India's iron ore production rises 7% in FY'26 as merchant supply offsets fall in captive production

...

- Captive output declines amid disruptions

- Record output from key miners supports growth, but supply uneven

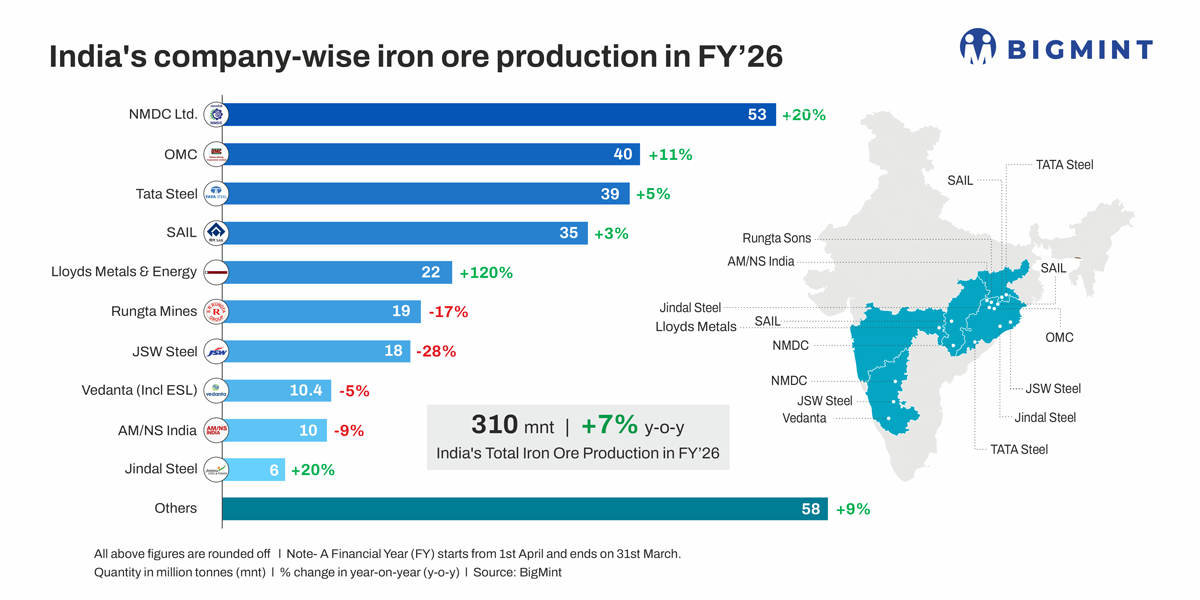

- NMDC top producer with volumes reaching 53 mnt in FY'26

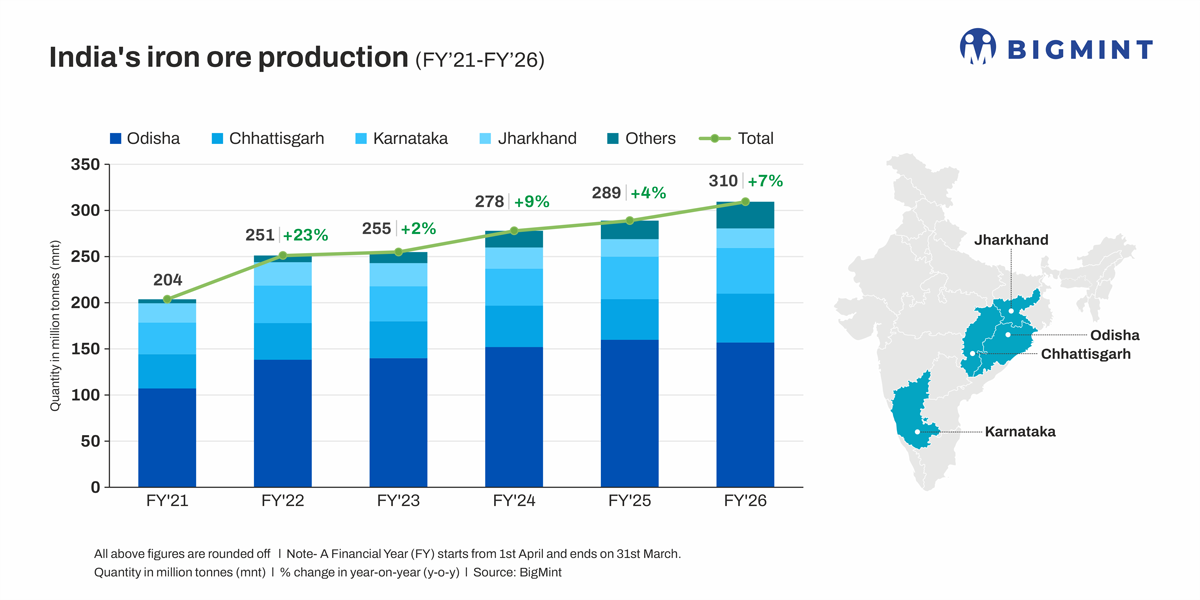

Morning Brief: India's iron ore production increased 7% year-on-year to 310 million tonnes in FY'26, as higher merchant output offset a decline in captive production. The increase reflects disruptions and transitional constraints across integrated producers, while merchant miners increased output, altering the composition of domestic supply.

The growth was supported by strong performance from large miners, with overall production reaching record levels during the year, according to government data. However, gains remained concentrated among a limited set of producers, highlighting uneven supply conditions.

Producer-wise trends

NMDC recorded the largest increase in output, with production rising 21% y-o-y to 53 million tonnes, marking a record level and reflecting higher production from its mining assets, as per government data. OMC also reported an 11% increase to 40 million tonnes, reinforcing its role as a key merchant supplier.

Tata Steel and SAIL registered modest growth of 5% and 3% respectively, indicating stable operations without significant capacity additions. In contrast, several producers saw output decline due to operational and regulatory factors. JSW Steel's production fell 28% to 18 million tonnes, reflecting disruptions linked to mine transitions.

Rungta Mines reported a 20% decline despite EC of around 33.3 million tonnes, as sourcing of nearly 4 million tonnes from OMC reduced its own mining output. AMNS India's production declined 9% to 10 million tonnes due to disruptions at its Thakurani mine, impacting overall volumes. Vedanta (including ESL) reported a 5% decline, indicating operational constraints at the margin.

