China's 15th five-year plan sets out new path for coke sector

...

- Stricter norms to drive consolidation in sector

- Oversupply likely in near term, market to tighten later

Mysteel Global: China's coke sector is set to undergo a structural shift in the following five years guided by the country's 15th Five-Year Plan (FYP), with development focus turning to high added value, enhanced capacity concentration and stricter environmental compliance. This redirection could also lead to changes in fundamentals of the domestic coke market, Mysteel Global predicts.

Stricter environmental norms to drive market reshuffling

The new roadmap charted in China's 15th FYP mandates that around 100 million tonnes/year of coke production capacities should finish the ultra-low emission revamps during 2026-2030, according to the government's document.

The revamp is aimed at lowering particulate matter (PM), sulfur dioxide (SO2), nitrogen oxides (NOx), volatile organic compounds (VOCs) and ammonia emissions during coal preparation, coking, quenching, byproduct production and transportation processes to the required criterion, mainly through installing relevant facilities or adopting environmental measures, Mysteel Global noted.

The targeted 100 million t/y coke capacity for ultra-low emission revamps, though less than the nearly 200 million t/y achieved during the 14th FYP period, signals a tightening of this policy since its nationwide introduction in 2024, as it has become a compulsory regulation with clear deadlines and punitive measures for non-compliance.

For instance, a latest document issued by China's Coking Industry Association specifies that any coke enterprises that violate environmental rules will have their environmental ratings revoked, be barred from reapplication or even face production suspensions.

Besides, the country's emission control campaign will prove an even more stringent action in the following period, with the control spectrum widening to the whole coking process. For 2026 alone, 50 million t/y of coke capacities need to complete the emission transformation, accounting for half of the total targeted volume for the next five years, according to a press conference convened by China's Ministry of Ecology and Environment (MEE) on February 27.

The new environmental regulations mirror China's tougher stance about pushing for decarbonization of key pollution-prone sectors including steel, cement, power and coke. The move is expected to drive the coke market to reshuffle as elevated investments in environmental facility installations could inevitably raise the entry threshold for the industry and boost further capacity concentration, Mysteel understands.

For coke producers, the ultra-low emission revamps could cost them an estimated Yuan 55-65 ($8.1-9.5) for each tonne of coke produced, meaning a cumulative investment of almost Yuan 3.3 billion for meeting the revamp target this year, some market sources shared.

By 2025, approximately 60% of coking capacities in major air pollution control areas - Beijing-Tianjin-Hebei, Yangtze River Delta and Fenwei Plain areas - have completed ultra-low emission revamps.

The coke capacity revamps in these key areas are expected to be largely completed by 2028, according to the MEE, and it targets an 80% transformation for the country's total coke capacities by 2030, which will help drive significant declines in VOCs, PM, SO2 and NOx emissions and an increase of over 10% in solid waste utilization rate by 2030.

Structural shift to occur

In the next five years, authorities will make larger strides in dismantling 4.3-meter and heat-recovery coke ovens in parallel with their moves of upgrading the 5.5-meter ovens and expanding 6-meter-above ones.

In the supply pool, dry-quenching coke (DQC) will represent a larger share while wet-quenching coke (WQC) will be gradually replaced; and the commissioning of larger-size blast furnaces will also guide top-charging oven capacities to expand mildly.

The past five years have witnessed intense elimination of small coke ovens with chamber heights of 4.3 meters or below, with their shares declining to less than 6.5% of the country's total operating capacities and mainly concentrated in Northwest and Northeast China. Besides, 5.5-meter ovens also represent a smaller 30% proportion of the total, Mysteel's survey results showed.

Large ovens with heights of over 6 meters, which are typically designed to be environmentally friendly, have increased to 60% of overall capacities. Capacities of dry-quenching coke (DQC) have further expanded to around 80% of the national total, stimulated by instruction for dry quenching facility installations for all new coke projects.

Value reshaping for coke sector

The Chinese government encourages coke producers to expand their operation chain from coke production to high value-added chemical production as well, in accordance with the country's new policy of including coal chemicals into the national energy security system against the background of global oil supply woes as geopolitical conflicts escalate.

Main chemical products from the coking process include coke oven gas, coal tar and crude benzene. For example, authorities aim to lift the comprehensive utilization rate of coke oven gas - used for producing hydrogen, methanol and synthetic ammonia - to above 95% by the end of 15th FYP period.

Besides, in renewables-rich Inner Mongolia, Xinjiang and Ningxia, Northwest China, new coke projects should promise 30-50% of their electricity consumption from green sources and utilization of green hydrogen in heating ovens before gaining approvals.

Potential changes in market fundamentals

Some market insiders anticipate China's coke market fundamentals to remain loose during 2026-27s before a tightening trend emerges in 2028-30. The scenario is based on the fact that many coke capacities are still under construction, which will come online in the following two years. With the commissioning of these new capacities, some small- and medium-size enterprises may leave the market later due to capacity elimination or financial pressures.

Coke demand, however, will likely maintain a shrinking trend in the next five years, in tandem with a similar trend for domestic crude steel production.

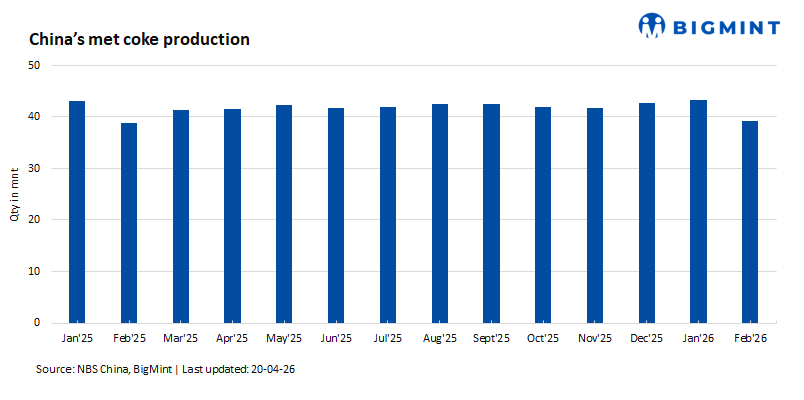

In 2025, China boasted coke capacities of 570 million t/y, which, however, failed to be completely digested due to fluctuated demand from the steel sector and volatile international trade environment. The resultant supply glut has constrained profitability among coke producers, Mysteel learned.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.