FTA-led imports trigger India's first ADC12 price correction of 2026 in Jun'26

...

- Landed costs of imports 7-8% lower than domestic prices in Chennai

- Import duties on aluminium scrap, tight supply lift production costs

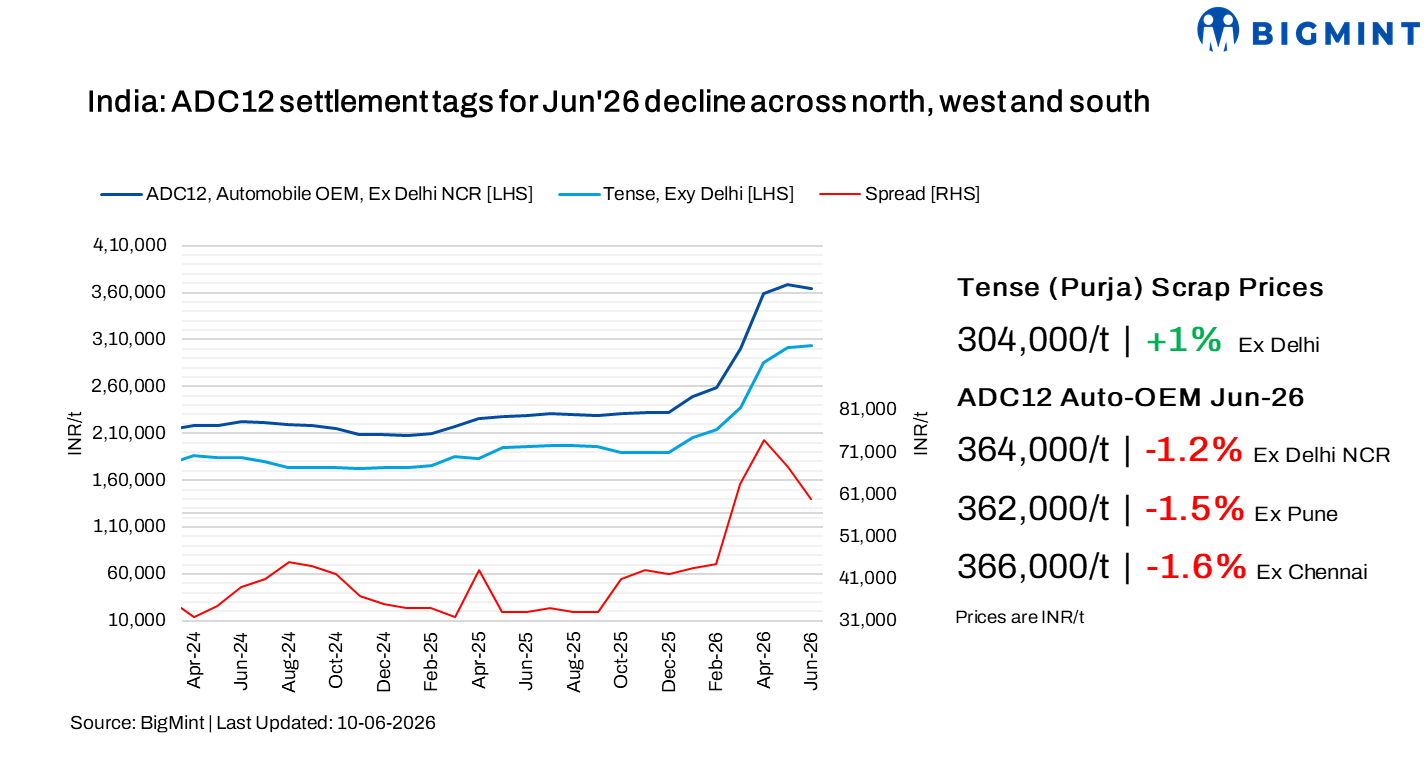

India's ADC12 aluminium alloy ingot prices declined m-o-m in June 2026, pressured by competitively priced imports despite firm raw material costs, healthy demand from the automotive sector, tight scrap availability, and ongoing supply disruptions linked to the West Asia conflict. This marks the first price correction since the beginning of 2026.

