Weekly round-up: Indian imported coal prices weaken amid cautious demand, rising supply

...

- Buyers increasingly shift to cheaper domestic coal, alternative fuels

- Coal freights show mixed trends on ample vessel supply, easing bunkers

Indian coal market sentiment remained weak in the week ending 10 April, with subdued demand across imported segments and stable domestic prices. Buyers stayed cautious amid uncertain downstream demand, while rising port inventories and steady supply weighed on prices. Fuel switching towards domestic coal and alternatives persisted, especially in the cement and retail sectors. Freight volatility and easing seaborne prices further reflected a market under pressure with limited buying support.

Indonesian coal prices ease

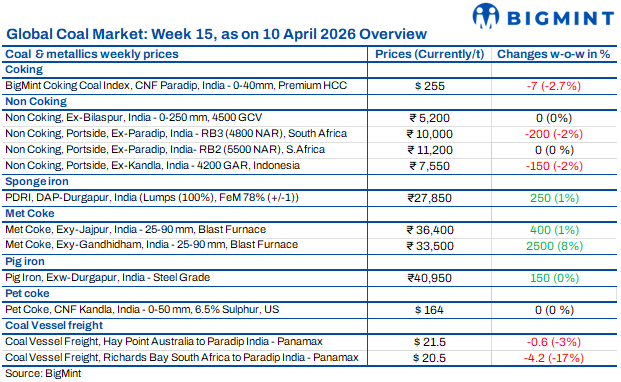

Indian portside Indonesian thermal coal prices declined slightly w-o-w on 10 April amid steady supply and cautious demand. BigMint assessed 5,000 GAR down INR 100/t to INR 9,300/t at Kandla and INR 9,200/t at Vizag, while 4,200 GAR fell INR 150/t to INR 7,450/t and INR 7,350/t, respectively. 3,400 GAR eased INR 50/t to INR 5,400/t at Navlakhi. Power plant stocks stood at 59.6 mnt, indicating comfortable supply. Additionally, as per sources, ceramics units in Morbi are expected to resume operations only from next week. However, stable freights and mixed global cues kept the market within a narrow range.

South African coal prices ease

South African thermal coal prices at Indian ports softened w-o-w on 9 April 2026 amid weak sponge iron demand, limited enquiries, and falling seaborne offers. BigMint assessed exw-Paradip RB2 (5,500 NAR) down INR 200/t at INR 11,200/t, while RB3 (4,800 NAR) fell INR 50/t to INR 10,200/t. At Vizag, RB2 declined by INR 250/t to INR 11,100/t, while RB3 remained stable at INR 10,100/t.

Seaborne RBCT 5,500 NAR offers dropped to $92-93/t from $97/t, while 4,800 NAR slipped to $75/t. Freights to India also declined by $4-5/t w-o-w. Portside thermal coal stocks rose 3.3% to 13.53 mnt, adding pressure on sellers. Market participants expect further downside amid domestic coal preference and softer freight.

Domestic coal prices stable

Domestic thermal coal prices remained stable w-o-w as of 10 April 2026, with 5,000 GCV at INR 6,600/t and 4,500 GCV at INR 5,200/t. Market momentum slowed amid dull trading activity and weak buyer participation. Sentiment turned cautious following a fresh SECL auction announcement, which indicated higher upcoming supply. Market participants expect pricing pressure, with traders likely to reduce offers to clear stocks if demand remain subdued in the near term.

Coking coal index declines

BigMint's premium hard coking coal index fell by $7/t w-o-w to $255/t CNF Paradip on 10 April 2026 amid weak buying interest and softer freight. Market sentiment remained bearish, with spot levels near $228-230/t FOB Australia. India's coking coal imports rose to 6.5 mnt in March from 4.4 mnt in February, indicating comfortable inventories and limited fresh enquiries. Vessel freight rates declined w-o-w due to ample tonnage and cautious demand. Prices are expected to soften further amid sufficient supply and weak demand.

Domestic met coke prices rise

Domestic met coke prices increased w-o-w on 9 April 2026 due to higher production costs and firm import parity, though market activity remained subdued. BigMint assessed BF-grade coke prices in eastern India up INR 400/t to INR 36,400/t ex-Jajpur, while western India rose INR 2,500/t to INR 33,500/t ex-Gandhidham. Foundry-grade coke increased INR 200/t to INR 36,400/t ex-Rajkot. Limited trades were concluded at INR 34,000/t in Gandhidham and INR 36,750/t in eastern India.

Indonesian BF coke stood at $287/t CFR India, down $3/t, while Australian hard coking coal eased $1/t to $236/t FOB. Despite cost support, cautious buying and weak trade activity limited further price gains.

US thermal coal prices fall

US-origin thermal coal prices in India declined sharply as weak demand and rising inventories pressured the market. NAPP coal offers at west coast ports dropped from INR 17,000-18,500/t in late March to INR 14,500-15,500/t by 8 April. The correction followed delayed vessel arrivals and inventory build-up, with stocks at Kandla and Tuna reaching 307,000 t against weekly lifting of only 74,000 t. Cement producers and brick kilns shifted to cheaper domestic and alternative coals amid margin pressure. Market participants noted that buyers increasingly preferred South African, Russian, and domestic coal, while further downside remained likely unless prices corrected more.

Petcoke prices surge, buyers resist

Global petcoke prices rose to multi-year highs, supported by tight US refinery supply and Middle East disruptions. CFR India East 6.5% sulphur petcoke was assessed at $168/t, while freight increased to $50.50/t, raising landed costs. However, Indian cement buyers resisted higher offers and shifted to cheaper alternatives. Thermal coal at $103-105/t remained significantly more economical, widening the fuel cost gap. Offers were heard at $160-170/t, while bids stayed lower at $150-152/t, limiting deal activity. Buyers increasingly switched to domestic and imported coal, keeping demand weak.

Coal freights show mixed trends

Bulk coal freight rates to India showed mixed trends in the week ended 10 April amid ample vessel availability and cautious demand. Richards Bay-India routes were heard at $21-22/t for west coast and $23-24/t for east coast, reflecting slight softness. Bunker prices declined sharply by $124.5/t to $765.5/t, while the Baltic Index rose by 95 points to 2,161. However, a mismatch in charterer and owner expectations and uneven demand across routes kept fixing activity inconsistent, with rates expected to remain largely stable with a slight downside bias.