Falling petcoke prices challenge NAPP coal's gains in Indian cement sector

...

- Pet coke falls to low-to-mid $130s/t CFR India as supply improves

- Ample inventories, domestic coal availability keep imports subdued

The fuel procurement landscape for India's cement industry is shifting once again. After spending much of the first half of 2026 substituting expensive petroleum coke (petcoke) with US Northern Appalachian (NAPP) coal, cement producers are reassessing their fuel strategies as petcoke prices retreat sharply from recent highs.

The correction in petcoke prices has eroded much of the economic advantage that supported increased NAPP coal consumption earlier this year. However, rather than triggering a wholesale switch back to petcoke, the market is entering a more complex phase in which cement producers are balancing petcoke, imported coal, and domestic coal while maintaining a cautious procurement stance ahead of the monsoon season.

Petcoke's sharp correction alters fuel economics

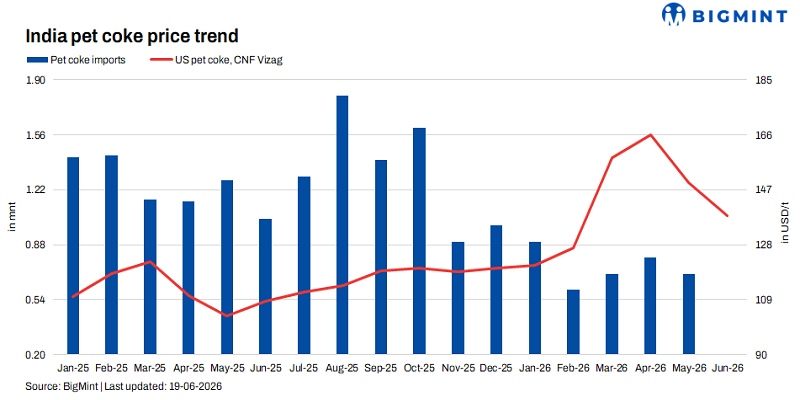

The petcoke market has undergone a dramatic reversal since April.

CFR India 6.5% sulphur petcoke prices climbed to around $160/t in early April after a prolonged rally driven by Middle East supply disruptions and tight global availability. The strength in prices prompted many cement producers to increase their use of imported thermal coal, particularly US NAPP coal, which offered a meaningful cost advantage on a delivered energy basis.

Since then, petcoke prices have corrected sharply. Increased refinery utilisation rates in the United States, improved export availability, and easing geopolitical concerns have pushed CFR India values back into the low-to-mid $130s/t range. Market surveys conducted across Indian cement producers indicate that petcoke offers have largely stabilised around $135-140/t CFR, with several buyers expecting prices to soften further towards $130/t before returning to the market.

The decline has effectively removed much of the pricing advantage previously enjoyed by NAPP coal.

Why cement producers can switch so quickly

Fuel costs account for roughly 30% of total cement production costs, making fuel procurement one of the most important margin drivers for the sector.

The economics of switching between petcoke and NAPP coal are influenced by India's import duty structure. High-sulphur petcoke attracts an import duty of approximately 11%, while imported thermal coal is subject to a significantly lower duty burden. This largely offsets petcoke's calorific value advantage and means relatively small changes in commodity pricing can quickly alter the preferred fuel choice.

Earlier this year, NAPP coal maintained a delivered price advantage of roughly $15-20/t versus petcoke, encouraging cement producers to increase coal consumption. The most visible example came from UltraTech Cement, which reduced petcoke's share in its fuel mix to 41% during the January-March 2026 quarter from 54% a year earlier.

That pricing advantage has now largely disappeared.

By late May and early June, NAPP coal was being discussed around $133-134/t CFR India, while petcoke offers were available at broadly similar levels. Once freight, duties, and calorific value adjustments are considered, the economics increasingly favoured a return to a more balanced fuel mix.

Buyers remain cautious despite improved petcoke economics

While petcoke has regained competitiveness, the market is not witnessing an aggressive buying spree.

Market surveys conducted between late May and mid-June show that many cement producers remain adequately covered for near-term requirements. Several buyers reported having already secured imported fuel requirements, while others indicated that existing inventories would be sufficient through much of the monsoon season.

The survey responses reveal a consistent theme: buyers are waiting for further price clarity before making significant commitments.

Some producers continue to monitor petcoke prices for additional downside potential, while others are avoiding fresh purchases altogether amid expectations of weaker seasonal demand.

As a result, procurement activity remains largely need-based rather than inventory-driven.

Domestic coal emerges as third competitive threat

The weakening outlook for NAPP coal cannot be attributed solely to petcoke.

Improved availability of domestic coal is also reducing dependence on imported fuels. Several cement producers reported increasing their use of domestic coal, citing favourable economics and adequate availability.

This is an important development because it transforms what was previously a two-way competition between petcoke and imported coal into a three-way competition involving domestic coal.

The availability of domestic fuel is providing additional flexibility to cement producers at a time when imported fuel prices remain volatile. This further limits the urgency to secure imported coal cargoes and increases competitive pressure across the entire fuel basket.

NAPP coal demand begins to cool

The impact on NAPP coal demand is becoming increasingly visible.

Combined NAPP coal inventories at Kandla and Tuna stood at approximately 406,000 t in mid-June, up from around 349,000 t a week earlier. Market participants describe current buying activity as largely replacement-driven, with few buyers willing to build additional inventories at prevailing prices.

A sizeable arrival pipeline is also approaching the market. Retail NAPP coal floating cargoes are estimated at roughly 225,000 t, while industrial consumers have close to 900,000 t of additional cargoes either afloat or scheduled to arrive during the coming weeks.

If monsoon-related demand slows as expected, these arrivals could place additional pressure on inventory levels and ex-works pricing.

Monsoon adds another layer of uncertainty

The fuel market is entering its seasonal demand slowdown.

The southwest monsoon typically reduces construction activity across large parts of India, weighing on cement consumption and production rates. At the same time, cement producers are facing mixed success in implementing price increases, increasing the importance of cost management and margin preservation.

The recent decline in petcoke prices is expected to lower fuel costs by approximately INR 70-80/t of cement production once lower-cost cargoes begin flowing through inventories. Although much of the benefit is likely to be reflected during the September quarter, the prospect of lower fuel costs is already influencing procurement decisions.

Consequently, many producers are focusing on preserving margins rather than aggressively expanding fuel inventories.

Outlook

The sharp correction in petcoke prices has removed much of the economic advantage that supported NAPP coal consumption during the first half of 2026.

However, the market is not witnessing a simple switch from coal back to petcoke. Instead, cement producers are entering the monsoon period with comfortable inventories, increased access to domestic coal, and greater flexibility across their fuel mix. As a result, procurement activity across all imported fuels has slowed, with buyers focusing on cost optimisation rather than volume accumulation.

The near-term outlook, therefore, remains challenging for US NAPP coal. Comfortable inventories, a substantial vessel pipeline, softer seasonal cement demand, and renewed competition from both petcoke and domestic coal are likely to keep buying interest subdued through much of the monsoon quarter.

Unless NAPP coal re-establishes a meaningful discount to competing fuels, the market is expected to remain characterised by selective, need-based purchasing rather than aggressive restocking.