India: Portside Indonesian thermal coal prices remain resilient amid weak demand, supply constraints

...

- High-CV coal prices stay firm amid limited availability and steady supplier offers

- Coal inventories at Indian power plants fall w-o-w

Indian portside prices of Indonesian-origin thermal coal remained largely stable during the week ended 19 June 2026, as subdued buying interest from end-users was balanced by firm supplier offers and limited availability of higher-calorific material.

Market participants indicated that "demand for Indonesian coal remained weak due to sufficient domestic coal availability, cautious procurement ahead of the monsoon season, and relatively unattractive import economics. However, sellers continued to maintain higher FOB levels to support revenue amid supply-side uncertainties."

High-CV coal availability supports premium grades

Premium 5,000 GAR Indonesian coal prices remained stable week-on-week at around INR 11,000/t at Kandla and INR 10,900/t at Vizag.

Similarly, 4,200 GAR coal increased marginally by around INR 50/t to approximately INR 9,150/t at Kandla and INR 9,050/t at Vizag. Limited availability of higher-calorific coal in the spot market prevented a significant price decline. Market participant noted that "the 4,200 GAR segment continued to receive preference from industrial consumers due to its competitiveness against South African coal for blending requirements."

Lower-calorific 3,400 GAR coal remained stable at around INR 7,100/t at Navlakhi.

Freight correction provides limited relief to delivered prices

Freight rates for Supramax vessels from East Kalimantan to Navlakhi eased slightly by around $0.4/t w-o-w to nearly $22/t. Despite the marginal correction, freight levels remained elevated and continued to support delivered coal costs. With monsoon-related logistics challenges expected to persist, freight rates are likely to remain stable to firm in the near term.

Inventory levels decline, but import demand remains cautious

Coal inventories at major Indian ports declined by 5.7% w-o-w to 14.72 million tonnes in Week 24, compared with 15.61 mnt in Week 23, indicating improved evacuation. However, imported coal demand remained limited as consumers continued to rely on adequate domestic coal availability. Thermal power plant inventories also declined w-o-w to around 46.7 mnt as of 18 June 2026, equivalent to approximately 15 days of consumption, though uneven distribution led to critical stock positions at around 29 power plants.

Global thermal coal prices under pressure

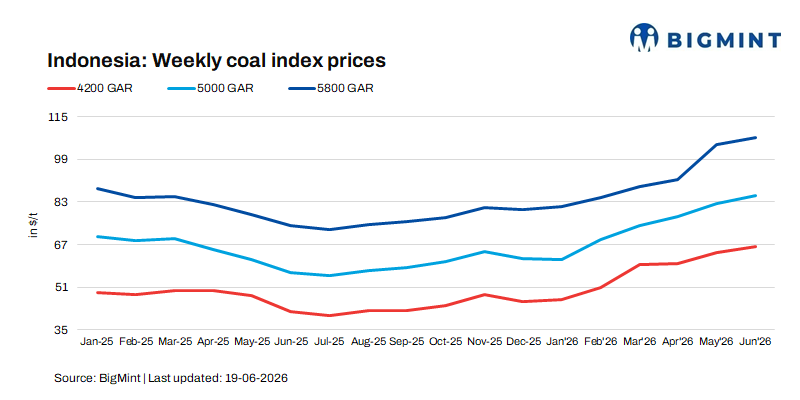

International thermal coal prices softened marginally during the week, marking the first decline after an 11-week consecutive upward trend, with Indonesian benchmarks declining across grades. 5,800 GAR prices decreased by around $0.5-1/t w-o-w, while 4,200 GAR and 3,400 GAR grades declined by approximately $1/t and $0.5/t, respectively. Easing geopolitical concerns and weaker spot demand contributed to the downward pressure.

Indonesia tightens coal blending regulations

Indonesia's Ministry of Energy and Mineral Resources (ESDM) implemented stricter coal blending rules under Regulation No. 6/2026, requiring mining companies to obtain approval from the ESDM Minister before blending coal to meet specific specifications. The regulation mandates submission of RKAB approvals, sales contracts, quality test results, and pre- and post-blending quality simulations covering calorific value, sulfur, moisture, and ash content. The move aims to improve transparency, strengthen monitoring, prevent quality manipulation, and safeguard state revenues.

Outlook

While weak import demand and softer global trends may limit price upside, restricted availability of high-CV Indonesian coal, firm supplier offers, and stable freight costs are likely to provide support. A market source mentioned that "in the coming week, market activity is expected to improve as traders return to the market and restocking interest resumes." Overall, Indonesian thermal coal prices are expected to remain range-bound with a stable-to-firm outlook in the near term, with any significant correction likely to be limited.