Asian thermal coal rally pauses as Indian demand softens, but China and Indonesian supply tightness keep market supported

...

- Indonesian low-CV coal gains but Australian, South African prices stable

- Summer power demand, tighter hydro supply lifts Chinese domestic prices

The Asian thermal coal market entered a consolidation phase in the final week of May (25-30 May 2026), with buying activity slowing amid holiday-related disruptions, elevated freight costs, and cautious procurement from Indian industrial consumers. Despite the loss of momentum, the market remains fundamentally supported by rising Chinese domestic prices and tightening availability of Indonesian low-calorific-value coal.

While Australian and South African coal prices remained largely stable, Indonesian low-rank coal continued to outperform, emerging as the strongest segment of the thermal coal complex.

China provides the market floor

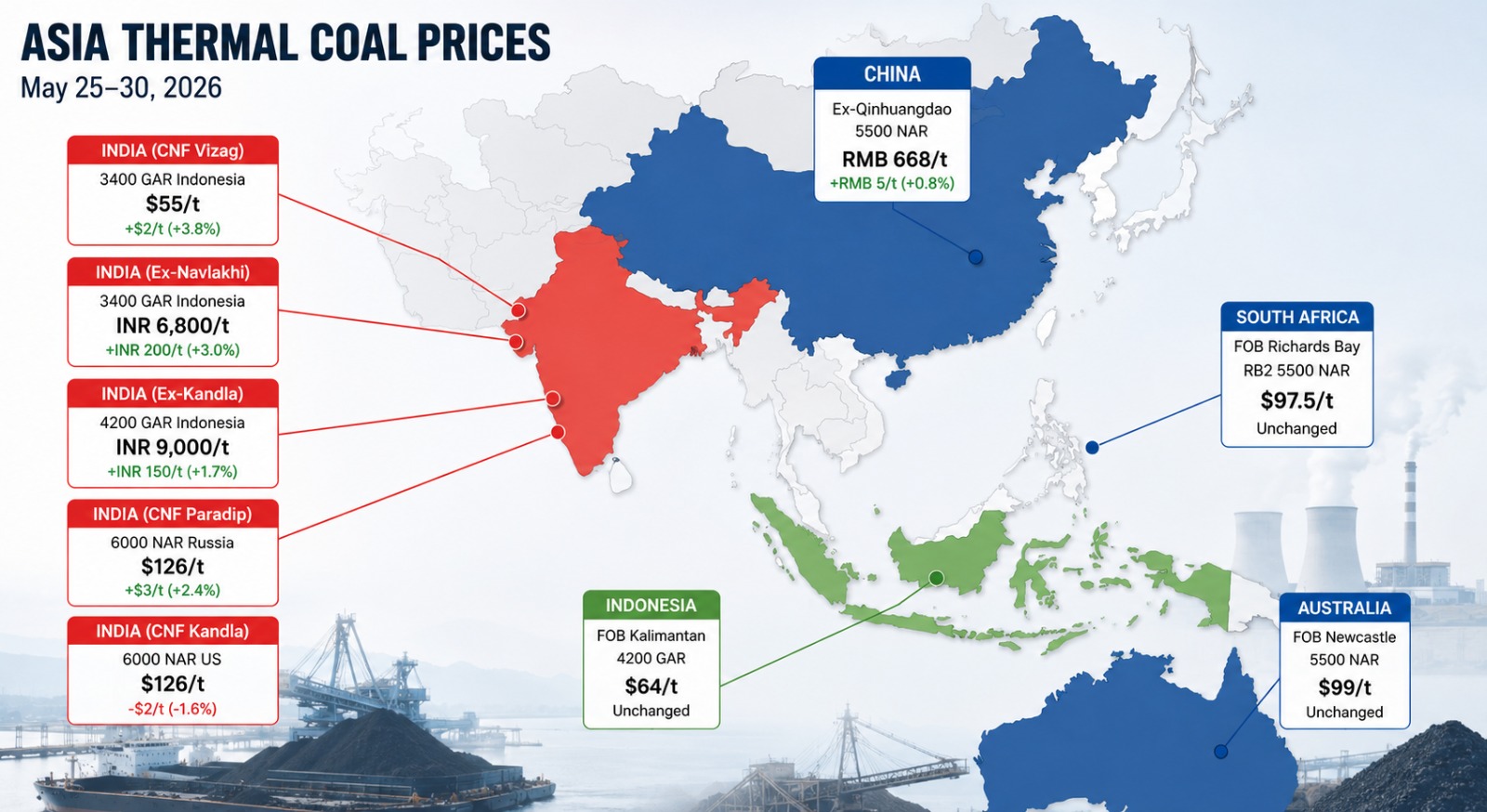

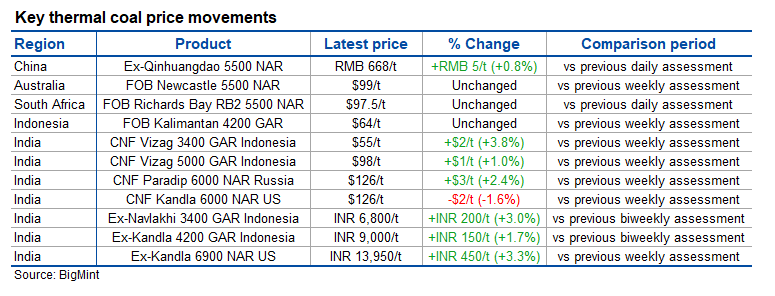

China remains the primary source of support for regional thermal coal prices. BigMint's ex-Qinhuangdao 5500 NAR assessment rose to RMB 668/t on 29 May, up from RMB 651/t a week earlier and RMB 622/t a month ago.

The rise reflects the onset of summer power demand, reduced hydropower availability in parts of southern China, and continued supply discipline across domestic mines.

However, stronger domestic prices have not yet translated into broad-based import buying. Chinese buyers remain highly selective, favouring Indonesian low-CV cargoes where delivered economics remain attractive while showing limited appetite for higher-priced Australian and South African coal.

Tender activity suggests that low-rank Indonesian coal supply remains particularly tight, with buyers willing to pay premiums for prompt cargoes.

Indonesian coal continues to outperform

The clearest bullish signal in the market remains Indonesian low-rank coal.

Although FOB Kalimantan 4200 GAR was unchanged at $64/t, downstream markets continued to strengthen. CNF Vizag 3400 GAR rose 3.8% w-o-w to $55/t, while ex-Navlakhi 3400 GAR increased 3% to INR 6,800/t. Ex-Kandla 4200 GAR climbed to INR 9,000/t.

The strength reflects a combination of production quota constraints, uncertainty surrounding Indonesia's proposed export reforms, and resilient blending demand from India and China.

More importantly, these gains have occurred during a period of slower trading activity, highlighting the underlying tightness in the market.