The spread between aluminium scrap and ADC12 alloy ingots narrowed to around INR 58,000-60,000/t in the Delhi NCR and Chennai regions. The contraction in the spread was primarily driven by the decline in ADC12 prices, while scrap prices remained largely firm during the month.

Market insights

Despite higher raw material costs, ADC12 prices in Chennai declined as buyers continued to resist further price increases. Transaction levels for 30-day payment terms were heard at INR 365,000-370,000/t, while supplier offers hovered between INR 370,000-373,000/t. However, persistent buyer resistance and aggressive negotiations pressured spot prices lower.

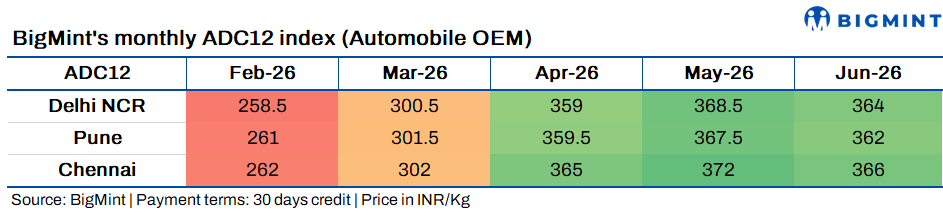

Similarly, the Delhi and Pune markets also witnessed a correction after India's leading automaker reduced its June ADC12 settlement price by INR 2,000/t, marking the first downward revision following a series of monthly increases since the start of 2026. While suppliers maintained June offers at around INR 365,000-367,000/t, and buyers' bids were heard between INR 360,000-363,000/t in both Delhi and Pune.

