China: Zinc concentrate imports rise 9% y-o-y in 5MCY'26 as ingots exports surge

...

- Zinc ingot imports decline as China retains more value addition

- Record-low treatment charges may challenge China's processing-led trade model in H2'26

China's zinc trade pattern during the first five months of CY'26 points to an evolving supply chain strategy. While imports of zinc ore and concentrates continued to rise, sourcing of zinc ingots declined sharply. At the same time, exports of zinc ingots recorded robust growth, suggesting that Chinese producers are increasingly retaining more value addition within the country by processing imported raw materials into higher-value products before supplying overseas markets.

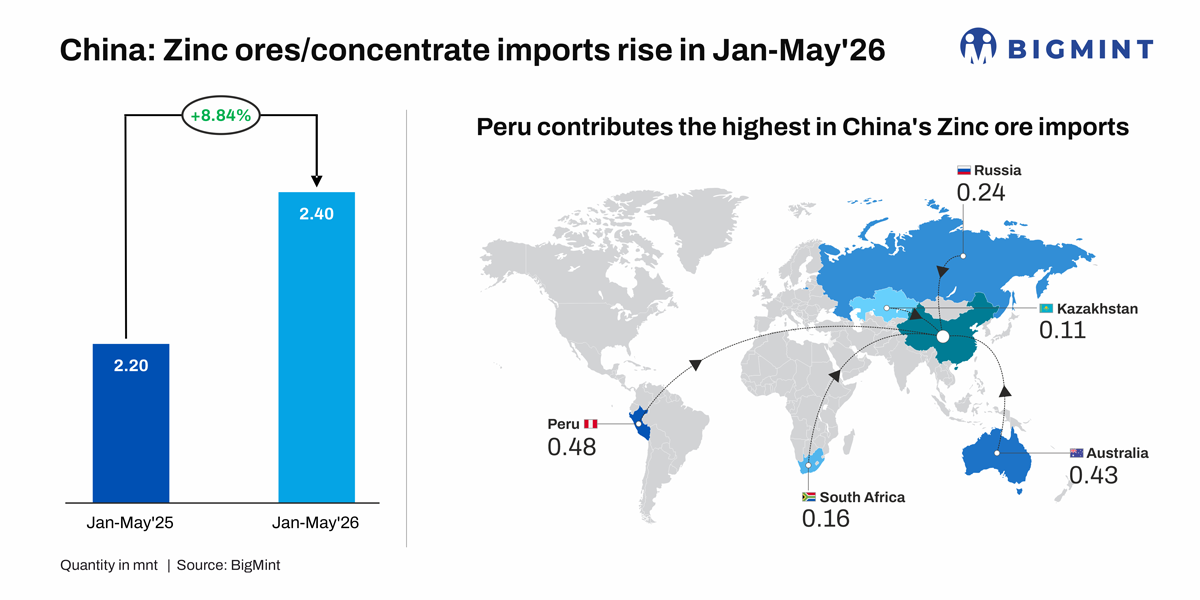

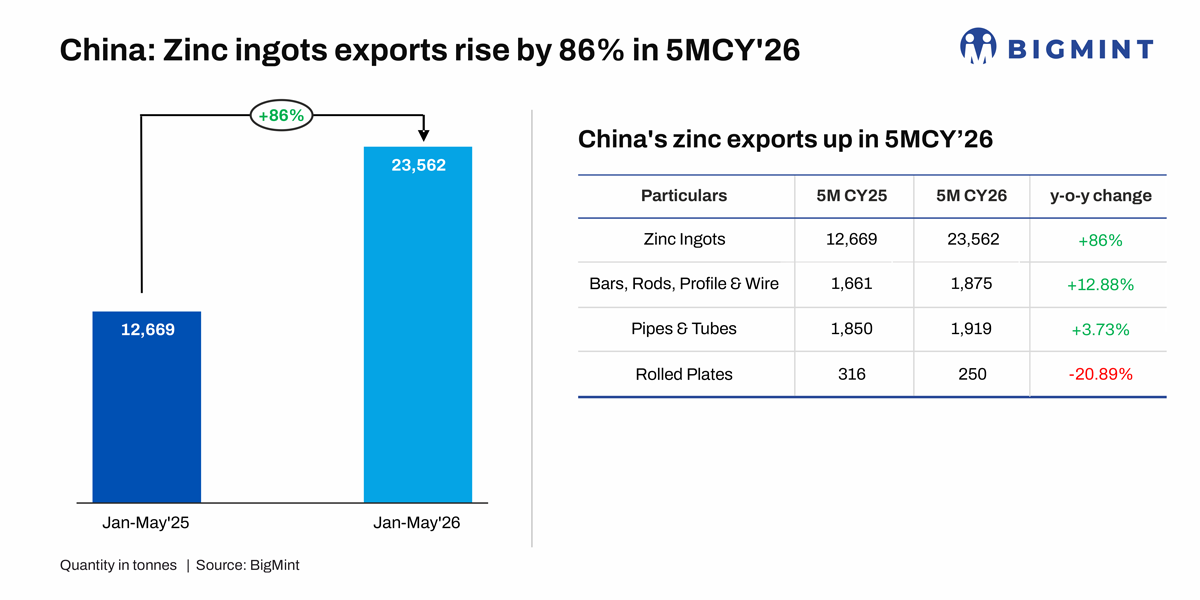

China imported 2.40 million tonnes (mnt) of zinc ore and concentrates during January-May 2026, up 8.8% y-o-y from 2.20 mnt in the corresponding period last year. In contrast, imports of zinc ingots fell 61.4% y-o-y to 67,390 tonnes (t) from 174,787 t, while exports of zinc ingots surged 86% to 23,562 t from 12,669 t over the same period.

The contrasting trade flows indicate that China is increasingly sourcing raw materials from overseas while undertaking more downstream processing domestically, reducing its dependence on imported zinc ingots.

Higher concentrate imports support domestic processing

The steady rise in concentrate imports reflects continued demand from Chinese smelters for raw material feedstock. Despite tightening global concentrate availability, smelters have maintained relatively high operating rates by securing imported ore to supplement domestic mine production.

Preliminary data from the International Lead and Zinc Study Group (ILZSG) also support this trend. China's zinc concentrate imports increased 16% y-o-y to 954,000 t during January-April 2026, while net refined zinc imports declined to just 35,000 t over the same period.

The figures suggest that domestic refiners remain well supplied with raw materials, enabling them to process more zinc within China rather than relying on imported intermediate products.

Why are imports declining while exports continue to rise?

The trade data point towards a gradual shift in China's zinc value chain.

As domestic refining and downstream processing capacity expands, Chinese manufacturers appear increasingly capable of converting imported concentrates into refined and semi-finished zinc ingots for both domestic consumption and export markets. This reduces the need for imported semi-finished material while creating additional export opportunities for locally processed products.

Competitive manufacturing costs, integrated supply chains and improving demand from overseas markets have also supported export growth.

China exported 23,562 t of zinc ingots during January-May, nearly double the volume shipped a year earlier. Market participants increasingly expect China to emerge as a net refined zinc exporter during 2026 as domestic production continues to outpace local consumption.

Finished zinc products present a mixed picture

