction suggests that demand across key ASEAN markets remained subdued despite ongoing infrastructure activity in parts of the region.

Meanwhile, the sharper fall in exports to the Middle East & Africa points to weaker import appetite across several major consuming markets as well as continued logistical and trade disruptions affecting regional flows.

East Asia and South Asia reflect softer industrial demand

Exports to East Asia, comprising Japan, South Korea, and Taiwan (JKT), declined 16% y-o-y to 3.4 mnt, reflecting weaker manufacturing-linked steel demand, softer export-oriented industrial activity, and rising anti-dumping measures across Northeast Asia.

South Asia also recorded a 12% y-o-y decline in imports from China, with shipments falling to 2.1 mnt during the four-month period. The decline reflected increasing trade protection measures across parts of Asia as well as softer construction-linked steel demand across several emerging markets.

Central and South America registered a comparatively smaller decline of 5%, suggesting that import demand remained relatively more stable across parts of Latin America despite rising anti-dumping actions and domestic industry protection measures. Meanwhile, shipments to North America fell 15% y-o-y amid elevated tariff barriers and stricter trade enforcement measures.

Europe, CIS emerge as secondary growth markets

Europe was the only major region to record strong growth, with Chinese steel exports rising 36% y-o-y to 2 mnt in Jan-Apr'26, although volumes remained significantly below shipments to Southeast Asia and the Middle East & Africa.

The increase likely reflected continued import demand amid elevated production costs and tighter supply conditions in parts of Europe. Exports to the Commonwealth of Independent States (CIS) also increased 18% y-o-y to 1.1 mnt, albeit from a relatively lower base.

However, growth across these secondary markets remained insufficient to compensate for the broad-based slowdown across Chinas primary export destinations.

Outlook

China's steel exports are expected to remain under pressure in the near term as demand across major importing regions remains uneven amid rising protectionism, weak manufacturing conditions, and slowing industrial activity.

While Chinese mills are likely to continue relying on exports amid weak domestic demand conditions, incremental export volumes may increasingly face resistance across global markets rather than being easily redirected to alternative regions.

At the same time, China's export mix is gradually shifting towards semi-finished steel products such as billets, which continue witnessing relatively stronger overseas demand amid comparatively lower trade restrictions than finished steel products. This may partially offset weakness in finished steel exports, although growing trade barriers and weakening global demand conditions are expected to continue limiting overall export growth.