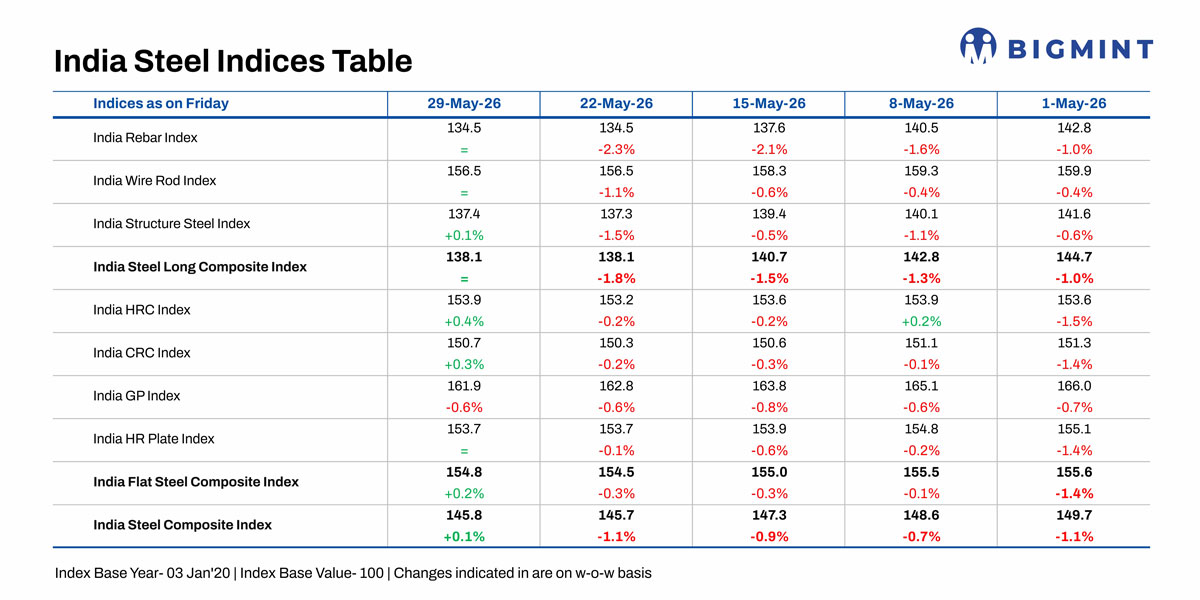

BigMint's India steel index stable w-o-w amid need-based demand, inventory pressure

...

- HRC prices stable, CRC rises marginally w-o-w

- BF rebar trade prices decline by INR 1,000/t (over $10/t)

