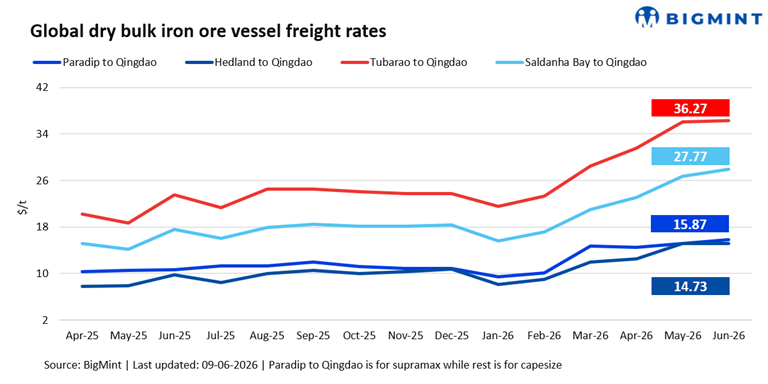

Capesize pressure weighs on iron ore freight sentiment, Supramax remains resilient

...

- Weaker Pacific activity weighs on Capesize earnings

- Steady minor bulk demand keeps Supramax relatively stable

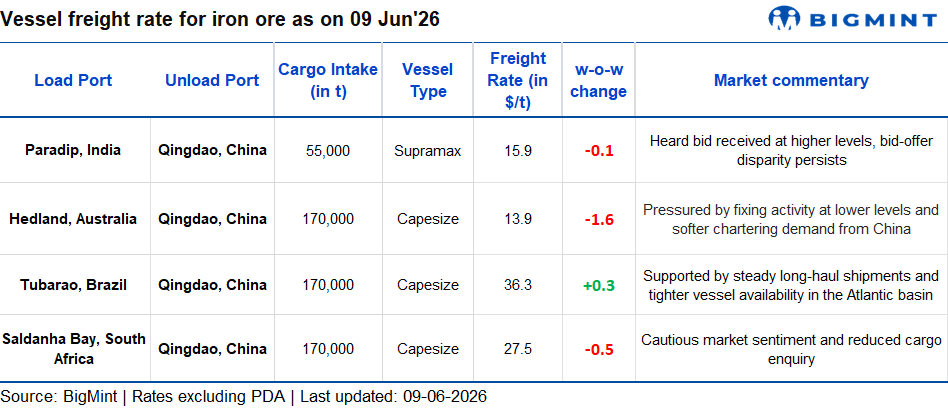

Dry bulk iron ore freight sentiment weakened w-o-w on 9 June 2026, with declining rates on key Pacific and South African routes reflecting softer chartering activity and cautious buying interest from China.

The Capesize market remained under pressure amid reduced fixing activity in the Pacific basin and softer iron ore demand sentiment. Higher vessel availability, limited cargo enquiries, and fixtures concluded at lower levels weighed on rates, particularly on the Australia-China route. Although Atlantic cargo flows provided some support, overall sentiment remained bearish as the market continued to grapple with excess tonnage.

Meanwhile, the Supramax segment remained relatively stable, supported by balanced vessel supply and steady demand for minor bulks. Continued cargo enquiries and regional trading activity helped maintain stability, keeping sentiment slightly positive compared with the weaker larger-vessel segments.

A shipbroker stated, "Capesize remained under pressure, while Panamax softened slightly on limited cargo activity. Supramax and Handysize markets held steady, supported by balanced fundamentals. Although enquiry volumes were modest, ongoing cargo and time-charter requirements from operators helped maintain a degree of market interest."

Route-wise update

Outlook

The iron ore freight market is expected to remain cautious in the near term, with Capesize rates likely to be influenced by Chinese steel production levels, iron ore procurement activity, and fresh cargo emergence from Australia and Brazil.

While Atlantic basin exports may provide intermittent support, ample vessel availability could continue to pressure earnings. Meanwhile, the Supramax segment is expected to remain relatively stable to firm, supported by steady minor bulk trade and higher bids.