Indian demand remains selective

Indian buying remains concentrated in low-CV Indonesian coal, while demand for higher-CV imports remains mixed.

CNF Kandla 6000 NAR US-origin coal fell $2/t to $126/t, while Russian 6000 NAR coal into Paradip rose $3/t to the same level. The divergence reflects differences in freight economics and cargo availability.

The strongest demand continues to be focused on Indonesian 3400-4200 GAR coal, which offers attractive blending economics for industrial consumers.

South African coal, meanwhile, continues to struggle. Weak sponge iron margins, comfortable domestic coal availability, and competition from alternative fuels have limited import demand. Portside RB2 prices remained broadly stable at INR 11,300-11,800/t across major Indian ports.

South Africa and Australia remain rangebound

South African prices showed little movement during the week, with RB2 5500 NAR assessed at $97.5/t and RB1 6000 NAR at $107/t.

The market remains caught between firm producer offers and subdued buying interest. Competition from Russian coal in Asia and Colombian cargoes in Europe continues to cap upside.

Australian coal faces a different challenge. FOB Newcastle 5500 NAR remained unchanged at $99/t despite firmer Chinese domestic prices. Japanese and South Korean demand remains steady, but Chinese buyers have yet to return in sufficient volumes to tighten the market.

As a result, both Richards Bay and Newcastle remain largely rangebound while Indonesian coal continues to lead the market higher.

Outlook

The Asian thermal coal market is increasingly becoming a story of two markets.

The first is Indonesian low-CV coal, where supply constraints and steady blending demand continue to support prices. The second is higher-CV Australian and South African coal, where demand remains adequate but insufficient to generate sustained upside.

BigMint expects FOB Kalimantan 4200 GAR to remain supported in the $64-67/t range through June, while CNF Vizag 3400 GAR could strengthen further if supply constraints persist.

FOB Newcastle 5500 NAR is likely to remain within $98-102/t, while Richards Bay RB2 is expected to trade around $95-99/t. Chinese domestic prices may continue to edge higher as summer power demand builds.

For now, the market remains supported rather than bullish. However, the continued outperformance of Indonesian 3400-4200 GAR coal suggests that low-rank material has become the most strategically important segment of the Asian thermal coal market.