India: Auto sector posts strong 4MCY26 growth; PV sales rise 16% y-o-y

...

- FADA retail sales rise 21% y-o-y

- Marriage season boosts automobile retail demand

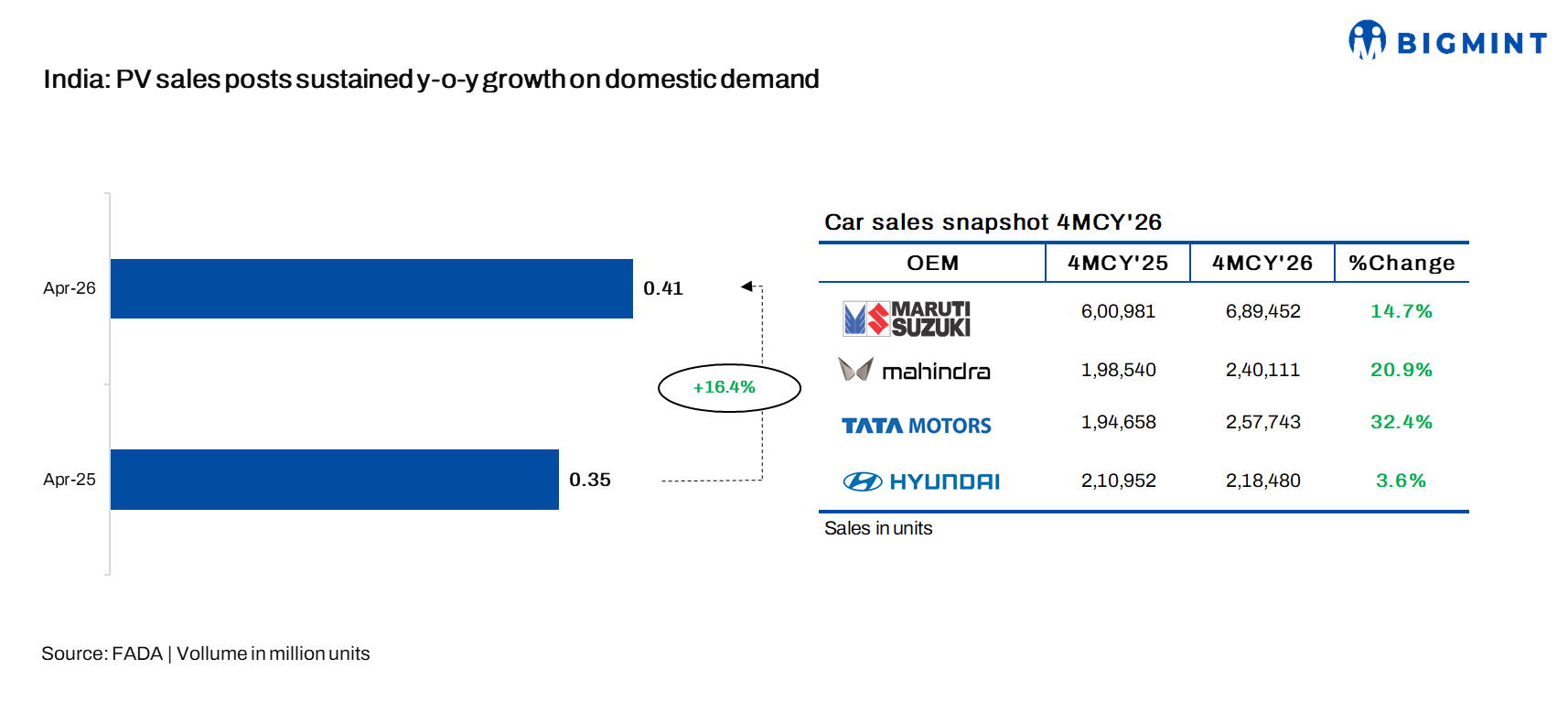

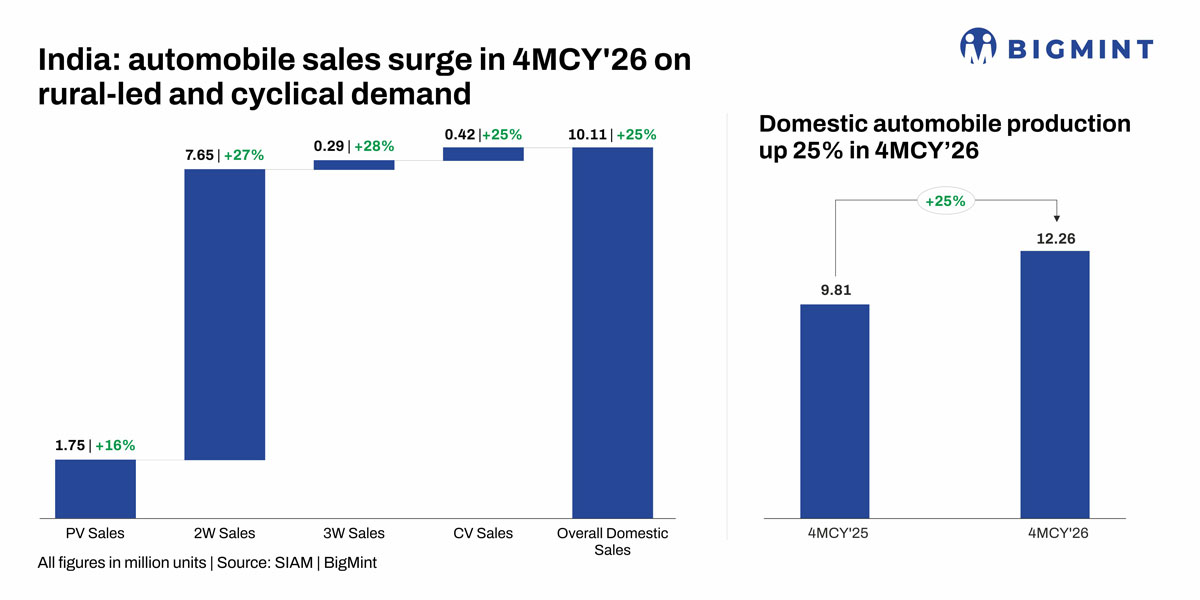

India's automobile sector recorded robust growth in 4MCY'26, as per industry sales data, with strong performance across all major segments. Passenger vehicle sales increased 16% y-o-y to 1.75 million units from 1.51 million units in 4MCY'25, while two-wheeler sales rose 27% to 7.65 million units from 6.03 million units. Three-wheeler sales also grew 28% to 292,229 units from 228,209 units.

Commercial vehicle sales increased 25% y-o-y to 419,948 units from 335,403 units. Overall domestic automobile sales rose 25% to 10.11 million units from 8.10 million units, while total automobile production also increased 25% to 12.26 million units from 9.81 million units in 4MCY'25.

Retail sales surge over 19% m-o-m in 2MCY'26

Meanwhile, FADA's retail data for 4MCY'26 reflected healthy year-on-year growth across all vehicle segments. Passenger vehicle sales increased 19% to 1.76 million units from 1.47 million units in 4MCY25, while two-wheeler sales rose 22% to 7.42 million units from 6.07 million units. Three-wheeler sales also grew 15% to 0.46 million units from 0.40 million units.

Commercial vehicle (CV) sales increased 13% to 0.42 million units from 0.37 million units, while tractor sales rose 23% to 0.36 million units from 0.29 million units. Overall retail sales increased 21% to 10.63 million units from 8.79 million units, indicating broad-based growth across segments.

Rural demand drives India auto sales surge

India's automobile retail market recorded strong 13% y-o-y growth in April 2026, reaching an all-time April high of 2.61 million units, according to FADA. The performance reflected sustained demand momentum from FY'26 into FY'27, with rural India significantly outperforming urban markets across major vehicle categories. Improved farm incomes, a strong rabi harvest, better liquidity conditions, and post-harvest spending supported demand for entry-level vehicles, tractors, and mobility solutions, indicating a structural broadening of demand beyond metro markets.

Seasonal factors such as the extended marriage season during May-June and stronger discretionary spending trends further supported demand. Improved financing access from banks and NBFCs, stable pricing conditions, and healthy consumer confidence also aided affordability, while product diversification across SUVs, small cars, and fuel-efficient models strengthened retail penetration. FADA highlighted that growth remained broad-based across all major categories, reflecting healthy underlying demand across the industry.