Trade in finished zinc products remained relatively stable compared with the sharp shifts seen in concentrates and semi-finished products. While exports showed only modest changes across bars, rods, profiles, wire, pipes and tubes, shipments of rolled zinc plates declined 21% y-o-y.

On the import side, bars, rods, profiles and wire fell 29% y-o-y to 176 t, while rolled plate imports increased 75% to 1,314 t from a low base. Imports of pipes and tubes remained largely unchanged at 27 t.

Overall, movements in finished zinc products were far less pronounced, indicating that the biggest change in China's zinc trade is occurring in raw material procurement and semi-finished product exports.

Can this trade pattern be sustained?

The biggest challenge lies upstream. Treatment charges for imported zinc concentrates have fallen to around minus $50/t, the lowest level recorded in more than a decade, as supply disruptions tightened the global concentrate market. Shipments from Iran have been affected by geopolitical tensions, Russia's Ozernoye mine has underperformed expectations, while operational disruptions at Kazzinc's facilities in Kazakhstan and Nexa Resources' Cajamarquilla smelter in Peru, along with shipment constraints from Cuba, have further reduced concentrate availability.

Although many Chinese smelters continue operating by relying on revenues from by-products such as sulphuric acid, silver, lead and cadmium, persistently low treatment charges are placing increasing pressure on processing margins. The tightening concentrate market has also fuelled investor optimism. Speculative long positioning in zinc has climbed to record highs on expectations that prolonged feedstock shortages could eventually force smelter production cuts and tighten refined metal supply.

At the same time, physical market fundamentals remain relatively comfortable. According to ILZSG, the global refined zinc market recorded a surplus of 144,900 t during January-April 2026. However, the group has revised its full-year outlook from a projected surplus of 271,000 t to a marginal deficit of 19,000 t, highlighting expectations that concentrate shortages could gradually reshape market balances during the second half of the year.

Outlook

China's zinc trade increasingly reflects a strategy of importing raw materials while retaining more value addition within its domestic supply chain.

Rising concentrate imports, falling semi-finished imports and stronger exports indicate that Chinese producers are processing a larger share of imported feedstock before supplying both domestic and overseas markets. This trend is likely to continue as long as domestic refining and fabrication capacity remains competitive.

The key risk is raw material availability. If concentrate supplies remain constrained and treatment charges stay under pressure, Chinese smelters may eventually be forced to reduce operating rates, limiting the availability of refined zinc for downstream processing and exports. Until then, China's zinc trade is expected to remain increasingly centred on importing ore and concentrates while exporting higher-value processed products.