- Seasonal weakness to weigh on market amid rising inventory

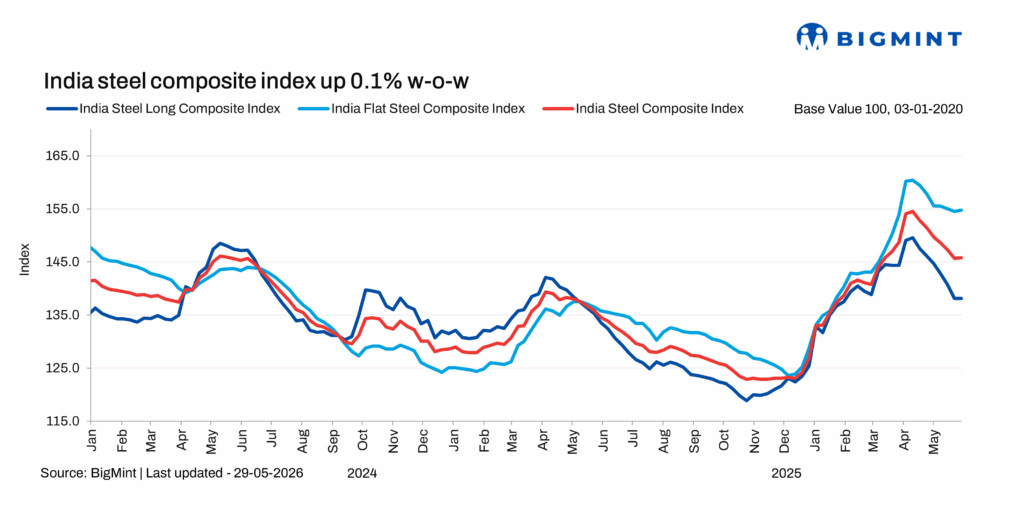

Morning Brief: BigMint's India steel composite index remained flat w-o-w, rising by just 0.1% in the week ending 29 May 2026. Steel prices started moderating in April, after the Middle East crisis triggered a rally in March, with the fiscal year-end demand and consumption momentum starting to slacken somewhat in April. Trade channel sentiment still remains muted even as mill- and distributor-level inventory edged up in May.