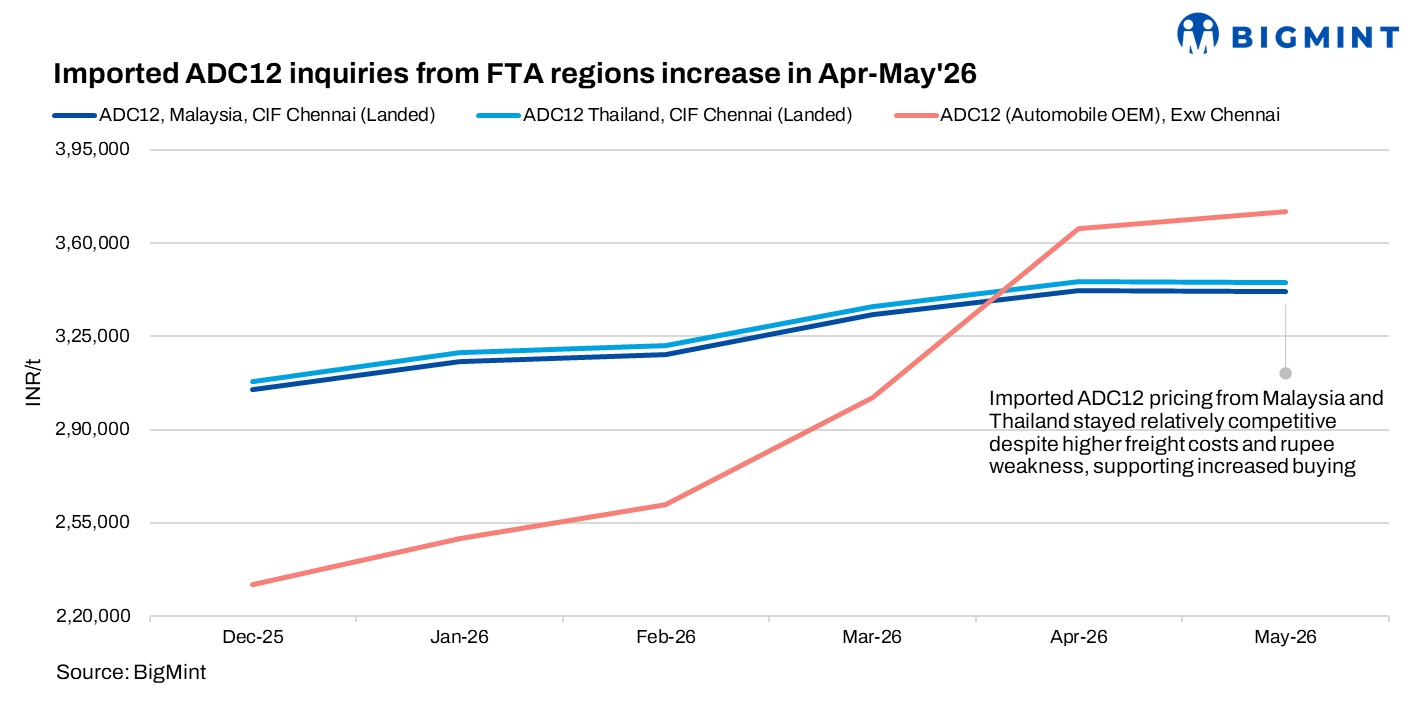

India's import enquiries for ADC12 alloy remained strong despite firm Asian offers, as elevated domestic prices continued to encourage buyers to source imported material, particularly from free trade agreement (FTA) countries such as Malaysia and Thailand.

Market participants noted that imported ADC12 remained more cost-competitive than domestically produced alloy across several Indian regions, even as Asian offers strengthened on the back of higher aluminium scrap costs. The widening price differential continued to attract buying interest from OEMs and secondary producers, particularly in southern India.

Landed prices of Malaysia-origin ADC12 in Chennai were assessed at around INR 342,000-343,000/t, while Thailand-origin material was heard at INR 345,000-346,000/t. In comparison, domestic OEM-grade ADC12 prices on an ex-works Chennai basis were assessed at around INR 365,000-370,000/t, providing an import cost advantage of approximately INR 20,000-30,000/t, or around 7-8%, over domestic material.

Market participants attributed the pricing advantage primarily to favourable FTA benefits enjoyed by Malaysia and Thailand, along with lower production costs due to duty-free aluminium scrap imports. In contrast, Indian secondary producers continued to face higher production costs because of import duties on aluminium scrap, tight scrap availability, and limited imported scrap arrivals, reducing their competitiveness against imported alloy.

Meanwhile, Middle East-origin ADC12 was offered at $3,350-3,360/t CIF West Coast India, with buying interest from western and northern Indian consumers also remaining firm due to its competitive pricing relative to domestic material.

Alloy imports surge y-o-y in 4MCY'26

Imports: India's ADC12 alloy ingot imports increased significantly, rising 261% y-o-y to 1,984 t in 4MCY'26 from 550 t in 4MCY'25. The sharp increase was driven by elevated domestic ADC12 prices, prompting buyers to increasingly source material from FTA countries, particularly Malaysia and Thailand.

Raw material trends

In June, imported aluminium scrap prices continued to strengthen, supported by the increase in LME aluminium prices, tight global scrap supply, and ongoing geopolitical tensions in West Asia. Market sentiment remained cautious amid weak buying activity, logistics disruptions, elevated freight costs, and rupee depreciation.

In line with imported scrap trends, domestic aluminium scrap prices, particularly casting-grade material used in ADC12 production, also remained firm as supply stayed constrained, especially in southern India.

Among key imported grades, US-origin tense recorded the sharpest increase of $165/t m-o-m to $2,945/t, while UK-origin wheel scrap gained $100/t to $3,570/t. Meanwhile, UK-origin taint tabor and UK-origin zorba 95-5 increased by $55/t each to $2,715/t and $3,035/t, respectively.

Rising scrap prices offered cost support and prevented a sharper decline in ADC12 prices.

Outlook

The domestic ADC12 market is expected to remain under pressure in the coming weeks as imported alloy continues to offer a notable cost advantage over domestic material. Nevertheless, elevated scrap prices, tight feedstock availability, and persistent logistics challenges are likely to prevent a sharp decline in domestic prices, keeping the market broadly balanced.