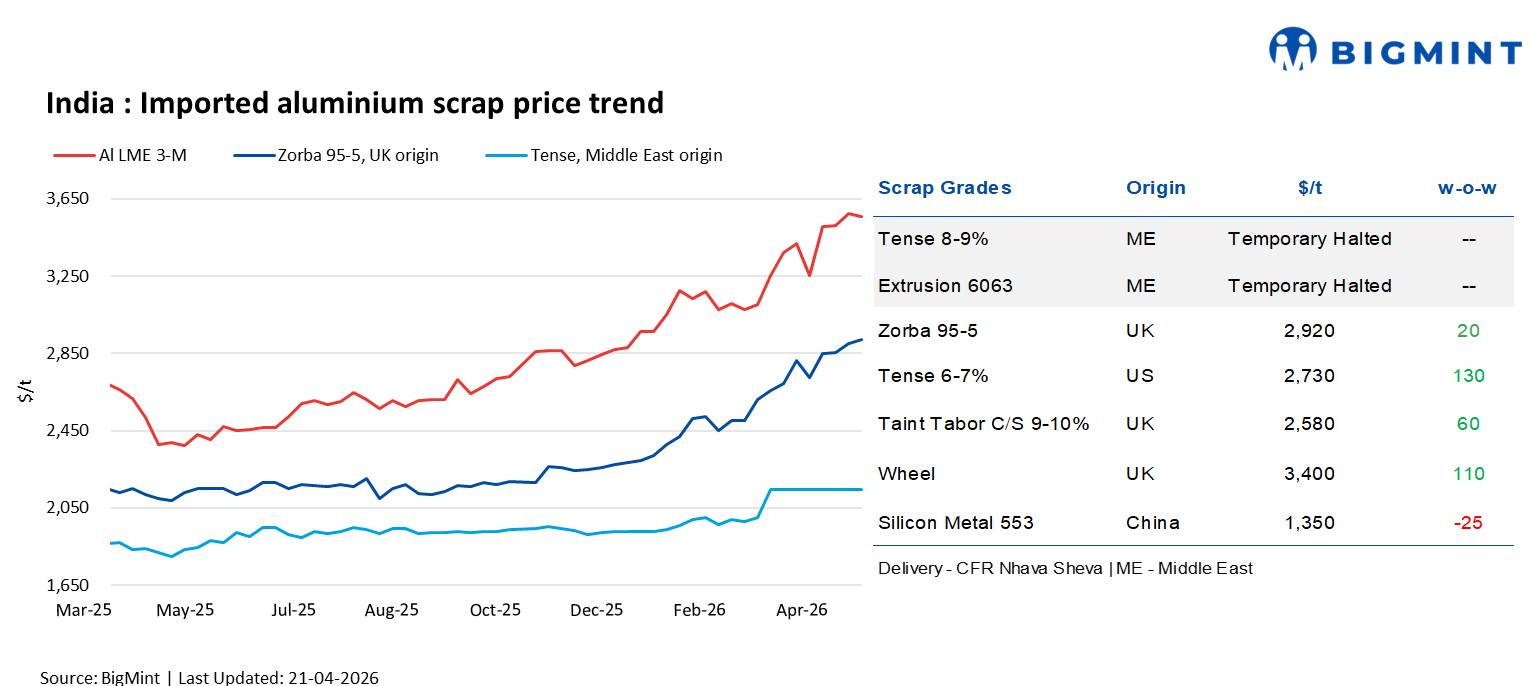

India: Imported aluminium scrap prices firm w-o-w on tight availability despite LME correction

...

- Imported scrap buying activity stays weak

- Khor Fakkan route sees delays due congestion

India's imported aluminium scrap prices strengthened w-o-w on 21 Apr'26, despite a decline in three-month aluminium prices on the London Metal Exchange (LME).

As per BigMint's latest assessment for CFR Nhava Sheva deliveries, UK-origin Zorba 95-5 scrap increased by $20/t w-o-w to $2,920/t, while US-origin Tense 6-7% scrap rose by $130/t w-o-w to $2,730/t, supported by constrained global scrap supply and sustained demand from downstream consumers.

LME aluminium softens w-o-w

Three-month aluminium prices on the London Metal Exchange (LME) declined by $13/t w-o-w to $3,553/t on 20 Apr'26 from $3,566/t on 14 Apr'26, indicating a marginal cooling in prices after the recent sharp rally.