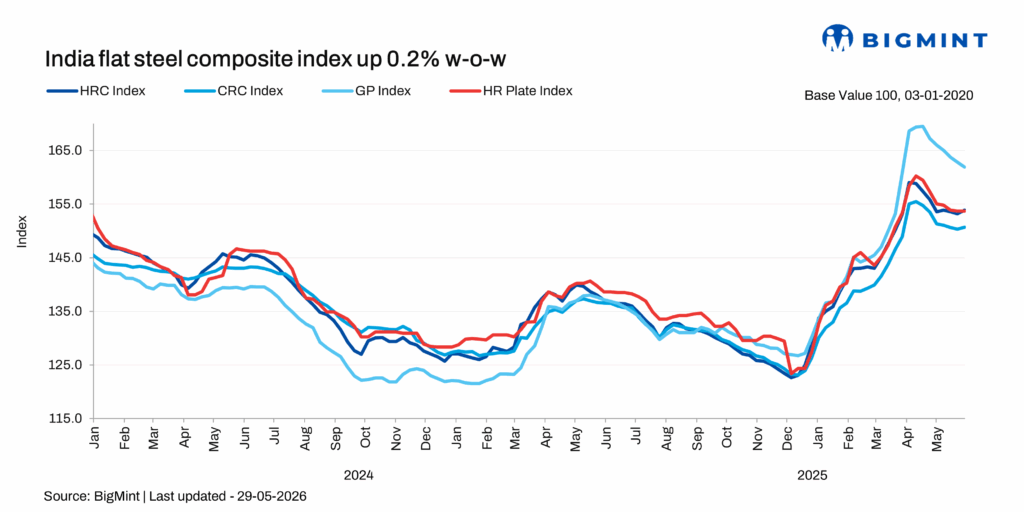

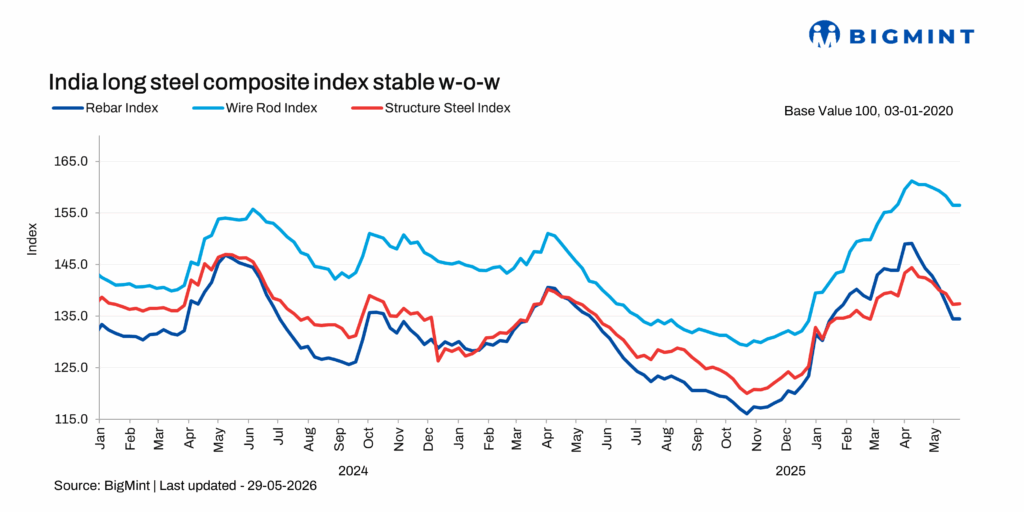

While the longs index remained unchanged w-o-w, the flats index edged up marginally by 0.2% due to a 0.4% uptick in HRC and 0.3% in CRC. However, the coated segment still remained in the red.

Highlights of price movements

Flat steel prices remain largely stable: BigMint's bi-weekly assessment for HRC (IS2062, Gr E250, 2.58 mm/CTL) was assessed at INR 58,500/t ($616/t) as of 29 May against INR 58,700/t ($618/t). However, CRC (IS513, Gr O, 0.9 mm/CTL) increased by INR 200/t ($2/t) w-o-w at INR 65,200/t ($687/t) on 29 May against INR 65,000/t ($685/t) on 22 May. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Trade-level HRC prices remained largely stable, although "some distributors attempted to push offer prices higher in Ludhiana", a ferrous market source informed BigMint. However, demand continues to remain subdued, with buying activity restricted primarily to immediate requirements. End-user consumption is yet to recover meaningfully, resulting in limited acceptance of higher offers.

A distributor in north India informed, "Mills are focusing on liquidating stockyard inventories". Mills continued focusing on dispatch discipline amid subdued spot demand and cautious downstream participation.

Slight uptick in imports, exports subdued: Despite the marginal uptick in bulk HRC imports in April and May, especially from non-FTA destinations such as China, the price spread between domestic HRC and landed cost of imports from non-FTA countries remains at around INR 7,000/t. Therefore, domestic prices are cushioned by the safeguard duty and do not seem to be weighed down by imports unlike last year.

Indian HRC export activity remained subdued last week, with shipments to Europe and the Middle East constrained by regulatory uncertainty, logistical disruptions and weak buying sentiment.

Inventory pressure weighs on rebar: IF-route rebar prices witnessed mixed trends across regions last week. While overall market activity remained limited, buying interest improved only for a brief period during the week, with most buyers maintaining a cautious approach and restricting purchases to immediate requirements.

Sellers attempted to push prices higher amid signs of better market movement; however, resistance from buyers at elevated price levels limited trade. Inventory pressure persisted at mills, with stock levels reported at around 10-15 days.

BF rebar prices (distributor-to-dealer) declined by INR 1,000/t ($10/t) w-o-w to INR 55,800/t ($487/t) exy-Mumbai. Inventory levels at major mills surged by over 30%, while heightened selling pressure at the distributor level continued to weigh on market sentiment. Buying activity remained moderate across regions, while demand in south India continued to stay weak. Need-based procurement was seen amid limited construction activity.

The BF-IF rebar price spread in Mumbai widened w-o-w to INR 9,000/t ($103).

Iron ore stable, coking coal firm: Odisha iron ore prices last week remained stable even as some private miners adjusted their offers downward in line with declining prices in OMC's auction in mid-May. Weakening steel prices exerted pressure on iron ore but imported coking coal remained firm amid China mine accident and stable supply conditions, while elevated wholesale inflation in fuel and industrial inputs continues to pressure mills.

Outlook

The steel demand cycle remains unshaken and the present demand downtrend is cyclical rather than structural. Steel prices may not show a major improvement in the June-September quarter due to seasonal factors but restocking demand may provide short-term boosts.

Geopolitics is always the wild card in the commodity market and volatility cannot be ruled out. Amid weak export sentiment and the momentary surge in bulk imports, the primary mills are expected to roll over HRC and CRC prices for June, while rebar may continue to face inventory pressure amid weak construction sentiment.