Among smaller producers, Lloyds Metals and Energy more than doubled output from a low base, while Jindal Steel Limited reported an 18% increase, supported by initial production from the Roida I mine. However, temporary closure due to statutory clearance issues limited its contribution to a short operating period.

Supply structure shifts

Captive and merchant production diverged during the year, with captive output declining 3% y-o-y to 120 million tonnes, while merchant production increased 15% to 190 million tonnes. The decline in captive output reflects disruptions, regulatory delays, and mine transitions across integrated producers, while merchant miners increased supply to partially offset these constraints, increasing the share of market-linked output.

Production remains geographically concentrated, with Odisha accounting for 157 million tonnes, followed by Chhattisgarh (53 million tonnes) and Karnataka (49.5 million tonnes) . This concentration indicates continued dependence on a limited number of mining regions, where regulatory developments and operational conditions can influence overall output.

Outlook

India's iron ore production is expected to remain supported by incremental output from merchant miners and sustained performance from large producers. Domestic production growth is supported by steel demand from infrastructure and capacity expansion, according to government data.

However, supply growth is likely to remain uneven. Delays in operationalising auctioned mines, regulatory clearances, and disruptions at existing mining assets have constrained output across select producers, according to industry reports, and are expected to continue influencing production trends.

While higher merchant output is offsetting disruptions in captive mining, the divergence in supply structure suggests continued reliance on external sourcing during periods of disruption. As a result, despite higher overall production, supply conditions are likely to remain sensitive to disruptions across key producers.