Meanwhile, aluminium inventories on the exchange fell by 9,725 t to 386,250 t from 395,975 t over the same period, highlighting continued stock drawdowns and persistent tightness in exchange-visible supplies.

Prices softened slightly as geopolitical tensions eased following a ceasefire and improved shipping conditions through the Strait of Hormuz, which temporarily reduced supply-risk premiums in the market.

However, declining LME inventories, low global stock levels and tight near-term physical availability across key producing regions continued to provide underlying support to aluminium prices. Reduced trading participation during holiday-affected sessions also contributed to short-term volatility

Going forward, continued inventory drawdowns and tight physical availability are likely to keep aluminium prices supported in the near term, despite intermittent corrections driven by easing geopolitical risks.

Market direction is expected to remain sensitive to supply-side developments, logistics conditions and exchange stock movements, with tight fundamentals continuing to underpin price trends.

Market scenario

Market sentiment remains cautious despite the recent decline in LME aluminium prices, as scrap prices have largely held firm week on week. The limited pass-through of lower LME levels into scrap pricing has kept the market volatile and prevented any meaningful improvement in buyer sentiment.

Imported aluminium scrap buying activity continues to remain weak, with buyers holding back on fresh procurement as price corrections have not met expectations and uncertainty around LME trends persists. Certain grades such as aluminium Zorba have remained firm, supported by steady demand from the secondary aluminium sector.

The Indian imported scrap market remains subdued, with limited trade activity and muted participation across regions. Sentiment is further weighed down by ongoing logistical constraints and intermittent disruptions, including restricted flows via the Strait of Hormuz, which continue to keep import availability tight.

Although some material from the Middle East has started arriving through alternative ports such as Khor Fakkan, delays due to congestion persist, with priority being given to critical cargo.

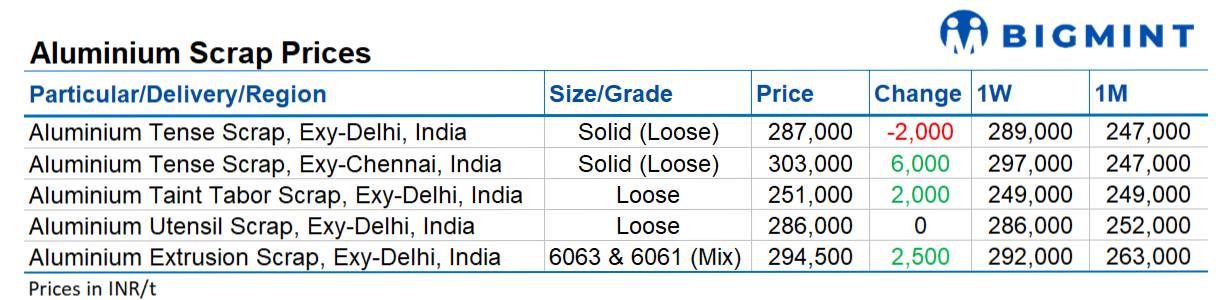

Domestically, aluminium prices have remained firm, while the scrap market continues to stay tight across both northern and southern regions, particularly for casting-grade Tense scrap, amid acute supply shortages.

Secondary producers are facing ongoing procurement challenges, leading to cautious buying activity and relatively subdued operating rates.

Chinese silicon prices

According to BigMint, China-origin silicon metal 553 prices decreased w-o-w by $25/t to $1,350/t from $1,375/t on a CFR Nhava Sheva basis amid limited buying interest.

Other updates

Chinese producer Tsingshan Holding Group is constructing an 800,000 t/yr aluminium smelter at Weda Bay industrial park, Indonesia, with initial capacity of at around 400,000 t/yr expected by end-2026 or early-2027.

Commodity traders Glencore, Mercuria and Trafigura have acquired minority stakes with expected offtake agreements. The project adds to Tsingshan's expanding Indonesian aluminium portfolio through the Taijih project with 600,000 t/yr capacity, the Juwan project operating at around 250,000 t/yr, and the Hua Chin joint venture with 500,000 t/yr capacity, further strengthening its regional aluminium footprint.

Outlook

Imported aluminium scrap markets are expected to remain firm in the near term, supported by tight global supply conditions, ongoing logistical constraints, and higher freight costs. However, liquidity is likely to stay limited amid cautious buyer sentiment.

On the domestic front, scrap availability is expected to remain constrained, which should keep spreads firm and continue to support secondary aluminium prices.